Crypto Markets Between Innovation and Speculation.

Photo by Pierre Borthiry - Peiobty on Unsplash

Article Authors: Mihail Gaydarov, Nikolay Marinski.

Introduction

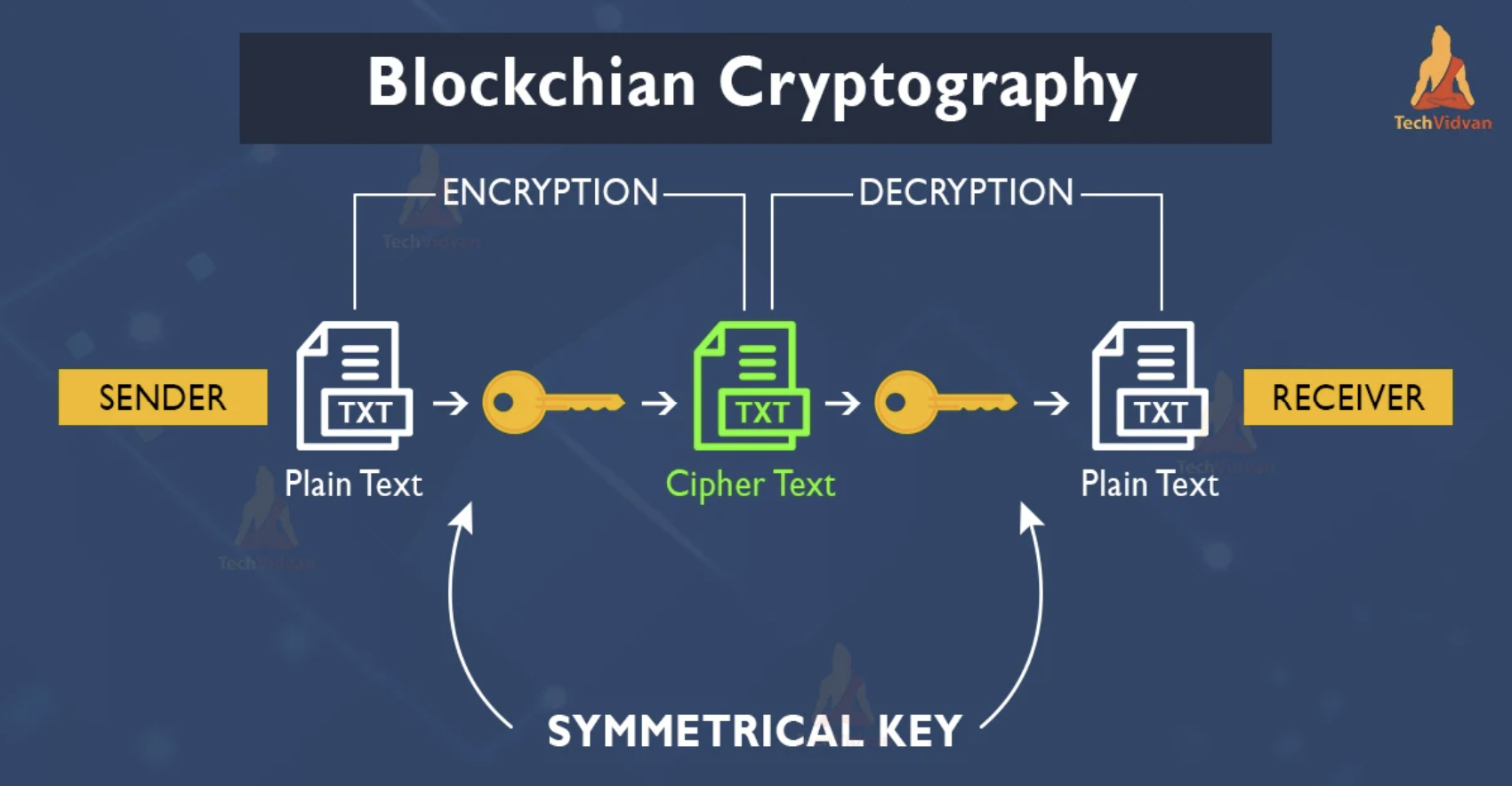

Since the creation of Bitcoin in 2008, cryptocurrencies have become very popular, not only as a technological innovation, but also among investors as both a highly volatile asset and a store of value. Firstly, cryptocurrencies were introduced as a decentralised digital ledger (blockchain), where people could transact money fast and efficiently, without an intermediary. The blockchain isn’t owned by any private or corporate entity, rather it uses a vast network of independent servers, which support the required computing power, more widely known as “miners”. In exchange for this investment in the network, the server owners are compensated with the cryptocurrency, which is comparable to owning shares of a company. The safety comes from the cryptographic lock of each block. A block contains hundreds to thousands of individual transactions, and when it gets “filled” it is locked and connected to the previous one by a cryptographic code, also known as a cryptographic hash, and a separate copy of it is saved on each of the servers. This means that every transaction is verified by the data stored in all of the servers.

Source: TechVidvan

After the 2008 Global Financial Crisis, when people lost trust in the traditional financial system, Bitcoin’s decentralised platform offered a revised way for people to store their funds. Most notably, the cryptocurrency system was met with a lack of demand at the start, due to low levels of credibility and security uncertainty from investors.

In 2013-2014, Bitcoin made its first surge in price, from approximately $13 to over $1000. The reason for this almost a hundredfold increase was a combination of geopolitical and economic factors. In this combination of constituents, we include the Cyprus banking crisis, coupled with high interest in the field from China, and further assisted by mainstream media coverage and heavy speculative buying. This was a pivotal moment for cryptocurrencies, as it exposed them on the map for regular investors as a potential new form of security.

While cryptocurrencies by themselves are a very volatile and insecure asset, holding a significant risk to investors, often priced through hedging and speculation, they are a foundational part of a transactional technological innovation system, which has the potential to change the virtual financial ecosystem in the future.

The Rise of Cryptocurrency: A Product of Bank Crises and Speculation.

Before Bitcoin was introduced to the public, there were several attempts at digitalizing cash, which laid the foundation for the cryptocurrencies we know today, but either remained theoretical or relied on a centralised system. The first project surfaced in the early 1980s and was created by the American scientist David Chaum, who is widely regarded as the first person to give the idea for a digital currency. His project was named “eCash” and introduced the idea of secure private digital payments through the use of cryptographic technology, but was still centralised. In 1998, a computer engineer Wei Dai proposed “b-money”, which was the first idea of a decentralised, anonymous, digital currency system, but at that time it was only theoretical. Finally, the blockchain innovator Nick Szabo, who designed “Bit Gold”, at the time was the closest concept to the present function of crypto, but was never fully implemented.

In 2009, Bitcoin was launched by an anonymous individual or group using the pseudonym Satoshi Nakamoto. It is recognised as the first true cryptocurrency. The first real-world transaction happened on May 22, 2010, when Laszlo Hanyecz paid 10000 Bitcoin for two pizzas. This is an important milestone for cryptocurrencies as it showed the world that Bitcoin had tangible value.

Following that, Bitcoin experienced its first major bull run in 2013, driven by a combination of geopolitical events and other contributing factors. One of the most significant causes was the 2013 Cyprus banking crisis, resulting from the exposure of Cypriot banks to the Greek debt crisis. When people saw their deposits at a potential risk, Bitcoin looked as an attractive asset outside of the traditional banking system. Additionally, driven by media attention and investors searching for alternative investments, there was a surge in the demand for Bitcoin, with the Chinese exchange (BTC China), becoming the world’s largest exchange, accounting for 60% of global volume. Further, the price of Bitcoin was increased by speculative buying and a fear of missing an opportunity, which ultimately led to the creation of a bubble in the market.

The price of Bitcoin dropped in early 2014 and didn’t recover until 2016, because of several matters. The leading factor for the crash was the collapse of the biggest exchange at the time - Mt. Gox, which handled around 70% of global trading volume, according to CoinDesk reporting. Additionally, China’s ban on financial institutions and other third-party payment companies from handling Bitcoin transactions and defining Bitcoin as a “virtual commodity”, instead of a currency, severely decreased liquidity in the market and led to a 50% drop in price in three weeks.

But even after such a crash, Bitcoin didn’t disappear; instead, new and better exchanges emerged, and technical problems were fixed, which showed people that cryptocurrencies weren’t just a short-term hype, but a part of the future.

The Advantages of Cryptocurrency: Decentralization and Money Without Central Banks.

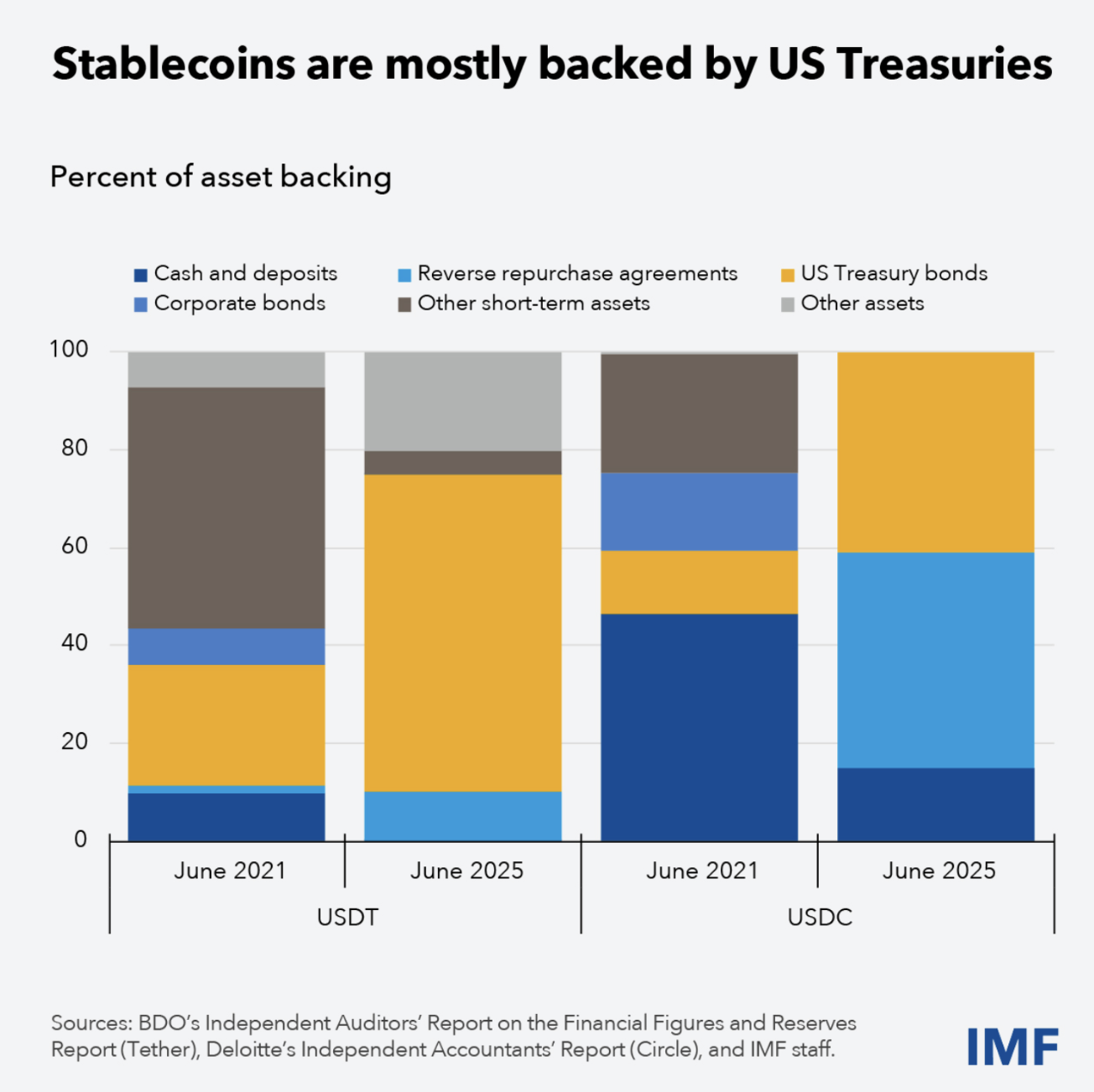

The 2008 Global Financial Crisis shook the financial and monetary systems. People saw that there is a large amount of risk involved when trusting one centralised organisation with their capital. In 2014 a derivative version of cryptocurrency was created in order to facilitate international payments in a more sustainable manner. Stablecoins like the “USDT” and “USDC” are a form of digital currency that has seen large success in the years after its creation. These Stablecoins are essentially digital currency that is backed by mostly liquid assets, like cash, deposits and US Treasury bonds. They are tradable and extremely predictable, which eliminates one of the main downsides of traditional fiat money, such as volatility. Although Bitcoin has a market capitalization of just 10%, the volume of Stablecoins has increased triplefold since 2023, reaching a combined $260 billion for USDT and USDC.

The main advantage of these digital currency coins is that, as well as being predictable, they are extremely efficient at transferring funds across borders without the major disadvantages of traditional financial transfers. When we discuss regular transfers, the logistic compensation for one could reach up to 20% of the transfer value in some cases, rendering this option extremely costly. Furthermore, due to the structure of Stablecoin transfer systems, shortcomings like long process chains, payment systems with operating hours and other delays are avoided. Again, we see this as a great innovation within the financial system, where issues like high transfer costs are mitigated.

Source: International Monetary Fund.

In contrast, a major obstacle with Stable coins is that they are centralised. The fact that they are owned by private institutions implies that they are managed and controlled by these entities. Similarly, as well as a hinder to transfer privacy, it ensures that transfers of funds around the world are not illegal and do not coincide with any kind of fraud, therefore it could also be seen as a positive aspect to centralisation.

Another positive aspect concerning cryptocurrency is the innovative and technological drive that they provide to the transfer market. The extremely low costs for making a money transfer and the exponential interest in such assets foster competition in the field. This could lead to lower costs with traditional transfer methods, as price pressure comes from these Stablecoins.

Furthermore, the introduction of such innovative methods for payment results in the spread of risk to other entities, unlike the traditional models where the risk within the system is held solely by financial intermediaries like banks, and mutual funds. Such occurrence ensures that single-point failures are far less likely to occur. “Black Swan” events like the 2008 Global Financial Crisis could become more predictable and even preventable. Overall, cryptocurrency innovation is a great method to diversify sectors like currency transfers and with the correct, extensive regulatory oversight, giving ground to future possibilities for more competitive markets that aim not only at individual profits, but also at providing the consumer with the best possible service.

The Shadow Network of Transactions derived from Cryptocurrency.

Considering all the benefits of investing in cryptocurrency it is important to note that there are significant downsides to the blockchain as a whole and the cryptocurrencies as a building block. In many instances around the world, especially in the development era of the crypto market there have been recorded cases of fraud and malicious activity circulating cryptocurrency. The decentralised nature of the cryptocurrency network of transactions is fundamentally enabling these negative outliers to exist. But more importantly, the main issue regarding cryptocurrency is the poor oversight of governmental regulators which further enables and fosters these criminal activities.

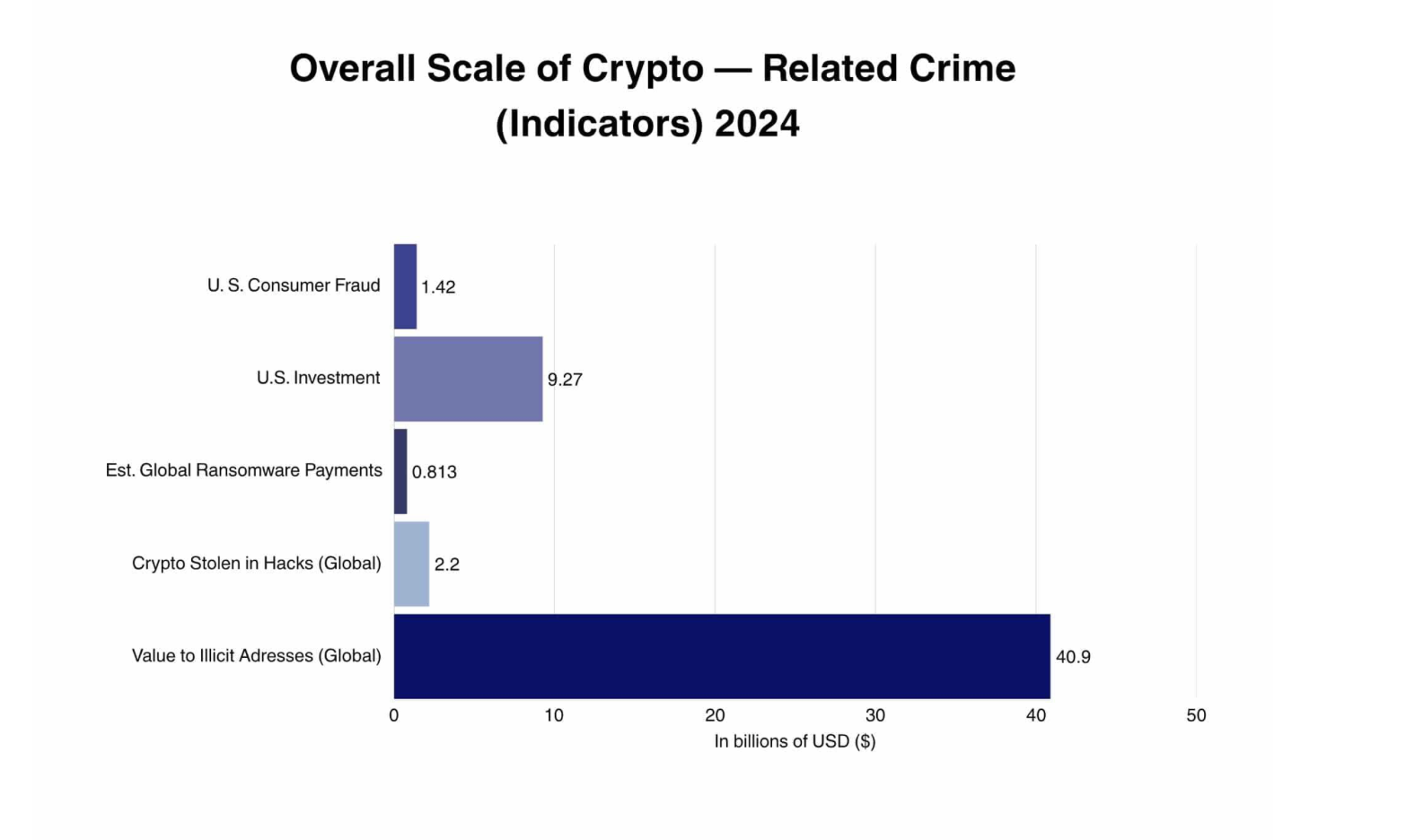

To give material scale to the relative amount of crypto scams we have identified a few officially posted indicators that provide insight on the volume of crypto-related crime.

Source: The Financier Review

Exit Scams

Furthermore, it is important to discuss the ways through which cryptocurrency is used in malicious activity. If we have to rank these scams among the most popular, the exit scams and Ponzi Schemes will take the first place in terms of frequency. In 2017, the esteemed crypto analysis firm Satis Group reported that 80% of all Initial Coin Offerings (ICO) were in some way or form - scams. The principal method from profiting on other investors' behalf was utilizing these ICOs. Coins are offered to the public, investors purchase these coins with the hopes of profiting from a hike of the price. What happens in the practice is that the creators of these coins speculate on the value of the coin and benefactors of the initial creators profit from the sudden surge in price. From there mostly the price crumbles, while initial creators abandon the project entirely.

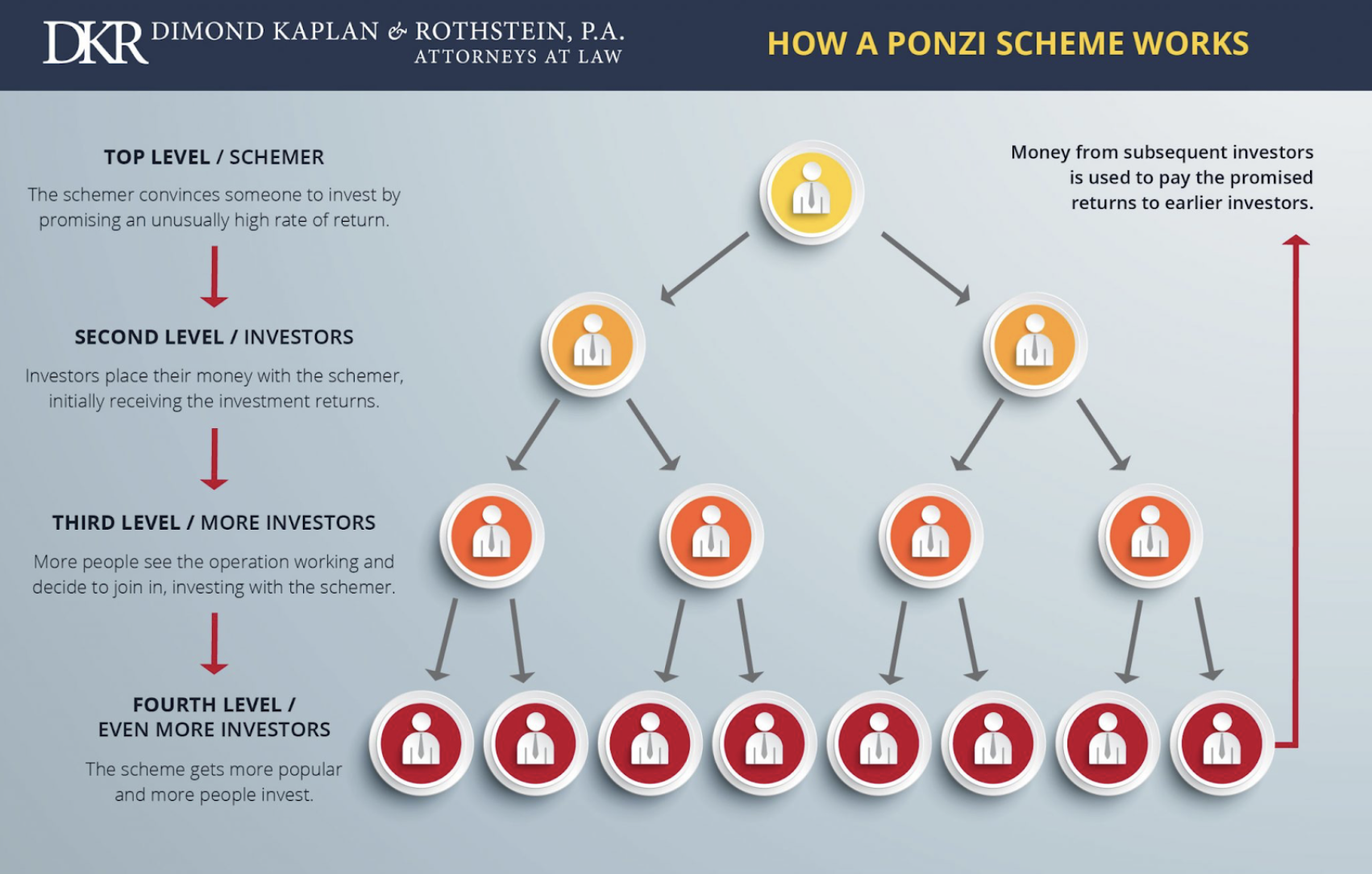

Ponzi Schemes

Another very popular example of cryptocurrency scams are Ponzi Schemes. In essence, they are just multi-level marketing schemes that encourage inexperienced investors (mostly through blockchain) to conduct risky investments. The model of the scheme usually consists of branching through a network of “ambassadors” that convince lower level members to invest in the given coin, while being compensated by unusually high returns. In other words, the model works by materially incentivising members to invite others to participate in the scheme. For instance, the most popular method to do so is through a monetary incentive - you join the network by investing a couple hundred dollars of your own money and for every next member you invite, you receive an abnormally high commission. Although the high commissions are rather lucrative, this model is fundamentally unsustainable and impossible to conduct business through due to significant cash flow problems and the need for reinvestment.

Of course, it is difficult to pinpoint the exact amount of people that have been affected by ponzi schemes, and even more so for crypto currencies specifically. Reports suggest that 57% of adults worldwide were a victim of some sort of financial scam. It is also important to note that the quoted figure above includes all financial scams, but there is statistical evidence suggesting that the majority of commercial scams are some forms of ponzi schemes. The Global Anti Scam Alliance (GASA), quotes that about half of the total adults actually lost money subject to a fraudulent financial scheme. This results in about 1 in every 4 adults being scammed of their money.

If we have to bring theory into reality, arguably the most significant Ponzi Scheme involving cryptocurrency was the Onecoin scandal. Onecoin was a large enterprise that was founded in 2014 by a woman named Ruja Ignatova. Their product revolved around producing a cryptocurrency that was a revolution in the field and a significant step towards a more unified blockchain for investors. In practice, the price of the coins was internally and manually regulated by Onecoin themselves. Under the surface it was a classical Ponzi Scheme with a pyramid structure that managed to last a little longer than usual.

The mechanism behind the Ponzi Scheme was the following: An investor would buy these offered “educational packages” bundled with tokens. As per usual, the compensation of each participant was dependent on the recruitment of new partners, rather than providing real value to the underlying service. The scale and success of this scheme was so large that it is often considered one of the largest, if not the largest, ponzi schemes globally. Onecoin is estimated to have raised from $4-$15 billion during their operational period. At the end of 2017, the founder Ruja Igantova disappeared from the public and the scheme ultimately collapsed after scamming investors of nearly $3 billion.

To this day, Ignatova remains the most wanted financial fugitive. Some reports suggest that the “cryptoqueen” was murdered on a yacht in 2018, but the more believable version of the story is that to this day she is alive and hiding from law enforcement for a little under a decade after her escape to Athens in 2017. More importantly, the story of the “cryptoqueen” and Onecoin is an example of how a great idea can turn into a malicious and deceptive practice. The narratives of cryptocurrency and the lack of transparency and moderation on the market are apparent through such stories. So investors that want to expose themselves to cryptocurrency should be wary of newer “revolutions” in the field.

Source: Dimond Kaplan and Rothstein.

Money Laundering

Another very popular, malicious utilization of the blockchain and cryptocurrency overall is money laundering. As we discussed previously, the nature of the crypto network allows transactions to be anonymous and very difficultly traceable. Government regulators and other oversight agencies are unable to control transactions, which criminals often use to transfer cash to their needs. Cryptocurrency as such is not fully anonymous but the pseudonymity of it is a significant driver of these activities. They might not be autonomous, but they are increasingly difficult to get de-pseudomised, making them an attractive method for transferring criminally sourced funds. Initial Coin Offerings are used as a popular method for laundering cash into a given scheme, while the weak Know Your Customer (KYC) framework and Anti-Money Laundering mechanisms allow this to happen.

The way money laundering occurs is through a regular offering of coins, where criminals inject illicit funds into the scheme. The so-called “Placement” is to move the “dirty” fiat money into the crypto system. Since entry to ICOs is often permissionless, these criminals use straw accounts (fake identities) or multiple wallets to fragment flaws and insert their cash. Later by purchasing tokens, the same tokens are sold to legitimate investors, after all rendering the “dirty” money, “clean”.

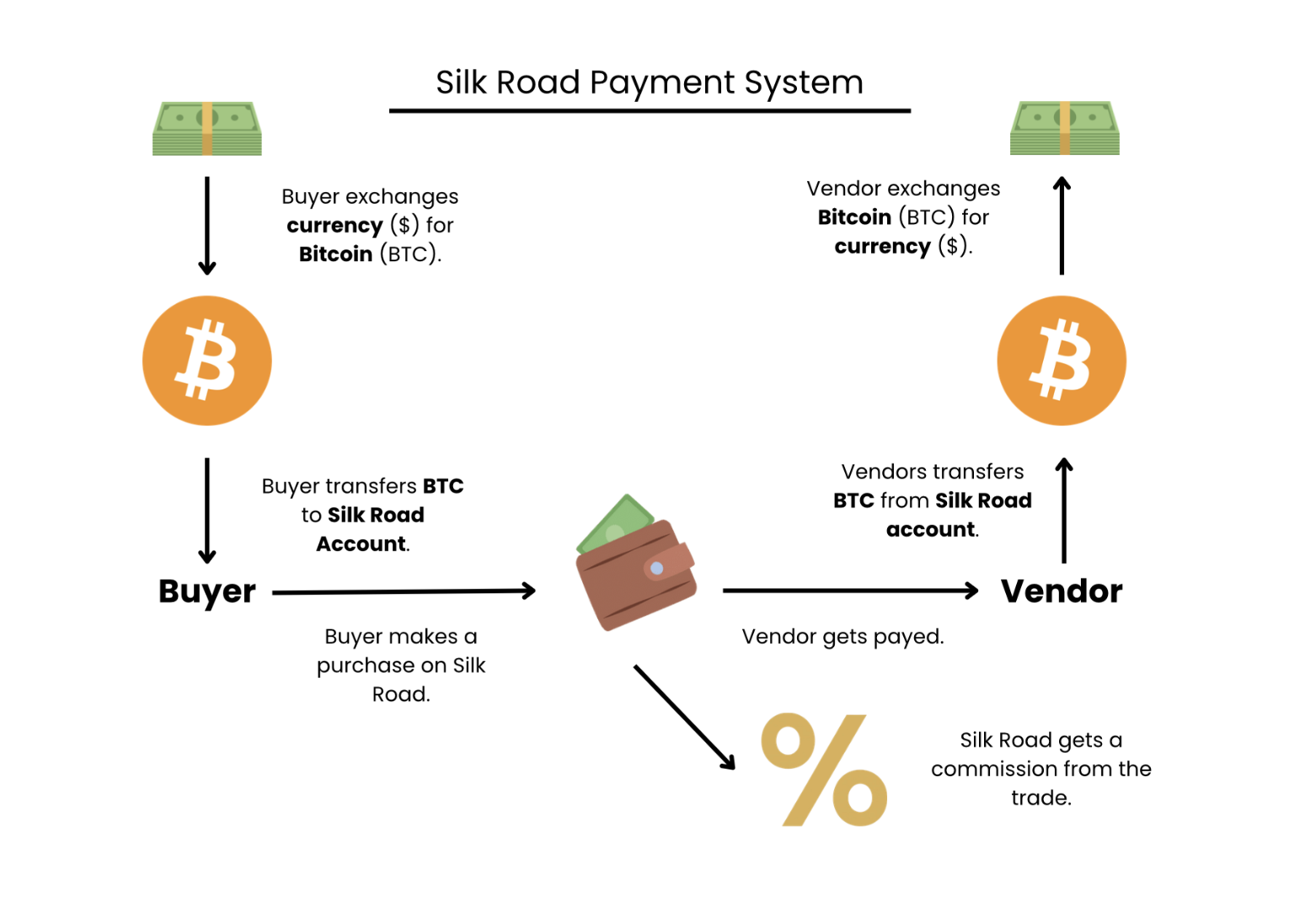

As well as money laundering there are other exchange level vulnerabilities that are embedded in the foundation of the crypto network. Centralised exchanges and transfers, especially in the early days were lacking in AML (Anti Money Laundering) security frameworks which led to the creation of businesses like “Silk Road”. In 2011 a physicist and engineer by the name of Ross Ulbricht created a complex payment system that facilitated the needs of a world-wide dark web market. The market functioned as an exchange place for drugs, forged documents and other illicit services. The system worked by offering payment only though bitcoin, which made the mechanism unreliant on bank oversight, ensuring secrecy.

Source: The Financier Review.

Silk Road used a built-in escrow system meaning that it temporarily held funds in order to facilitate the given payment. Using a combination of mixing/tumbling techniques, the transactions were kept by redistributing funds across wallets. At the base, the transaction system operated on the following principle: a buyer would purchase their need on the market using bitcoin. The moment this happens the cryptocurrency funds entered Silk Road wallets and the transactions were routed through multiple addresses. The vendors received Bitcoin and later converted them into fiat money reused in the crypto system. Fundamentally, Bitcoin acted as a sort of layering tool that did not provide enough anonymity to be untraceable, but offered enough obfuscation.

The model operated from 2011 to 2013, when the FBI arrested Ross Ulbricht and shut down the entire system. Silk Road had an estimated volume of transactions at about $1.2 billion, from which every time it took a small cut for said transaction. Ultimately, The Silk Road marketplace demonstrated how Bitcoin could be used to facilitate and obscure illicit transactions at scale, combining escrow systems with transaction obfuscation techniques to enable large-volume money laundering despite the traceability of blockchain records.

Cryptocurrency Derivatives: The Blockchain.

Тhe first blockchain was the Bitcoin blockchain. It was designed as a decentralised digital ledger, which allows its users to transact money safely, without an intermediary, by using proof of work (PoW). PoW requires participants (miners) to use computational power to solve complex mathematical puzzles - finding a specific hash code. This process validates transactions and prevents fraud or double-spending without needing a central authority. The miner, who first solves the puzzle, adds a new block to the chain and receives compensation in the form of a cryptocurrency. This system is considered extremely safe, because for a person to tamper with it, they would have to not only change each copy in every individual server supporting the blockchain, but also because each block is connected with a unique hash code, he would need to change every one of the following blocks as well. The drawback is that to support this system, a large amount of computational effort is required, which leads to high energy consumption.

The next big leap forward in blockchain technology was the introduction of Ethereum. Firstly introduced in 2013 and later launched in 2015 by the Russian programmer Vitalik Buterin, Ethereum brought new functionalities to the blockchain technology. While Bitcoin was regarded as a store of value and a digital currency, Ethereum offers an open-source blockchain platform providing smart contracts, which are self-executing programs that automatically run actions (e.g., transferring funds, updating records) when predetermined conditions are met. Furthermore, this programmable blockchain could be used for decentralised applications (dApps) and decentralised autonomous organisations (DAOs). This made Ethereum the foundational layer for Decentralised Finance (DeFi), Non-Fungible Tokens (NFTs) and Web 3 development. Moreover, in 2022, in an update called “The Merge”, Ethereum switched to using proof of stake, instead of proof of work. This means that instead of miners using big server centres, validators lock up a portion of their cryptocurrency as a stake (bond) to earn the right to validate transactions and create new blocks. This, in turn, is not only more energy efficient and environmentally friendly but also enables faster transactions - 15-30 transactions per second (TPS), compared with Bitcoin’s 4-7 TPS.

Regarding speed, the Solana blockchain was purposefully created with the aim of solving one of the biggest problems with cryptocurrencies - how to make blockchains operate faster and cheaper. Its mainnet launch was in 2020. While it shares a similar open-source blockchain to Ethereum, which allows Web 3 development, it differs in its use of Proof of History (PoH) in combination with Proof of Stake. PoH is a technical innovation original to the Solana blockchain. It solves the problem of ordering transactions and timing the events by creating a verifiable timeline, which helps the network know what happened and in what order, in a faster and more efficient way. This allows Solana to send 3000-5000 TPS with extremely cheap fees of around $0.0005. This makes Solana exceptionally attractive and preferred over similar blockchains like Ethereum for DeFi, transactions, and NFTs.

These technological advancements have made a huge impact on the way people operate in digital spaces. In particular, dApps are open-source software programs that run on peer-to-peer blockchain networks, such as Ethereum or Solana. By using smart contracts, they operate independently without intermediaries, offering higher transparency, censorship resistance, and user ownership of data. Owing to their use of cryptographic verification, they are highly secure, private, and resistant to shutdowns. Furthermore, DeFI, through the use of smart contracts, enables users to lend, borrow, and trade directly from a decentralised wallet, without a central exchange or bank. This offers transparency, because every transaction is recorded on a public, immutable ledger and speed, as cross-border transactions happen faster than with traditional banking. In addition, blockchain technology has enabled the proof of authenticity and ownership of digital and real-world assets. The NFT is a unique non-fungible digital certificate stating that the person owning it possesses the said digital asset, but not necessarily the copyright or full commercial rights, unless the terms explicitly say so. Initially, the owner “mints” the NFT on the blockchain, which gives it a unique token ID and the ownership is linked to a specific wallet address. Following this, when the owner sells it, the transaction is recorded on the blockchain. Naturally, it is worth mentioning that, as a new invention, there are still problems and bugs which may occur. Nevertheless, developers are actively working on fixing and improving these systems, showing that they are here to stay.

The Future of Cryptocurrency and Investor Implications

While crypto prices are highly volatile, as a result of being supported by mostly speculative buying and fear of missing an opportunity, blockchain technology has proven incredibly useful. It has brought many innovations, which are being incorporated across various new sectors. Especially, NFTs have transformed the use of real-world assets by providing a secure way to verify ownership for physical items through the blockchain. This helps reduce transaction friction in industries like real estate, luxury goods, and ticketing and helps guarantee authenticity and reduce fraud.

Taking this into account, we can conclude that cryptocurrencies aren’t just a short-term hype. Their blockchain applications are quickly becoming the building blocks of the new Web3 and bring new way users can interact with the digital space.

Nevertheless, this does not rule out cryptocurrencies as potential investments. Scarce currencies, like Bitcoin, which is capped at 21 million coins, have the potential to truly live up to its nickname and become the digital alternative to gold. This scarcity could make this type of cryptocurrency a good investment opportunity and a secure store of capital. Additionally, other investment derivatives of crypto currency and alike assets have the potential to add great value to the blockchain network. Stablecoins and other similar products create competitive market environments, which ensure that in the long run consumers receive a better product, at a better price.

While other currencies like Ethereum and Solana use inflationary models and have unlimited supply, different deflationary mechanisms are set in place to manage inflation by destroying (burning) a set percentage of each transaction fee. For Ethereum, the base fee from each transaction is burned. During periods of high network activity, this burning can exceed new coin issuance, resulting in a deflationary effect. In the case of Solana, 50% of transaction fees are burned, and while initially the inflation rate started at 8%, it is decreasing by around 15% year-over-year, with a set goal of settling at a stable rate of 1.5% in 2031. These mechanics make such cryptocurrencies a promising investment as a hedge for centralised currency inflation rates, such as the Dollar (2.5%) or the Euro (2.3%).

Bibliography

Frankenfield, J. (2019). Mt. Gox. Investopedia. https://www.investopedia.com/terms/m/mt-gox.asp

Lee, B. (2026). BTC: Bitcoin, a New Value Chain in China – US-Asia Technology Management Center. Stanford.edu; Stanford University. https://asia.stanford.edu/course/topics-in-international-technology-management/2013-topics-in-international-technology-management/btc-bitcoin-a-new-value-chain-in-china

Picardo, E. (2023). Solana (SOL). Investopedia. https://www.investopedia.com/solana-5210472

Piyankov, H. (2025). Solana (SOL) Tokenomics: Sustainable Growth and Design. FinDaS Main Website. https://www.findas.org/tokenomics-review/coins/the-tokenomics-of-solana-sol/r/7KPXo3rqeQKcMgVC72GUGu

Token Terminal. (2020a). Bitcoin Transactions per second Metrics. Tokenterminal.com. https://tokenterminal.com/explorer/projects/bitcoin/metrics/transactions-per-second

Token Terminal. (2020b). Ethereum Transactions per second Metrics. Tokenterminal.com. https://tokenterminal.com/explorer/projects/ethereum/metrics/transactions-per-second

All data used in this article is derived from publicly available institutional reports and industry analyses.

This article is for informational purposes only and does not constitute investment advice.

Mihail Gaydarov

Founder & Chief Financial Analyst.

Nikolay Marinski

Chief Business and Financial Analyst.

Maxim Gaydarov

Chief Woof Woof Officer

Happy 1st of April!

The Financier Review

© 2026 The Financier Review. All rights reserved.