From Phone Batteries to The Largest EV Manufacturer In The World - The BYD Motor Company.

Photo by Michael Förtsch on Unsplash

Article Authors: Mihail Gaydarov, Nikolay Marinski.

Wang Chuanfu and the Manufacturing Mindset

Wang Chuanfu was born in 1966 into a poor family with 8 siblings. After the death of his parents, he was raised by his elder brother and sister while attending high school. After that, he went on to study metallurgical physical chemistry at the then Central South University. Following his graduation in 1987, he earned a master's degree in 1990 from the Beijing Non-Ferrous Metal General Research Institute. There was his first entrepreneurial experience, when in 1993 the Institute established a battery company called BAK Battery and given Chanfu’s academic background in related fields, he was appointed as the general manager. Through this opportunity, he gained experience in business management and battery manufacturing. Anticipating an industry shift as Japan phased out nickel-cadmium batteries and moved to lithium-ion, Wang Chuanfu saw a gap in the market with the booming mobile phone and cordless device market in China still requiring that technology. He left BAK Battery in 1995 to found his own company, BYD (Build Your Dreams) Company, at 29 years old, with his cousin Lu Xiangyang, who was a key early investor.

After managing to secure a starting capital of around CN¥ 2.5 million ($300,000 at the time) Wang Chuanfu started operations with a team of 20 people. Because of the limited capital, BYD had to implement an alternative manufacturing approach, incorporating more manual labour, contrasting the capital-intensive, highly automated approach adopted by most companies in Japan. Combined with the in-house manufacturing of fundamental machinery, this allowed BYD to cut unit costs by around five or six times compared to Japanese competitors. The company also developed advancements in battery technology, which improved performance.

Considering the socio-economic conditions of the country, it is very important that we perceive the heritage of the company through the prism of the business environment in China during the 1990s. A crucial element for the success of BYD was the rapidly growing industrial segment of the Chinese economy. If we were to pinpoint an exact event that caused this trend towards privatisation of state-owned enterprises was the transition of the country to a “socialist market economy”, following Deng Xiaoping's southern tour. Upon the military crackdown in Tiananmen Square in 1989, the Chinese statesman attempted to resume the opening of China to the rest of the world.

Manufacturing Under Constraint: How BYD Became So Efficient.

While the business model of the company was rather simplified at the time, it was a cornerstone to the giant’s present-day success. Firstly, while labour in China was extremely cheap at the time, we have to find out why that was the case. During the 1990s, the incredible push towards industrialization and expansion of China to the rest of the world, while receiving considerable foreign direct investments, resulted in over 30 million workers being laid off. The primary cause of this was the shift from a state-planned labour force to one that caters to the needs of now privately owned enterprises. Distorting the labour market by dismantling many of the SOEs (State-Owned Enterprises), meant that the principle of the “Iron Rice Bowl” or in other words, lifelong employment was not the case anymore. As a result, many people did not have an occupation and, even more so, were in desperate need to find jobs to feed their families. Accompanying the already poorly valued labour of the average worker resulted in a labour force that was easily affordable for new businesses like BYD.

On a similar note, the reason why foreign competitors did not have a chance to compete with BYD is that, at the time, the polarization of wages around the world was very significant. The average salary of a Chinese worker during the 1990s, following the dismantling of many SOEs, was in the range of $50-$100 per month for urban workers. If we were to compare with other major global powers, the wage pay for an average worker (in the same field) in the United States was 10x-50x the Chinese norm. Even more closely, the most significant competitors of BYD, the Japanese, had a labour force that was nearly three times as expensive as the one in China. So instead of relying on expensive, capital-demanding machinery, BYD’s manufacturing process was built around labour-intensive work and manual processes.

Furthermore, another key aspect for the early success of the battery producer was their levels of vertical integration. The process of vertical integration is a business strategy where the company owns its production chain and the factors of production related to it - protecting itself from external shocks to production factors. Many sources, including BYD’s own story report, suggest that the company was so vertically efficient that almost all of their production steps were made, sourced or completed in-house. This meant that BYD was practically immune to external supply shocks, allowing the enterprise to drown their competitors in low pricing, while they relied on volumes to generate thin profit margins.

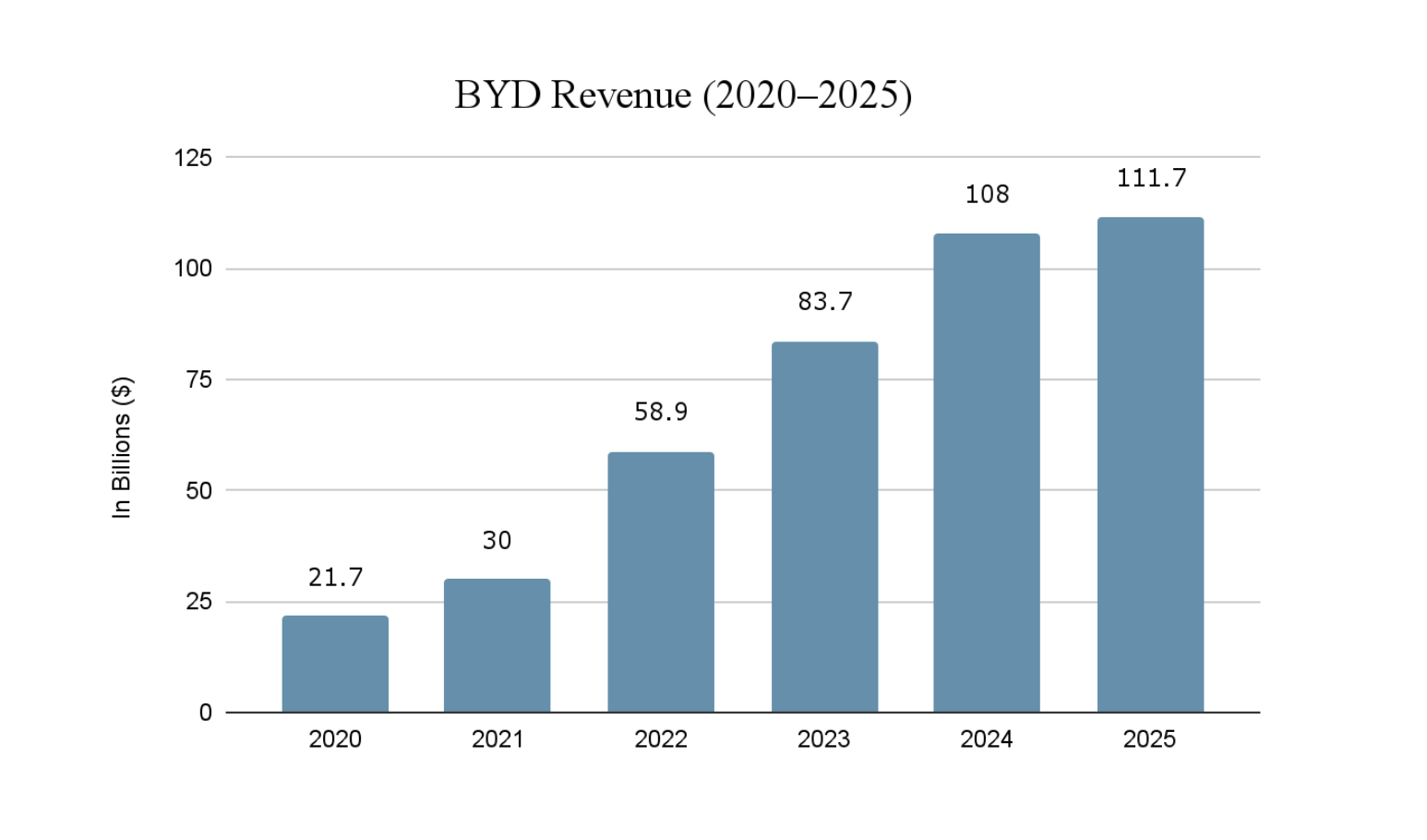

If we look at the story of the giant in more recent days, BYD reported over 30 industrial parks, covering a staggering 18 million square meters across almost every continent on the planet. The massive R&D hubs for the company in Pingshan and Shenshan allow for the integration of manufacturing and housing at the same time. In 2025, BYD generated a revenue of ¥803.96, which equates to $117.8 billion. In comparison, Elon Musk’s Tesla generated $94.83 in revenue for the same time period. What is more important than the colossal revenue numbers is the slowing growth of the Chinese EV giant. Reports from Reuters show that BYD experienced its weakest pace for growth at 3.46% in six years.

Perhaps the most notable question we can deduce here is to what extent can efficiency be profitable and at what point does it stop resulting in effortless profit expansion. The efficiency of the company is quite clearly evident, but does that mean it will create incremental profit for the future, and are there any external factors that have affected the slowing growth?

Imitation Over Innovation - The BYD Model.

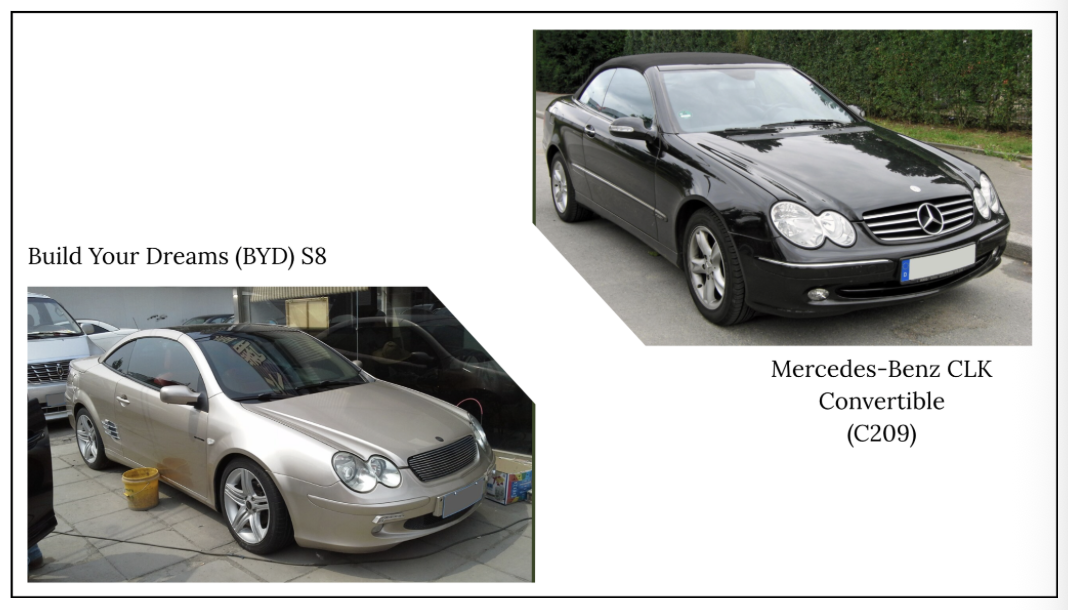

As well as taking advantage of the economic situation during the 90s the Chinese EV corporation has been accused numerous times of copying designs of other car manufacturers. Perhaps the most prominent culprits for this imitation strategy are the early 2000s vehicles. Models like the BYD F3 (2005), resembling a Toyota Corolla, and the BYD S8 in 2007, being a Mercedes-Benz CLK convertible. Other models like the BYD F3 were compared by the industry as the Chinese Toyota Corolla and Honda Fit.

At first glance, these accusations do have ground due to the fact that the aforementioned vehicles have a striking resemblance to their respective German and Japanese counterparts, but there is a much deeper reason that plainly disinterests in original design.

More importantly, the visual similarities between these models is the fundamental state that the company was at. BYD was just beginning to enter the manufacturing of vehicles, and although they had experience in the production of batteries it was not the case for vehicles.

Arguably, the strongest claim that we can deduce from these rather questionable business and design practices is that BYD was still in their stage of understanding the car market and the know-hows of manufacturing cars. And indeed so, the claim that all early models of the BYD could be labeled as “fast follower” behaviour also has ground. But the most important distinction to be made here from the absorption of car design ideas and models, coupled by very low production costs and aggressive scaling, gave the brand an opportunity to create a future for their distinction in the upcoming decades, not set them as design followers. Lower R&D costs meant that the company had the ability to produce at scale and stash on capital that can be later used for the development of newer technologies.

During the joint development of the Toyota-BYD EV project, Japanese engineers from Toyota shared with the press that they were absolutely fascinated with the company’s speed and willingness to redesign parts at need, even in the late stage of model development. The recognition that renowned engineers from Toyota gave to BYD materialized the move of the Chinese company from an imitator of design to a very powerful engineering organisation.

Therefore, we could argue that the early-stage imitation practices of BYD were the root cause of a few external factors. Firstly, the lack of capital meant that BYD did not have lots to experiment with design, so they stuck with very proven and effective models to “borrow” from. Over the years, this allowed the company to operate on thin margins and very low production costs, which in turn gave path to a future of expansion and allowed the brand to become a pioneer in the field of electric vehicles for the future.

Many other analytical sources have regarded the company as the Chinese copycat of German and Japanese vehicles, but we do not believe that BYD resorted to these practices out of laziness towards design, but a choice that demonstrates more of a strategic decision that allowed them to expand in the future and as of today, be one of the largest car manufacturers in the world.

State Capitalism in Motion.

Now, coming onto the less glamorous reason for the success of the Build Your Dreams car company. Or, in specific terms, the involvement of the Chinese state in the market for the manufacturer.

Effective, since the 30th of October 2024, the Chinese giant was subject to countervailing duties or in simpler words, tariffs imposed by the European Commission. Following an anti-subsidy investigation, there was a definitive conclusion that the Chinese EV battery chain has benefited from an unfair amount of government subsidies. With that said, BYD was hit by a 17% tariff on every imported good to the European Union. Even so, other Chinese EV manufacturers were hit with higher tariffs, like 18.8% for Geely and 35.3% for SAIC. These countervailing duties will be imposed for a time period of five years and will affect every Chinese Battery Electric Vehicle (BEV).

Subsequently, the EU launched the investigation due to the large suffocation of the European market with Chinese cars, which at the time were mostly performing significantly better than any other European BEV. The case was against the entire BEV value chain, not specifically with BYD, but it is important to note that this trade-distorting subsidisation created a very substantial threat of material injury to EU BEV vehicle producers.

Of course, the exact amounts of subsidies that the Chinese manufacturers received are estimates, but we have compiled a callout with the main hard numbers on the matter: (Note: These are direct subsidies to BYD).

~$3.7 billion in direct subsidies→ 2018–2022 total

$2.1–2.2 billion in 2022 alone→ peak year of support

~$309 million in 2023→ sharp drop as China began phasing out subsidies

~$1.4 billion in 2024 (grants)→ support didn’t disappear, just changed structure

2025: ¥12.5 billion ($1.7bn) in subsidies→ rising again amid price wars

Albeit, the interpretation to be made here is that subsidies are definitely not linear and that spikes occur mostly when policy priorities shift. With a figure of about $2.2 billion, 2022 was the most highly subsidised year for BYD. Following 2023, the Chinese state transitioned into more of a targeted and indirect support through government contracts policy-directed procurement and industrial mandates, rather than direct support.

If we consider the relative size of the revenues that BYD generates, we receive the following figures:

2022 Subsidies ≈ 3.5% of BYD’s Year Revenue.

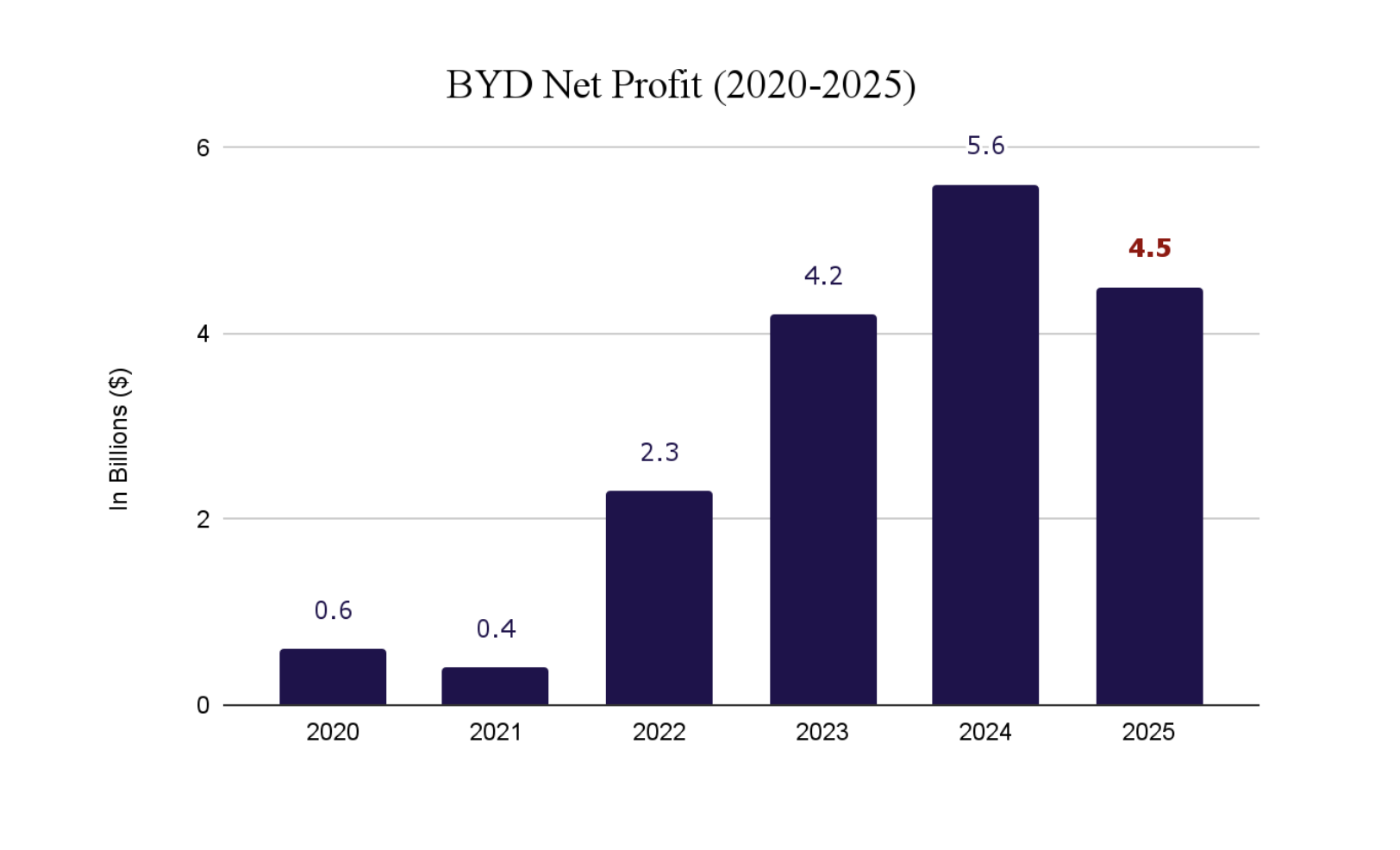

2024 Subsidies ≈ 26% of BYD’s Net Profit.

2025 Subsidies ≈ 3.5% of BYD’s Net Profit.

We can make the implication here that the subsidies the company received are not the core drivers of revenue, but they are significant margin stabilisers. The ability to operate on thin margins and be extremely competitive price-wise allows companies to engage in price wars. Such subsidies also act as a downside buffer during competition. Therefore, we can conclude that these subsidies are less of a growth engine, but more of a strategic support in the game of Chinese manufacturing domination on the European market.

Selling at a Near Loss Makes you a Winner.

As we have already seen through the history of the automaker, BYD has consistently been resorting to budgeting and decreasing the cost of production in order to compete price-wise with their rivals. From the imitation of other popular European and Japanese car designs to other cost-cutting measures it is in the DNA of the company to generate thin profit margins and rely on sales volume to make up for future profits and development.

Despite that, in 2025, net profit fell 19% to ¥32.6 billion, but at the same time revenue rose by 3.5%. Therefore we can make a safe assumption that the thin profit margins that the company operates on, combined with the sanctions that the EU has imposed on the Chinese EV giant are taking effect on the balance sheet front. Further, sources like Reuters report that this is BYD’s first annual profit decline in 4 years. What caused the decline is the domestic price war and the shrinking margins that the company is experiencing.

In addition to the crumbling overall profits, BYD’s specific profit from cars took the largest hit. Last year the company suffered a 20.5% reduction in profits from vehicles, clear evidence that the aggressive pricing is compressing financials materially. As well as the financials it is important to note that sales targets also play a crucial role in understanding the financial situation the company is in. 61% of domestic sales come from models below $22,000, which in turn leaves the company vulnerable to subsidy changes and price competition.

On the bright side, sales overseas aided the damage that was caused to the company by EU policy makers. Results from 2025 state that overseas sales accounted for 22.7% of total sales and carried a 19.5% gross margin, which is a higher figure than the one from the previous fiscal year.

If we have to sum up the entirety of the situation for the BEV car manufacturer we can state that BYD is sacrificing their margins to hold their scale and share of the EU market. More importantly, how long can they really continue to withstand the hit from compressed profit margins? Also, considering the imposed tariff of 17% of BEVs, it is a matter of time until even more significant financial effects take place on the profit front of the company.

The Emerging EV War: From China to Europe.

China’s electric vehicle expansion is no longer a domestic industrial policy experiment—it is now a direct challenge to Europe’s automotive core. That matters because BYD is not being punished as the worst offender. It is being treated as the most competitive subsidised player: low enough tariff to remain aggressive, high enough to signal that Brussels sees its cost structure as politically and industrially threatening.

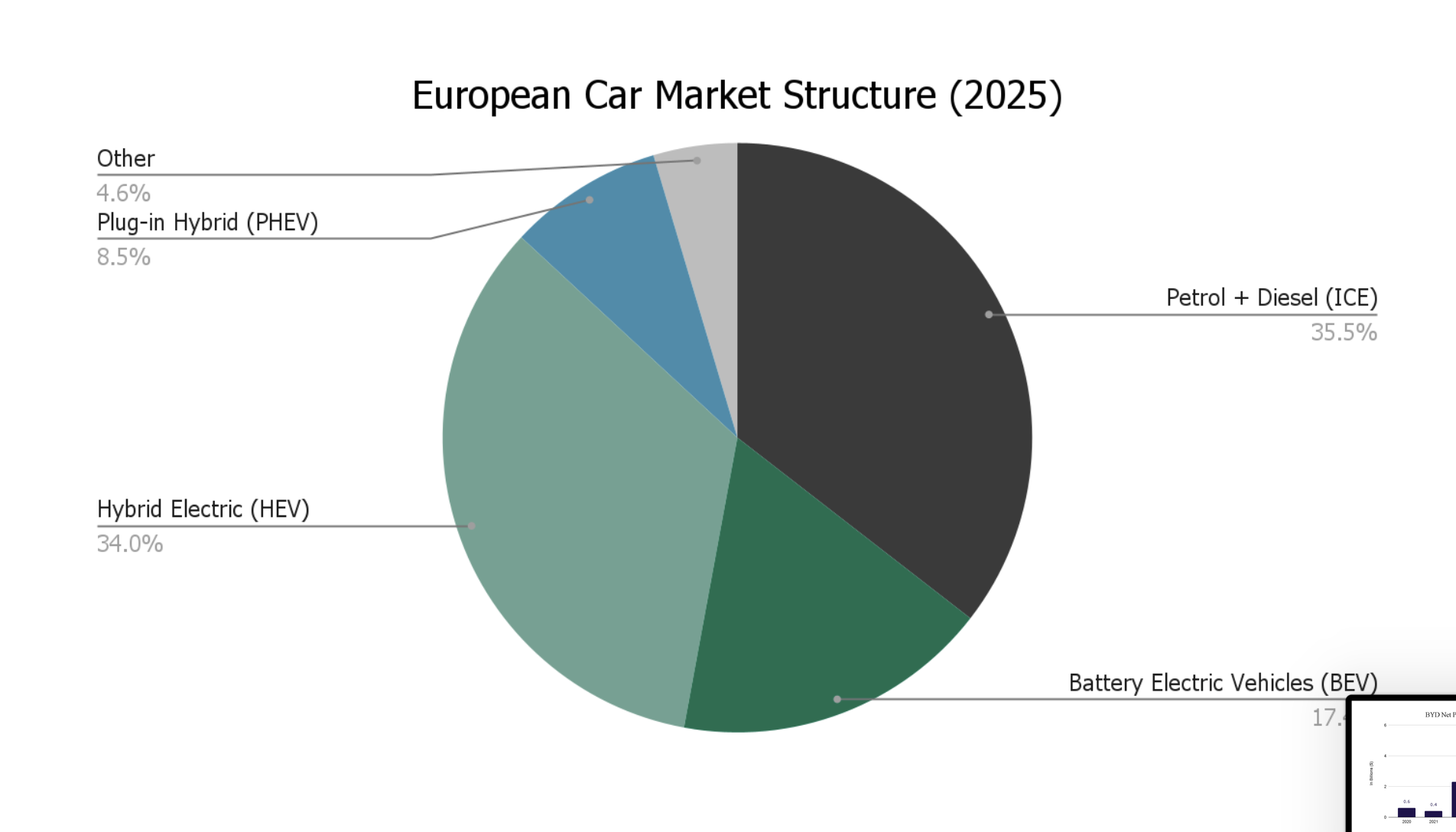

The EU’s worries are derived from the significant demand in the BEV market and the marginal replacement of traditional Internal Combustion Engine (ICE) vehicles. Where the Chinese come into play is taking an alarmingly large portion of the 17.4% BEV car market share and delivering on the growth of the market. In 2025 alone, the EU registered 1,880,370 Battery Electric Vehicles, accounting for the 17.4% market share, which in fact is up from 13.6% for 2024.

In parallel, as the EV market is growing, petrol and diesel vehicle share has collapsed from a combined share of 45.2% in 2024 to 35.5% in 2025. So at last, the issue is very simple. The structural shift of the European market towards electrification has given way to extremely competitive products from Chinese car manufacturers. And we have to consider that this is not a light matter, this is a fight over who captures the next industrial base and pioneers in the European auto sector.

The Cracks in BYD’s Business Mechanism

One of the main issues with BYD’s production strategy is that it heavily relies on growth and cash flow, however recent developments have put a strain on all the foundations, causing a series of strains that together have shaken the company’s finances.

It is also important to note that BYD’s numbers are the result of a period of short-term inflation caused by the expansionism of their strategy, hence the values are not the result of long-term and proven supply but rather short-term bulk sales.

The first shock came from the vehicles sold: initially the price was significantly cheaper than other competitors, but because of new tariffs, surges in raw material prices, and an increase in competition in the segment, meant the cost of a new BYD car is closer to the competitors’s. The market sector of the company is now saturated and new orders have slowed down, therefore the required high demand and volumes that made the model function are no longer met.

It is also important to note that BYD relied on longer periods to pay suppliers (127 days) in order to keep cash available. This is fundamental because the latter can be used to finance other operations, however new and tighter regulations on payback windows have compromised this strategy both in domestic and export markets.

This series of setbacks have led to clear signs of an internal shock that BYD hasn’t quite been able to contain yet, the company is structured to operate in a situation of constant growth, which is no longer the case. This has led to the first major workforce reduction of 10.2% in 2025, however even increased discounts weren’t enough to fix the issues, as net profit plummeted -18.97% in the same year. Indeed, as regulatory scrutiny tightens and growth begins to moderate, this mechanism becomes increasingly fragile. Slower sales cycles and compressed margins reduce incoming cash, while obligations to suppliers normalize, creating a potential working capital squeeze. In such an environment, scale no longer functions purely as an advantage, but begins to demand greater liquidity to sustain itself, exposing a financial vulnerability beneath BYD’s operational efficiency.

Another aspect that is not immediately conceivable from economic data alone is the fact that BYD “Created its own competitors”, their success in creating electric and hybrid vehicles has led to many other Chinese companies to invest into this sector, and many offer similar, better or cheaper products, reducing the company’s market share. Furthermore, the automaker had its initial international success because it was among the first Chinese manufacturers to export cars capable of competing with other more renowned European and Japanese automakers. While this worked in their favor as it brought more business, at the same time the success and fall of the myth of Chinese cars being low quality led domestic competitors to gain traction in the same countries.

Overall, BYD set its business model on overestimated numbers based on inflated short term data, this dynamic is further more complicated by the general crisis of the automotive sector, especially for EV’s, that has led to a lower volume of vehicles sold, which paired with increases in overall costs of production, limited financial options and tighter margins have put a strain on a system set on expansion, catching it at its most vulnerable state without a complete premeditated contingency plan.

Is There a Future For The Chinese EV Giant and What Kind of Future?

Well, the answer to this question is almost definitive considering the current state of the company. It is almost certain that the Chinese manufacturer has a future at least in the battery manufacturing business. Perhaps, the more objective question to ask here is: what kind of future can we expect for the company? Considering the public data provided by the company, as of today BYD is one of the largest EV and NEV manufacturers in the world. As mentioned prior, revenues for the previous year have exceeded ¥800 billion and there are very few reasons to believe that the company will halt growth from this point onwards. It would have to be subject to severe sanctions and regulations that might have the possibility of forcing the EV giant to leave the European market.

The bullish case for BYD can be identified through a few major factors, which mostly include production. As discussed, one of the cornerstones to the BYD business model are the high levels of vertical integration. Owning most of the production means towards manufacturing their final products reduces the dependency of the company on external suppliers, subsequently making BYD mostly immune to geopolitical shocks and shortage events.

The most likely future for the Chinese car manufacturer is the further expansion overseas, coupled with increasing local production in Europe. Also, the highly likely continuous support of policy-makers towards electrifying the consumer car park will support the expansion of the company. Potential trade agreements with the Asian market, inclusive of China to ease restrictions on the automaker, can be considered the biggest aid to BYD. Without tariffs “eating into” already thin profit margins a bright future for the giant is foreseeable.

On the contrary, we can argue that a bearish case is also a possibility for the company. From their historic practices of cost cutting and trying to be increasingly competitive on the market they might become a victim of their own business model. In a case where political barriers continue to be a factor and with the potential of increasing tariffs and restrictions in upcoming years, as more and more Chinese vehicles are suffocating European automakers, BYD might struggle to sustain itself on the European market. Other anti-business practices which include supplier finance constraints also have the chance to bring the company down. With extended periods where suppliers do not see payment for completed work, it might be the case that many do not cooperate and work with the Chinese EV giant. Without a doubt, the most important point to be made here is that the true state of the company remains unknown. Although the required data is publicly available, postponed accounting for debts towards suppliers perhaps do not show the entire story of the company and to what extent their indebtedness might prove to be the failure point of the machine that Wang Chuanfu created nearly 30 years ago.

Bibliography

BYD Company Limited. Annual Report 2025. Hong Kong Exchanges and Clearing Limited, 2025.

https://www1.hkexnews.hk/listedco/listconews/sehk/2025/0324/2025032401238.pdf

BYD Company Limited. “BYD Reports 2024 Financial Results.” BYD UK Media Centre, 2025.

https://bydukmedia.com/en/news-articles/byd-reports-its-financial-results-in-2024-revenue-hits-777.1-billion-yuan-up-23-year-on-year.html

International Energy Agency. Global EV Outlook 2024. IEA, 2024.

https://www.iea.org/reports/global-ev-outlook-2024

Rhodium Group. “China’s Electric Vehicle Industrial Policy.” Rhodium Group, 2023.

https://rhg.com/research/china-industrial-policy-evs/

Center for Strategic and International Studies. “China’s Electric Vehicle Industrial Strategy.” CSIS, 2023.

https://www.csis.org/analysis/chinas-electric-vehicle-industrial-policy

McKinsey & Company. “Automotive & Assembly Industry Insights.” McKinsey, 2024.

https://www.mckinsey.com/industries/automotive-and-assembly/our-insights

European Automobile Manufacturers’ Association (ACEA). “Key Figures: Electric Vehicles in Europe.” ACEA, 2025.

https://www.acea.auto/figure/electric-car-sales-share-in-eu/

Statista. “Electric Vehicles in Europe – Statistics & Facts.” Statista, 2025.

https://www.statista.com/topics/4978/electric-vehicles-in-europe/

Mihail Gaydarov

Founder & Chief Financial Analyst.

Nikolay Marinski

Chief Business Analyst, Financial Analyst.