Accounting and Microeconomics - The fundamental tools for effective business management.

Photo by Adeolu Eletu on Unsplash

Author: Nikolay Marinski.

the business toolkit

For entrepreneurs, managing a business, whether in a start-up or an already scaled-up company, isn’t just about having a good idea or offering a useful product—it’s about making strategic decisions that propel the enterprise forward. Accounting and microeconomics are the foundation of those decisions. They provide the information required for managers to decide what is the best course of action. Accounting focuses on keeping track of where the money comes from and where it goes. Combined with microeconomics, which helps explain why those numbers look the way they do and how markets respond to different choices, they give a complete overview of the internal health of the business and the external forces in the market which are influencing and shaping its path to success, such as pricing products, understanding customers, and learning how to compete effectively. In the increasingly competitive and data-driven world we live in, understanding both is not just helpful—it’s essential for long-term success.

Accounting in Business Management

Accounting plays a crucial role in both the short-term and long-term success of a company. It is a process which records and organises financial information in a structured way, enabling managers to clearly see how the business is performing and which activities need improvement. There are three main types of financial statements, which help organise information, based on the performance aspects a manager wants to inspect.

Firstly, the cash flow statement reflects the amount of capital flowing in and out of the business over a certain period of time. It is an important and easy-to-follow financial statement because it follows the cash earned by and spent on the business through operating, investment, and financing activities.

Additionally, the income statement is also referred to as a profit and loss (P&L) statement. It follows how the net revenue is turned into net earnings, over a specific period, usually a quarter or a year, by taking into account the different expenses the business has. The statement provides valuable insights into the main and secondary operations of a business, and the performance relative to industry peers. Primary revenue and expenses show the enterprise generates cash with its core activity, while the secondary revenue displays how the company is capitalising on available assets and resources for additional capital inflow. This reveals to managers where costs could be cut, helping to increase profit over time, or whether an operation should be expanded or shut down.

A balance sheet accounts for a business's assets, liabilities, and shareholders' equity at a specific time. An important note to mention is that a balance sheet always follows the commonly called “accounting rule”, where assets equal the liabilities plus the shareholders’ equity. A balance sheet helps to determine the risk a company can take, as it enables managers to quickly assess whether they have too much debt, if it has enough cash to cover costs or whether there are enough liquid assets if more cash is needed.

Moreover, there is a financial branch of accounting that focuses on presenting a company's financial position to external stakeholders, such as investors, creditors, and regulators. Investors use the aforementioned financial statements to analyse a company’s financial health and calculate key ratios, which are later considered to determine whether the company is worth investing in or its creditworthiness.

Therefore, accounting is fundamental, not only in management, but is crucial for a business to know how to organise its statements in a way that makes it look in the best way possible when presented in front of external stakeholders and potential investors.

Understanding the market

Microeconomics analyses the market and how different individuals and factors influence demand through changes in customer incentives.

Тhe study of microeconomics combines several concepts. The utility or consumer theory examines and tries to predict how customers make decisions with their budget constraints, preferences, and based on the perceived value. It mostly relies on a couple of assumptions about human behaviour - humans strive for utility maximisation, or said otherwise, they aim to purchase products that bring them the most benefits for their budget. Additionally, it is taken into consideration the human trait of always wanting to consume more, but also that customers lose interest the more they use a product.

On the business side, there is the supply or production theory, which observes a company’s aim to maximise output and minimise costs through the use of different production methods. This helps businesses produce in alignment with the current market demand, preventing the wasting of resources.

By combining these theories, we get the theory of supply and demand, which determines the pricing in a competitive market. Businesses rely on these concepts to set prices that are both competitive and profitable

Moreover, microeconomics provides an understanding of different market structures. It helps determine the competition, each company's market share, and each company's growth. This gives managers a clear picture of current market conditions and whether any changes or innovations are needed for the enterprise's survival and development.

The benefits of aligning accounting data with microeconomic principles

By understanding what each has to offer, it becomes evident why a deep understanding of both is required for a business. When the raw data of accounting, which analyses in a structured way the information about internal revenues, costs and overall performance, is put within the microeconomic context of customer behaviour, competition and market dynamics, it enables the business to not only build a solid operational foundation, but to construct a strategic long-term development plan.

Clear examples of this are pricing decisions and innovations in the business models. Combining the accounting data, which reveals all the direct and indirect costs to produce a certain product or provide a service, with the microeconomic concept of demand elasticity, which examines how customers respond to different price levels, ensures that businesses not just cover their costs, but instead maximise their revenue. Furthermore, it becomes important when businesses need to allocate their resources. Understanding the external drivers of the market displays the current needs and wants of the customers and how well our product can satisfy them compared to our competitors. It also could be used as a signal to know when the market is changing, and an investment in a new innovative approach may be required. In this scenario, managers need to understand the financial situation of the business in order to know the extent to which they can risk capital to experiment with new products or operating models.

Challenges and Limitations

While there are many positives to the use of these two studies, they also bring some difficulties for the company.

The complexity of accounting data grows exponentially with the development of the business, and at certain point, a skilled accountant becomes a necessary investment. There are numerous examples of companies which have failed and gone bankrupt because of either unskilled accounting or fraudulent use of deceptive accounting practices to hide poor performance..

A relatively recent example was the major and well-known British construction and service company Carillion, which collapsed in 2018 under £1.3 billion of debt. The company relied on an aggressive management tactic by taking long-term debt and acquiring competitors. At its “prime” it was considered one the the largest British construction companies with more than 400 public sector contracts for schools, prisons, military housing, and large transportation projects. Additionally, many of the acquisitions made included goodwill payments (paying over the company’s fair market value to acquire them). These were again part of the aggressive expansion tactics, silencing any competition, and were justified as long-term assets and investments because of their positive financial outlooks. When those outlooks didn’t materialise, Carillion took years to record the payments as losses. In the end, the company was estimated to have £1.57 billion worth of goodwill payments on its books: a value that didn’t actually exist. Moreover, Carillion used a financing scheme known as reverse factoring. Factoring is a common agreement where, rather than waiting for the customers to pay, the company gets the bank to lend cash against the invoices. Carillion’s reverse factoring used a similar logic, but with its suppliers.

Another example is the major American telecommunications company WorldCom, which in 2002 became the centre of one of the biggest accounting scandals, resulting in around $11 billion in fraud. It was founded in 1983 and, through acquiring relatively 30 of its competitors, was built into one of America’s biggest telecommunications companies, with its market capitalisation reaching $186 billion during the Dotcom bubble. The aggressive acquisition, coupled with a decrease in revenues, pushed the company into the red. To prove WorldCom was still financially viable, executives used a set of fraudulent accounting techniques, such as recording expenses as investments, complicated accounting terms were used to hide the movement of capital, and financial transactions were made with a lack of evidence. By doing so, it exaggerated its profits by $3.8 billion, reporting a profit of $1.38 billion, instead of a net loss. This scandal prompted the creation of the Sarbanes-Oxley Act of 2002, aimed at increasing corporate accountability and transparency in financial reporting.

As already discussed, microeconomics also plays a crucial role in the success of a business. There are plenty of examples of businesses which have gone bankrupt in various markets because of a lack of understanding or neglect of the microeconomic drivers.

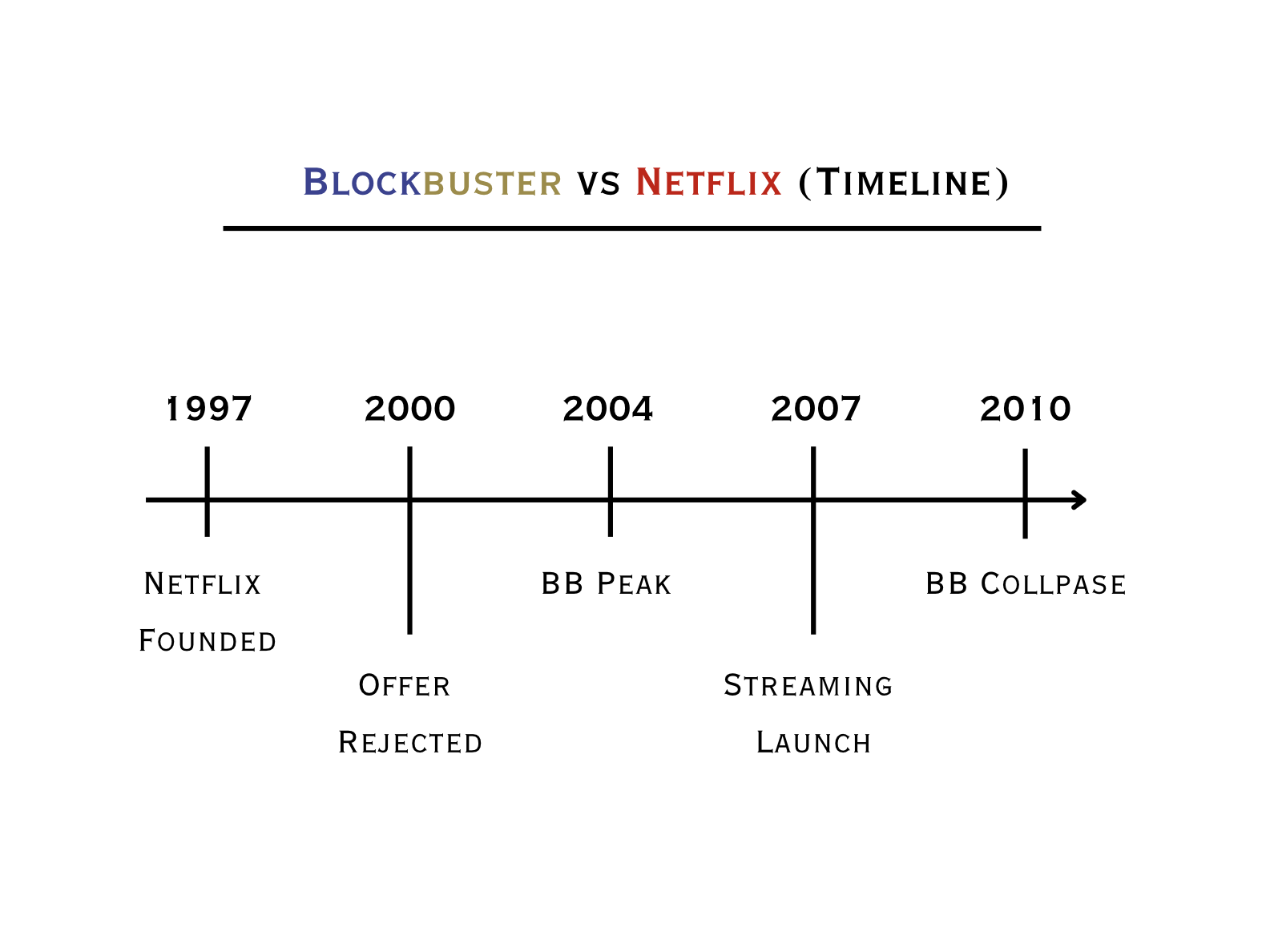

Probably the most famous one is the downfall of the dominant American video rental chain in 2010. Founded in 1985 in Dallas, Texas, by David Cook, the company introduced computerised tracking and a vast, organised selection of tapes, revolutionising the fragmented video rental market. In its prime in 2004, it grew to having more than 9000 stores, making $5.9 billion in revenue. While renting movie tapes was its main activity, they made a significant portion of their revenue (16% or $800 million) from charging late fees. While it was developing at a rapid rate, a competitor emerged in the form of the now-well-known company Netflix. The entertainment giant was founded by Reed Hastings and Marc Randolph in 1997 in Scotts Valley, California. Hastings got the idea after he was annoyed by a $40 late fee for a Blockbuster VHS tape.

Source: The Financier Review

The first plan for Netflix was simple, but innovative - they would send DVDs by mail for a flat monthly rate. People could also order online, which was a fresh idea at the time. Additionally, Netflix used data to suggest movies people might like, making the service more attractive and easier for users. In 2000, Netflix faced hard times with the burst of the dot-com bubble, and the company had a lot of expenses. Hastings and Randolph went to Blockbuster with a $50 million offer to sell Netflix, but the leaders of Blockbuster, feeling sure of their position, turned down the offer, even reportedly laughing at it. In 2004 and 2005, Blockbuster saw an increase in demand for quicker rental options with no late fees and launched Blockbuster Online and decided to end late fees, resulting in a combined cost of $400, but it was years behind Netflix and was less effective. In 2007, Netflix made the big move of starting streaming services, with the rapid spread of fast internet. This was the final blow to Blockbuster, as it couldn’t move to a digital format and was stuck with its physical stores, which were dying out and went bankrupt in 2010.

Another noticeable case is the failure of Nokia and BlackBerry. In the early 2000s, these phone brands were ruling the market. Nokia, formerly being the world's dominant mobile phone manufacturer, grew because of its sturdy phones with long-lasting batteries and user-friendly interfaces. Alternatively, BlackBerry was the ultimate status symbol for business professionals. They offered unmatched at the time security with their encrypted messaging through BBM (BlackBerry Messenger), which allowed for instant and secure communication. Additionally, its iconic physical keyboard (the QWERTY keyboard) provided fast and efficient typing, making it preferable for professionals who used emails and texting. This created a loyal corporate customer base, as BlackBerry became deeply embedded in the business and government sectors. Nevertheless, when Apple launched the first iPhone on June 29, 2007, it created a disruption in the market, changing the physical keypads to user-friendly touchscreen interfaces. Following this, Samsung, initially a component supplier to Apple, saw the potential of the smartphone market and in 2009 launched its first Galaxy phone. While initially, both Nokia and BlackBerry stuck with their belief that users would always prefer physical buttons and dismissed the touchscreen and app stores as a short-term trend, they eventually saw the customer demand for those features, but Apple and Android had already taken over. Nokia’s and BlackBerry's OS were outdated and slow to evolve. With Apple’s App Store and Google Play becoming some of the main selling points, the two declining companies' ecosystems also became obsolete, as they offered a limited number of native apps, especially with Nokia deciding to partner with Microsoft, instead of adopting Android.

Conclusion

Understanding and using microeconomics and accounting is fundamental to a business's health. The latter tracks and organises the financial data of the internal practices of a business, enabling both managers to track performance and compare it to their development plans, and investors and creditors to examine if the business is credit and investment worthy, which could further help the enterprise to reinvest this external capital for further growth. On the other hand, the study of microeconomics focuses on the market in which the business operates and its drivers, allowing managers to have a comprehensive view of external factors such as consumer incentives and demand elasticity.

While fraudulent tactics in accounting are possible, to create a false sense of viability in front of external stakeholders in the short-term, ignoring those cracks in the business ultimately leads to the downfall of the company. Similarly, ignoring changes in the market conditions and demands precipitates their fall. When taken into account and interpreted correctly, with an aim of optimising operations, the combination of these studies reveals the strengths, weaknesses, bottlenecks, and developmental areas and opportunities in a business, the combination of which can be condensed into a comprehensive long-term strategy.

Bibliography

Berger, Adam J. “WorldCom Scandal | EBSCO.” EBSCO Information Services, Inc. | Www.ebsco.com, 2022, www.ebsco.com/research-starters/business-and-management/worldcom-scandal.

Byrne, Dan. “What Happened to Carillion?” The Corporate Governance Institute, 18 Feb. 2026, www.thecorporategovernanceinstitute.com/insights/case-studies/what-happened-to-carillion/.

Hayes, Adam. “The Rise and Fall of WorldCom: Story of a Scandal.” Investopedia, 14 June 2024, www.investopedia.com/terms/w/worldcom.asp.

Joshi, Nikhil. “Why Nokia and Blackberry Lost Their Edge - Nikhil Joshi - Medium.” Medium, 15 Mar. 2025, medium.com/@cast_shadow/why-nokia-and-blackberry-lost-their-edge-ab1c050d99e7.

Mor, Federico. “Carillion Collapse: What Went Wrong?” Commonslibrary.parliament.uk, 19 Jan. 2018, commonslibrary.parliament.uk/carillion-collapse-what-went-wrong/.

Olito, Frank, and Alex Bitter. “Blockbuster: The Rise and Fall of the Iconic Movie Rental Store.” Business Insider, 24 Apr. 2023, www.businessinsider.com/rise-and-fall-of-blockbuster?st_source=ai_mode#but-trouble-was-on-the-horizon-in-1997-as-blockbusters-future-competitor-netflix-was-founded-7. Accessed 22 Apr. 2026.

Nikolay Marinski

Chief Business Analyst, Financial Analyst.

The Financier Review

© 2026 The Financier Review. All rights reserved.