How to Boost Your Valuation 101 - SpaceX Wants It Big Pre-IPO.

Article Authors: Spas Arsov, Mihail Gaydarov.

Buyer and Seller Background

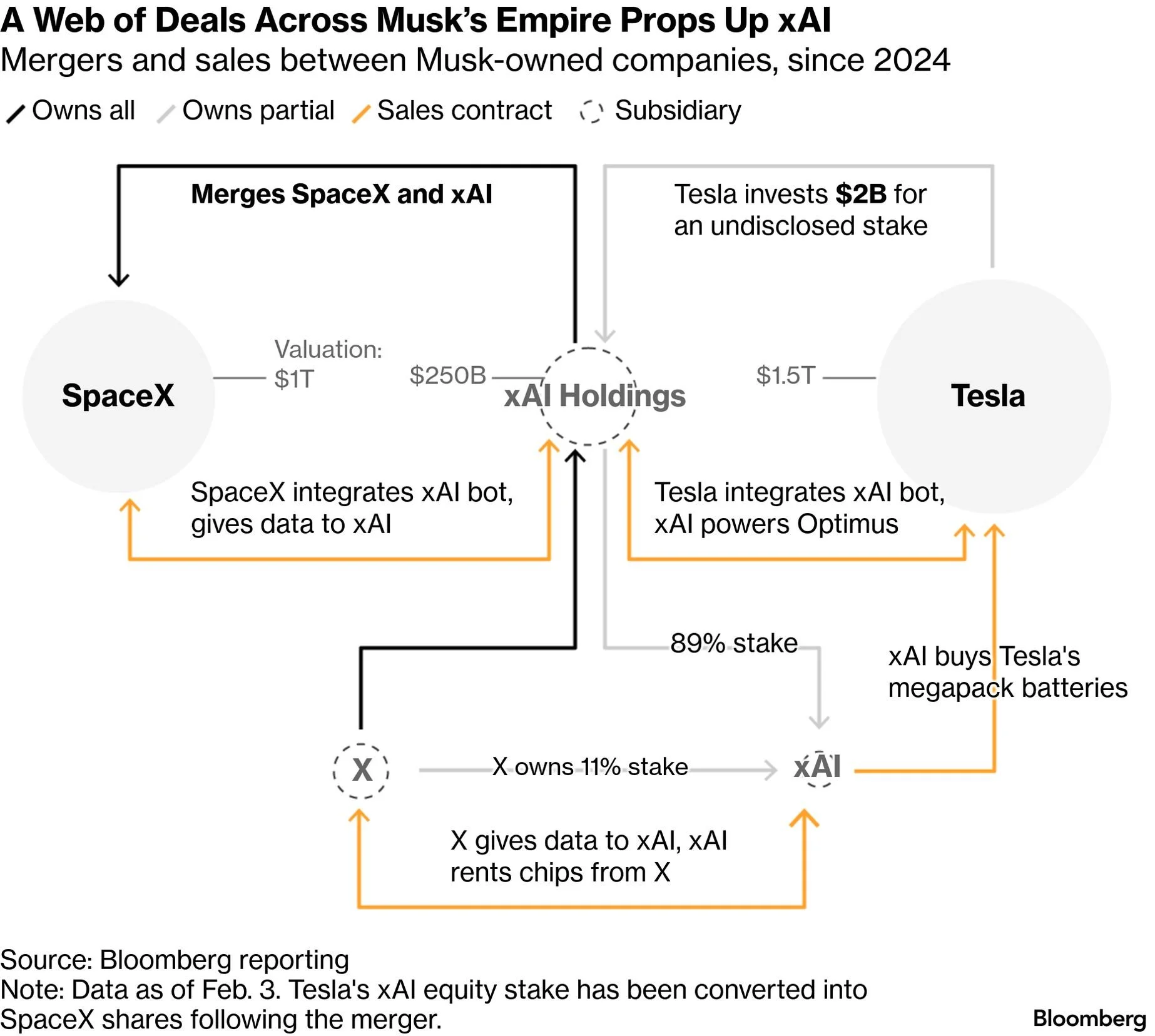

A jump from $800 billion to $1.75 trillion is not mere growth for a company but a test of how much a market can be convinced on behalf of an idea. The company responsible for the first private launch, orbit, and recovery of a spacecraft, SpaceX, is currently merging with Elon Musk’s other daughter company, specialising in AI development known as xAI. At the centre of this merger are two companies that operate in completely separate markets, which raises the question - why? Why would two companies that have absolutely nothing in common besides a common founder find the need to join ventures? They both share the appetite forcapital-intensive scaling and a close technological narrative on the innovation frontier.

While SpaceX is currently the dominant actor in commercial launch services, it also specialises in enhanced satellite connectivity. The businesses’ core activities revolve around many areas, the most vital of which are launch vehicles (reusable), defense contracts, and Starlink. Perhaps out of all of SpaceX’s business, Starlink is the most vital from a financial standpoint. Credible sources, like Reuters, report that SpaceX generated $15-16 billion in revenue in 2025. From that revenue, the derived EBITDA is in the range of $8 billion. Such amounts of profit place the company far beyond a speculative-backed aerospace enterprise.

Observing the xAI side of the deal, it is an artificial intelligence company which began its operations with the mission to accelerate scientific discovery and develop human understanding of the universe. With that in mind, xAI is not just a software that tries to rival competitors like OpenAI’s ChatGPT and Google’s Gemini but tries to leverage a position as a broader infrastructure enterprise-AI platform. Undoubtedly, the most popular product that the company has produced is their generative algorithm, "Grok," which is included in Elon Musk’s “X” media platform and also as a free-to-use LLM. Another popular service from xAI is their APIs, which are essentially developer toolkits that allow the integration of Grok into private commercial solutions. In terms of classifying xAI from a corporate viewpoint, their website proclaims the company as a scientific and engineering-led AI platform. As of November 2025, the company was in talks for a financing round at a $230 billion valuation, which, compared with their previous merger with "X," is almost double the valuation they had.

Tactically, the merger between these companies is tied to the following logic: SpaceX controls most of the physical infrastructure that xAI needs. Within that segment, we categorise launch capabilities; orbital deployments; satellite networks, which are crucial to Starlink networks; and more. On the other hand, xAI provides the software layer for the enterprise's intelligence. Services like model training, data analysis, and enterprise-grade tools are some of the cornerstone elements of this merger. In theory, now SpaceX as a whole will have the capabilities to independently cover all of their infrastructural needs and further enhance their operating capabilities - making it an intelligence-enabled infrastructure platform. The framing of the merger is very important; instead of selling SpaceX as an aerospace business, the combination of these two entities allows the combined group to be marketed as the culmination of space exploration, overall network connectivity, defense, and development of modern technologies like LLM AI models.

Contextually, though, it’s not really a strategic issue but rather a financial one. Both businesses are in industries where scale and execution matter far more than short-term profitability because they’re capital-intensive. SpaceX needs capital to build Starship and satellites. xAI needs capital to build compute and models. Therefore, this approach is much less of a vision play and far more of a capital-market engineering solution. Tying an AI story to an aerospace vehicle allows for the justification of a higher multiple. It is also important to note the compound's execution risk. Everything about this tension still stands—real industrial symbiosis vs. strategic adjacency as a valuation multiplier.

The IPO Target

Before we dive into the nature of the deal and the details regarding the merger, we have compiled a small paragraph with core numbers relevant to the case.

In December of 2025, the offer valuation was at $800 billion.

SpaceX reply: Stock buyback at $421/share for about $2.56 trillion.

The reported IPO valuation target exceeded $1.75 trillion (April 8th, 2026).

In essence, the data suggests a step-up in valuation from $800 billion to $1.75 trillion, equating to a 2.19x increase in valuation (119%). This massive repricing is not just a normal readjustment of valuation but a repricing exercise that would test the limits and objectivity of public valuations.

The operating data suggests an EBITDA of $8 billion for 2025 at a revenue of $15-16 billion. Reports from Reuters show that investor optimism regarding this deal is very heavily skewed towards Starlink. As of recently, Starlink had more than 10 million subscribers worldwide, accounting for SpaceX’s high launch frequency at almost one rocket every two days.

If we were to use the Reuters valuation framework at $1.75 trillion, the valuation is placed at 56x revenue and 109x EBITDA, supported by 2026 revenue estimations. Certainly, at such a high valuation, the market would place SpaceX at an extraordinarily high valuation and far greater than the justified norm for the industry's aerospace alternative companies. This puts SpaceX in a category with extreme frontier-tech multiples, as stated by Reuters.

The valuation is possible due to several factors related to management's efforts to achieve it. Most importantly, his high valuation number rests on the idea that there are no other public equivalents. Subsequently, this gives hand to banks and investors the ability to justify this so-called speculative premium over the regular market valuation. The profitability and scalability of the Starlink business model are also key factors in this case. The possible integration of xAI, it allows for the future deployment of up to one million data-center satellites orbiting Earth. In comparison, Saudi Aramco’s market capitalization sits at about $1.75 trillion for 2026, which directly places the $1.75 trillion valuation for SpaceX next to one of the largest listed companies in the world. In contrast, the value of the Saudi Arabian Oil Company is based highly on established, large-scale cash flows, while SpaceX relies on current strengths accompanied by very bullish future expectations.

The prior valuation of xAI at $230 billion is $20 billion less than the proposed valuation for the merger, putting xAI at $250 billion and SpaceX at $1 trillion for February 2026. The primary risk associated with this potential merger is the valuation itself, which is heavily dependent on the successful execution of Starship commercialization, direct-to-call services for Starlink, and other broader AI-linked satellite ambitions. Put simply, the IPO is strongly supported if investors agree on the future possibilities and new frontiers unlocked by the unification of xAI and SpaceX. After all, this makes the valuation very structurally insolvent if the execution of the aforementioned sectors fails.

The mission of SpaceX is a visionary one and the need for further AI integration via xAI into the aerospace industry is a crucial step for the optimisation of time, resources, and labor, but “valuation bloating” together with market hype could never guarantee long-term strategic success.

M&M (Mergers & Musk)

A $250 billion acquisition deal. And the hype is not even close to what this means. A deal greater than the Vodafone-Mannesmann deal in 2000 following the $180 billion acquisition of Mannesmann AG, which in today’s standards could be adjusted for inflation to about $360 billion. Nevertheless, this is the biggest merger in history in regards to the combined value of the conglomerate being up to $1.25 trillion in valuation of the private entities.

The merger was finalized on February 2, 2026, which transformed SpaceX into a behemoth with "the most ambitious, vertically-integrated innovation engine on and off earth", while incorporating 2 other primary Musk-controlled entities – xAI Corp. and X Corp. With this manoeuvre the total stake of Elon Musk in SpaceX has increased to 42% or roughly $525 billion, based on the $1.25 trillion valuation from the February merger. This number could increase up to $735 billion if the $1.75 trillion deal materialises. Another important factor in the ownership structure is Alphabet with a 7% stake, the second biggest after Musk, which could be worth up to $120 billion if the IPO lives up to the expectations. The rest of the company is split among institutional and venture capital firms such as Fidelity Investments, Founders Fund, Andreessen Horowitz, Sequoia Capital, Draper Fisher Jurvetson, Coatue, and Valor Equity Partners. Even the Ontario Teachers' Pension Plan is also listed among its investors. Several publicly accessible funds have acquired significant holdings in SpaceX. These include the Baron Partners Fund (run by early Musk backer Ron Baron), Cathie Wood's ARK Venture Fund, and The Private Shares Fund. In the UK, the investment trusts Scottish Mortgage and Edinburgh Worldwide hold SpaceX as their largest position. Furthermore, SpaceX employees hold equity in the company, which they have periodically been able to sell through internal tender offers facilitated by the company.

Lastly, and most worryingly for the US government, in its role as a significant government contractor of SpaceX, foreign and minority mostly Chinese investors, such as the Shanghai-based Leo Group, who have purchased shares through offshore special purpose vehicles (SPVs) in the Cayman Islands and British Virgin Islands, often facilitated by middlemen like Tomales Bay Capital with the founder, Iqbaljit Kahlon. Just a few days after the completion of the merger and after a letter being sent to the Department of Defense and to the Pentagon by senators and committee members galvanising a response on Chinese investments in the firm, SpaceX went further telling Kahlon that his fund is barred from purchasing shares in the company, on which his business model depends. Soon after Kahlon returned $50 million to Leo Group, which filed a lawsuit against Tomales Bay Capital and the rest is a whole another story.

Beyond his economic ownership, Musk also exercises overwhelming governance control over the company. Prior to the xAI merger, Musk held roughly 80% of SpaceX's voting stock. When SpaceX goes public, its SEC filings are expected to include a dual-class share structure that will allow him to maintain outsized voting control over the company's strategic direction, executive compensation, and capital allocation, regardless of his exact economic ownership.

The transaction was executed as an all-stock merger. Shareholders of xAI, and respectively X, received SpaceX stock through a 0.1433 exchange ratio. This "Mergers & Musk" approach allowed for the consolidation of assets without a massive cash outlay, though it effectively transferred the "burn" of Musk’s newer ventures (i.e. xAI) onto the SpaceX balance sheet. Furthermore, this makes the firm an extremely diverse value creation entity, which could prove challenging as the board will have to oversee a wide range of products, from orbital launch vehicles to social media content moderation, altogether, while the concentration of authority increasingly revolvesaround Elon Musk.

Cash or No Cash - Liquidity Risks

The SpaceX-xAI merger as an all-stock transaction was tax-efficient, which prevented capital gains tax to occur, but it introduced significant liquidity risks. xAI burns through around $1 billion per month prior to the merger, which is a massive cash drain. This means that SpaceX has to always have the liquidity factor in check if it ever plans something big, which is in fact what the IPO is. But liquidity is not only about the company, but also about the investors. Whoever wants to purchase SpaceX stocks pre-IPO on the secondary markets will have to accept strict illiquidity. Such shares could often be purchased and held through by SPVs instead of a direct ownership, and buyers will be subject to a 90- to 180-day lockup period following the IPO, which means that early investors will have to weather the post-IPO volatility without being able to sell, meaning the traditional "pre-IPO premium" may be minimal or even negative.

There is an inherent tension in the combined entity's free cash flow. Returning to SpaceX, Starlink serves as the “cash cow” making the whole consolidation possible, on the back of which revenue the xAI-burner and SpaceX’s own starship highly capital-intensive and volatile development could continue to operate. In 2025, the revenue of Starlink was $10 billion with 10 million subscribers, roughly 70% of the $15-16 billion of revenue generated by SpaceX as a whole. By year’s end it is expected for Starlink to achieve around 16.8 million subscribers with the revenue of SpaceX jumping to $20 billion with an EBITDA of $14 billion. Analysts note that Starlink’s recurring, high-margin revenue is the thing that makes SpaceX's astronomical valuation defensible, or does it?

In a highly unusual manner designed to reward retail investors for their hype, SpaceX plans to allocate up to 30% of its IPO shares to the general public, which is unprecedented for a company of this size and three times the Wall Street average for large IPOs. The usual free float allocation around a company’s IPO is between 10% and 20% of total equity with lower free float incurring higher price volatility due to restricted supply. Conversely, people would think that a higher free float of 30% is a great thing, though in highly volatile situations such as an IPO, it could trigger rapid price spikes and crashes as retail investors rush on what is “hot” until it is “not”. Musk could think that in the long term this could guarantee price stability, but for the short-term it is a huge gamble.

With a cashflow supposedly secured, the company could move to its core business operations, but there is no such thing as a free lunch, which brings us to the point of capital expenditure (CAPEX). SpaceX, having enormous capital requirements and an aggravated balance sheet after the merger, has a lot to balance on its plate. xAI was already facing massive expenses for terrestrial data centers, high-end AI chips, and energy, which is not made easier with Musk’s vision of “orbital data centers” to bypass the power grid limitations on Earth. Such investments would have to further cover specialized radiation-hardened GPUs, complex thermal radiators to reject heat in a vacuum, and immense solar arrays. Simultaneously, SpaceX is pouring billions of dollars into terrestrial infrastructure, including constructing massive new "Gigabay" manufacturing and integration facilities in both Texas and Florida to dramatically increase Starship production. This could prove more than the company could chew if the IPO does not go well.

This is why the valuation of the company matters. Higher valuation means a more stable debt-to-equity ratio. The Sum-of-the-Parts (SOTP) Disaggregation method could be a great method of reviewing the valuation of the conglomerate as it disassembles it into distinct business units, valuing each separately based on its unique growth, risk, and industry, then summing them to find the total EV, i.e. enterprise value. We could break it down to the $1 trillion valuation of SpaceX and the $250 billion one of xAI respectively to achieve the combined value of $1.25 trillion. Despite that it is important to point out that SpaceX is a market leader generating $15-16 billion in revenue, while xAI reportedly consumed $7.8 billion in the first nine months of 2025 alone, averaging a loss of $28 million per day.

Now that is what we could call “too hot”.

The Strategic Private-to-Public Bridge

Another interesting thing about the SpaceX IPO is its “controlled labs”, i.e. the private secondary markets. The conglomerate has effectively utilized private equity channels to “pre-clear” its aggressive valuation of $1.75 to $2 trillion amongst institutional investors before hiking its valuation through the reach of the public. Through platforms like Forge Global, EquityZen, and Hiive, accredited investors and institutions have been trading SpaceX shares, effectively establishing a strategic bridge between its private valuation and initial public offering.

In December 2025, SpaceX executed an internal tender offer (share sale) that priced its stock at $421 per share, effectively doubling the company’s valuation to $800 billion, at which valuation surpassed the combined market capitalization of the United States' six largest defense contractors, including aerospace giants like Boeing, Lockheed Martin, RTX, and General Dynamics. The December tender offer also served as a major pricing benchmark for investors seeking pre-IPO exposure, though financial analysts and outlets like Bloomberg have used the $800 billion figure from the December tender offer as the realistic baseline valuation for SpaceX's standalone assets, rather than the $1 trillion internal valuation claimed by the company later on during the merger. Since the $421 per share mark was established, the hype surrounding the company's upcoming IPO has driven shares substantially higher on secondary markets like Forge Global and Hiive, where they have recently traded between $527 and over $832 per share. That tender offer also served as a liquidity gateway for employees and early investors to leave before the IPO so they could cash out their gains.

Another key point to mention is the “Musk risk” as SpaceX’s reputation is tied to Musk’s reputation and vision. Musks leads a number of companies such as SpaceX (now together with xAI and X respectively), Tesla, The Boring Company, and Neuralink and if any event reduces his involvement, such as health issues, legal troubles, politics or other “excursions”, this could create massive uncertainty. His recent involvement in DOGE (Department of Government Efficiency) as well as his increased political polarization have had serious public backlash and the boycott of Tesla, which crashed its stock price by 45% after its December 2024 high. While the status of SpaceX as critical infrastructure insulates it from public boycott somewhat, Musk’s vocalism invites unwanted friction with regulators and politicians.

With geopolitical tensions and the macroeconomic outlook especially regarding the war in Iran, the need for air defense, and the US government request to Congress for a $200 billion military budget extension, SpaceX could reap benefits from the further involvement of its Starshield Programme, missile tracking, and secure communication. Nevertheless, SpaceX and especially Starlink is deeply exposed to geopolitical dynamics. Starlink's global involvement makes it subject to regulatory approvals in every jurisdiction, as some nations have already restricted or banned the service due to tensions with the United States.

Are these just minor setbacks, though, as many focus on what is up for grabs after the Mergers & Musk deal?

Intelligence-Led Consolidation or the Lack Thereof ?

Rockets, satellites, AI, media. This is what SpaceX offers now. An interesting claim for "the most ambitious, vertically integrated innovation engine on and off Earth", which could prove a unique strategy for a space-focused market leader in the realm of rocket and satellite creation. However, many analysts and minority shareholders call this merger an instant bailout for xAI instead of a rational intelligence-led consolidation. Moreover, critics say that the merger was just so that xAI could launch orbital data centres off Earth using SpaceX’s rockets, but instead of partnering with SpaceX, all of the aggravation from xAI was laid upon SpaceX’s balance sheet with the “vertical integration” as an excuse to boost valuations and save a “drowning man”.

On the positive side of things, if we move on from the financial motivations, SpaceX has already begun rapidly deploying AI capabilities within its operations such as in the integration of neural networks into Starlink’s satellite routing, advanced satellite management, automated anomaly detection, predictive maintenance, AI driven Starlink customer support, advanced rocket flight scheduling and rocket trajectories.

Not only have they already started with the architectural synergies, but also upcoming plans have been drafted for a radical AI integration, named “Orbital Intelligence”, which is the idea of moving the most demanding AI computations off-planet. Key elements include the launch of the aforementioned orbital data centers as well as “Grok-Sats” (heavy, GPU-laden satellites, i.e. satellites aimed at moving data processing and AI inference from terrestrial data centers to low Earth orbit), the use of NVIDIA’s radiation-hardened Blackwell chips, the improvement of Starlink’s connectivity and data-gathering abilities for orbital AI training, and the powering of deep space AI implemented in AI-guided satellites for future bases on the moon and on Mars.

This could all seem sci-fi, but the AI integration in the intelligence-led consolidation is real, despite questionable financial motives. But what about the buy-and-build part of the equation?

Playing Monopoly or Smart Vertical Integration

As everything in capitalism, the endgame is always a high-stakes game of chess. We believe that “they” just sit up there and do nothing, while collecting billions, but the reality is that it ends up in a game, where your compounding strategy and adaptability redefine what is possible. Not always the cleanest execution, but a neat one. For now the odds are in Musk’s favour despite a lot of, to put it bluntly, questionable actions. The Buy-and-Build strategy is traditionally mentioned when discussing horizontal integration of smaller competitors but in some cases it is also considered when talking about vertical integration as in SpaceX’s situation. It represents a radical change from usual aerospace business models and ecosystems as it bets heavily on telecommunication, integration of artificial intelligence, and operational efficiency in the hardware build of rockets, satellites, and AI infrastructure.

Is SpaceX “TBTF”? A bold statement, on which we could bet that Musk would mention if things turn south for the IPO. Some of SpaceX’s main competitors are launch providers (Blue Origin, Rocket Lab, United Launch Alliance), satellite internet (Amazon's Project Kuiper and OneWeb), and, obviously, artificial intelligence (OpenAI, Anthropic, Google DeepMind, etc.). This may sound like a lot, however none of these integrate into each other to the extent of which SpaceX does. The competitive advantage is deeply structural as it could offer rapid reusability and operational efficiency when discussing rockets and satellites with the company holding over 80% of the U.S. commercial launch market.

On the competitor landscape SpaceX was dominant even before the merger with xAI and the pre-IPO landscape is favourable for Musk as SpaceX’s main competitors are significantly behind in the race for the best launcher, satellite, or space communication technology. An example could be that Blue Origin, as SpaceX’s main competitor has completed one successful propulsive landing, where in comparison SpaceX has completed over 500, enabling it to launch a rocket roughly every two days with turnaround times as short as three weeks. This leaves Musk with significant leverage as investors price SpaceX with a massive “monopoly premium", reflecting its near-total control of the low-Earth orbit market. This allows in some ways to justify the astronomical valuation expectations as analysts see, for instance, Starlink as the global telecommunications monopoly with a rockets division. And the cherry on top could be that SpaceX operates in an insulated critical-global-infrastructure market, which shields it from consumer boycotts, brand risks, or public outrage regarding Musk’s political actions.

However, not every consolidation could be framed as successful before we take a look at the synergies between the buyer and the seller.

Synergies for Lovebirds

A bloat in the valuation of around $200 billion. Are those synergies or just a really expensive marketing trick, which could pass the financial pain down to investors? The merger of SpaceX and xAI promises an “innovation engine” with intelligence-led consolidation, which could unlock a massive ecosystem of cross-disciplinary across various segments and structures of the business. It promises a significant boost in revenue as the early growth rate of SpaceX was considered around 33%, where the figure for 2026 lies around 50%, which is approximately a 50% increase from the average itself.

Nevertheless, integration happens rapidly with AI becoming an integral thread between rockets and satellite broadband. The X platform served even prior to this merger as the primary distribution hub and real-time data source for training xAI’s Grok models, while Starlink further provides the global backhaul necessary for off-planet inference also including data from its capture into the training of Grok. Musk’s visionary heavy, GPU-laden satellites, Grok-Sat, will happen exactly through the operational integration of xAI and SpaceX, which will be revolutionary for the “off-planet computing” just as his idea for orbital data centers.

A significant part of the UVP of SpaceX is the operational efficiency. With further AI integration this model could continue keeping up with the demand and pace of the AI era. Examples could be launch and flight logistics through AI planning systems, autonomous satellite management via AI-driven anomaly detection, and the development of AI copilots and advanced decision-support tools to assist astronauts during crewed missions. However, everything comes at a cost. This could drive up spending immensely just as the previously mentioned extraterrestrial AI infrastructure. Sometimes these opportunities could be quantified and implemented too early with no realistic development in the immediate future with hidden risks but on the other hand with immediate benefits for the management and majority shareholders.

The buy-and-build vertical integration strategy brings many assets and products under development under a unified corporate structure with shared R&D labs, which in turn reduces the transaction costs and friction of negotiating strategic partnerships. Despite that, analysts note that these structural savings will be highly necessary and need to be substantial as most of those synergies will have to offset the heavy insurance premiums and latency penalties associated with launching and operating space-based computing infrastructure.

What truly makes the headlines though are the revenue synergies. The integration creates proprietary data loops and guaranteed distribution channels that competitors cannot easily replicate with Grok benefiting the most. Through this merger xAI gains immediate, massive distribution channels across the Musk ecosystem, including Starlink and potentially Tesla outside of its integration already in X. This also creates the possibility of new markets, such as AI-managed satellite services for third parties, on-orbit processing of Earth observation data, frontier AI services for remote regions.

After all, does this sound like a $200 billion immediate EV increase or just a non-existent synergy ramp, which could prove the expectations tricky to fulfil?

Conclusion: “A Behemoth on the Way”

At its current stage of IPO preparation it could be firmly stated that the $1.75 trillion valuation of SpaceX is ambitious, let alone the $2 trillion one. What we discussed here measures just how realistic this set target could prove. The state of SpaceX is one with a focus on compounding growth with tech integration as a core principle, which could be the king maker of this roadshow. With a valuation of around $350 billion in 2024 and a target for $1.75 trillion in just 18 months, SpaceX tries to redefine the meaning of the word “scalability” and now it wants to prove itself to the market with some unorthodox gestures of appreciation for the public such as a 30% free float for the IPO release and the secondary market trading by private equity funds and SPVs.

What we could truly call a “behemoth” is on the way. And it is coming fast. It will be the first of the three mega IPOs together with OpenAI and Anthropic and will start one of the biggest on-release trading waves on the day of the IPO. Until then Musk will have played his hands well with the xAI integration and the $50 billion in investment, which he plans to raise by then. The synergies will have to be in a rapid process of realisation due to the time pressure and incoming volatility of the company on the day of the IPO, so that SpaceX could mostly live up to them, as it focuses on continued intelligence-led consolidation with the already acquired assets and liabilities from xAI.

Strong financials due to projects such as Starlink are not the only thing, which is required by SpaceX. Despite a massive “monopoly premium” and a partially insulated business from the consumer sentiment, the high free float could trigger the exact opposite and what is a strategy for long-term stability could prove the exact opposite. The “Musk Factor” and controversies should always be kept in mind, especially around institutional investors regarding Chinese investments threatening U.S. national security and involving SPVs in the Cayman Islands and the British Virgin Islands.

All in all, there is no perfect firm and there is certainly no perfect time for a risk-free IPO. The pure idea of the merger between SpaceX and xAI just months before the initial public offering may sound sketchy, but the true capabilities of such companies working as one is just fascinating, particularly when thinking about all the possibilities it may unlock. The real question is whether the intrinsic value of the goods and services offered are priced correctly in relation to the firm as a whole. In some ways it may be true that SpaceX could get to a valuation of $1.75 trillion, but in this case the real risk factor is time. With all that the company now has to offer it may indeed come a day when the intrinsic value or at least the overvalued version of it gets to this point. But whether this day will be the day of the IPO of SpaceX, only time will tell.

Bibliography

“Analysis-Blockbuster SpaceX Listing Could Suck the Oxygen out of Fragile IPO Market.” Investing.com, 7 Apr. 2026, www.investing.com/news/stock-market-news/analysisblockbuster-spacex-listing-could-suck-the-oxygen-out-of-fragile-ipo-market-4599979. Accessed 16 Apr. 2026.

Brooks, Sophie. “Inside Elon Musk’s Strategic SpaceX-XAI Merger.” Businesschief.com, Bizclik Media Ltd, 4 Feb. 2026, businesschief.com/news/inside-elon-musks-strategic-spacex-xai-merger. Accessed 16 Apr. 2026.

Coach, The Startup. “SpaceX XAI Acquisition: Elon Musk’s Vision for Vertical Integration of AI and Space.” TorontoStarts, 3 Apr. 2026, torontostarts.com/2026/04/03/spacex-xai-acquisition-analysis/. Accessed 16 Apr. 2026.

Down, Aisha. “Musk’s SpaceX Courts Retail Investors as It Aims for Record-Breaking Stock Market Flotation.” The Guardian, The Guardian, 7 Apr. 2026, www.theguardian.com/science/2026/apr/07/spacex-2tn-valuation-retail-investor-ipo-elon-musk. Accessed 16 Apr. 2026.

Elliott, Joshua Kaplan,Justin. “How Elon Musk’s SpaceX Secretly Allows Investment from China.” ProPublica, 26 Mar. 2025, www.propublica.org/article/elon-musk-spacex-allows-china-investment-cayman-islands-secrecy.

“Elon Musk Net Worth 2026: $811B Fortune, SpaceX IPO & Path to $1 Trillion.” TECHi®, 7 Apr. 2026, www.techi.com/elon-musk-net-worth/. Accessed 16 Apr. 2026.

Erwin, Sandra. “SpaceX, ULA, Blue Origin Win $13.7 Billion in U.S. Military Launch Contracts through 2029.” SpaceNews, 4 Apr. 2025, spacenews.com/spacex-ula-blue-origin-win-13-5-billion-in-u-s-military-launch-contracts-through-2029/.

“Even Starlink Wants Your Data for AI Model Training. How to Opt Out.” PCMag UK, 16 Jan. 2026, uk.pcmag.com/ai/162633/even-starlink-wants-your-data-for-ai-model-training-how-to-opt-out. Accessed 16 Apr. 2026.

“GDP by Country (2025) - Worldometer.” Worldometer, 2025, www.worldometers.info/gdp/gdp-by-country/?source=imf®ion=worldwide&year=2025&metric=nominal.

Grush, Loren, and Edward Ludlow. “SpaceX Sets $800 Billion Valuation, Confirms 2026 IPO Plans.” Bloomberg.com, Bloomberg, 13 Dec. 2025, www.bloomberg.com/news/articles/2025-12-13/spacex-sets-insider-share-deal-at-about-800-billion-valuation. Accessed 16 Apr. 2026.

“How to Own SpaceX before the $1.75 Trillion IPO.” Kevin Crowther | Top-Rated Financial Advisor in Dubai, UAE, 9 Apr. 2026, kevincrowther.com/news/spacex-1_75-trillion-dollars-ipo/. Accessed 16 Apr. 2026.

Jamali, Lily. “Musk’s XAI Buys His Social Media Platform X.” BBC, 28 Mar. 2025, www.bbc.com/news/articles/ceqjq11202ro.

Jennewine, Trevor. “Want to Own SpaceX Stock before Its Blockbuster IPO? Here Are 3 Ways Investors Can Buy Right Now.” The Motley Fool, 11 Apr. 2026, www.fool.com/investing/2026/04/11/own-spacex-stock-before-ipo-investors-can-buy-now/. Accessed 16 Apr. 2026.

Mac, Ryan, et al. “Elon Musk Merges SpaceX with His A.I. Start-up XAI.” The New York Times, 2 Feb. 2026, www.nytimes.com/2026/02/02/technology/spacex-xai-deal.html.

Morningstar, Inc. “SpaceX Officially Acquires XAI. Here’s How Elon Musk Justifies the Move.” Morningstar, Inc., 2 Feb. 2026, www.morningstar.com/news/marketwatch/20260202434/spacex-officially-acquires-xai-heres-how-elon-musk-justifies-the-move. Accessed 16 Apr. 2026.

“Musk Makes Starlink IPO Guarantee to Small Investors.” Light Reading, 2020, www.lightreading.com/wifi/musk-makes-starlink-ipo-guarantee-to-small-investors. Accessed 16 Apr. 2026.

Musk, Elon. “Elon Musk Prepares SpaceX IPO Valued at More than RTX, Boeing, Lockheed Combined.” Sahm, 2025, www.sahmcapital.com/news/content/elon-musk-prepares-spacex-ipo-valued-at-more-than-rtx-boeing-lockheed-combined-2025-12-15. Accessed 16 Apr. 2026.

Petrova, Magdalena. “How the U.S. Space Industry Became Dependent on SpaceX.” CNBC, 24 Aug. 2025, www.cnbc.com/2025/08/24/spacex-how-us-space-industry-became-dependent.html.

Pratley, Nils. “Elon Musk Is Taking SpaceX’s Minority Shareholders for a Ride.” The Guardian, The Guardian, 3 Feb. 2026, www.theguardian.com/business/nils-pratley-on-finance/2026/feb/03/elon-musk-is-taking-spacexs-minority-shareholders-for-a-ride. Accessed 16 Apr. 2026.

Saha, Sulagna. “SpaceX Targets Record IPO, Riding Starlink’s Explosive Growth.” RCR Wireless News, RCR Wireless, 6 Apr. 2026, www.rcrwireless.com/20260406/network-infrastructure/spacex-files-for-ipo-starlink-is-why-it-matters. Accessed 16 Apr. 2026.

“SpaceX.” SpaceX, www.spacex.com/updates.

“SpaceX IPO: Investment Opportunities & Pre-IPO Valuations - Forge.” Forgeglobal.com, 2024, forgeglobal.com/spacex_ipo/. Accessed 16 Apr. 2026.

“SpaceX-XAI Merger: Corporate Governance and Valuation Impact - AI CERTs News.” AI CERTs News, 10 Feb. 2026, www.aicerts.ai/news/spacex-xai-merger-corporate-governance-and-valuation-impact/. Accessed 16 Apr. 2026.

Subramanian, Pras. “Why Starlink Is so Important to SpaceX’s IPO.” Yahoo Finance, 14 Apr. 2026, finance.yahoo.com/sectors/technology/article/why-starlink-is-so-important-to-spacexs-ipo-174446711.html?guccounter=1. Accessed 16 Apr. 2026.

“The $1.25 Trillion Gymnastics: What the SpaceX and XAI Merger Teaches Every Business Owner.” Carbon Law Group, 11 Mar. 2026, carbonlg.com/podcast/spacex-xai-merger-tax-free-reorganization-los-angeles/. Accessed 16 Apr. 2026.

The Chronicle-Journal. “The $1.25 Trillion Frontier: SpaceX and XAI Merge to Create “Orbital Intelligence” Powerhouse.” The Chronicle-Journal, 9 Apr. 2026, markets.chroniclejournal.com/chroniclejournal/article/marketminute-2026-4-9-the-125-trillion-frontier-spacex-and-xai-merge-to-create-orbital-intelligence-powerhouse. Accessed 16 Apr. 2026.

“Welcome to Zscaler Directory Authentication.” Satellitetoday.com, 2026, interactive.satellitetoday.com/via/january-february-2026/the-key-questions-for-a-potential-spacex-ipo-in-2026-analyst-roundtable.

All data used in this article is derived from publicly available institutional reports and industry analyses.

This article is for informational purposes only and does not constitute investment advice.

Mihail Gaydarov

Founder & Chief Financial Analyst.

Spas Arsov

Financial Analyst, M&A Specialist.

Alexandria Chaliovski

Financial Analyst, Article Editor.

The Financier Review

© 2026 The Financier Review. All rights reserved.