Private Credit And The Shift Beyond Banks - Structural Transformation Or Cyclical Illusion?

Photo by Ales Nesetril on Unsplash

Article Author: Mihail Gaydarov.

Editor: Nikola Todorov.

IntroductioN

The global credit landscape has undergone some crucial structural changes since the 2008 Global Financial Crisis that crippled many large institutions. The collapse of the securitised credit market, primarily driven by excessive leverage on loans, poorly structured credit risk assessment and other asymmetric issues triggered a large-scale regulatory overhaul that changed private lending and fundamentally altered the origination of credit, the distribution of lending and how banks hold their loans on their balance sheets. If we take into consideration the history of private lending, banks are the most prominent figure here. In the aftermath of the crisis and the tightening regulations banking institutions were subjected to much tighter capital and liquidity requirements under frameworks like Basel III.

Although these very important structural changes provided the guidance for a more secure environment for private lending, it came at the cost of major constraints for banks. These financial intermediaries were forced to reduce their exposure to risk-weighted assets and narrow their levered lending. While the private lending activities of banks were shrinking, a niche developed for non-bank companies that turned from a rare asset class into what we now know as a pillar of global capital markets.

The scale of the expansion that these intermediaries saw was very sizable. In 2010 the global private credit assets were valued at $300 billion (USD), which is a negligible figure compared to the estimated $3.5 trillions (USD) in 2024. As of 2026 the industry for private lending is considered to be one of the fastest-growing segments in what we see as modern finance. It is notable that the trend of growth is not merely cyclical but a reflection of deeper structural changes brought by regulatory frameworks similar to Basel III.

We can argue that while private credit is capturing a very large portion of the market share from traditional banks, the implications from this trend extend far beyond institutional displacement. Private credit institutions are primarily reshaping the architecture of financial intermediation more than replacing banks in their entirety. These firms introduce new methods for efficiency, they redistribute risk across the entirety of the system while questions regarding liquidity, transparency and long-term sustainability remain.

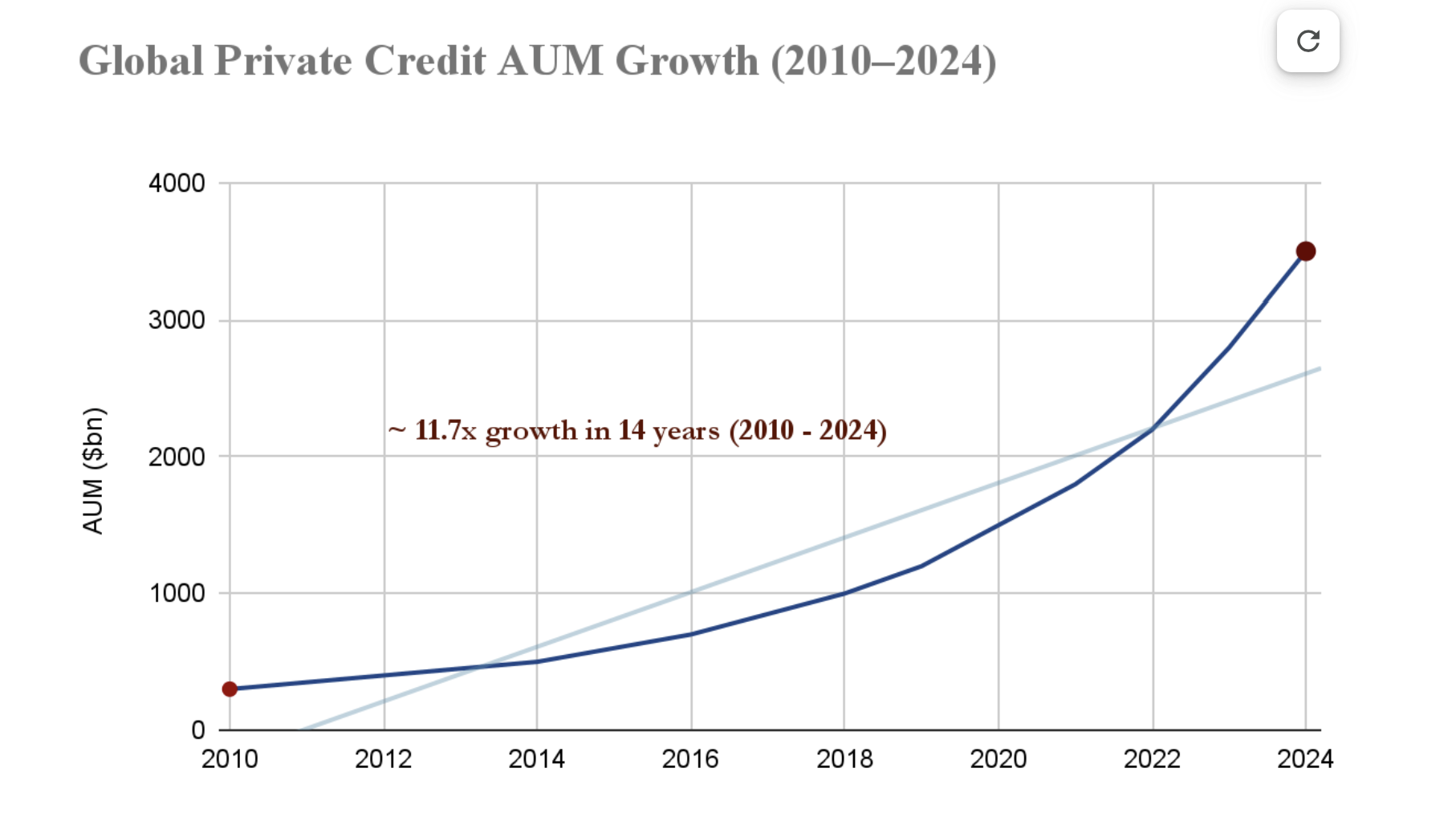

Figure 1.

Graph interpretation: as illustrated in figure 1, private credit has seen a large expansion from $300 billion in 2010 to $3.5 trillion in 2024. As observed using our data, that is more than a tenfold increase in 14 years. Post-2018, we note a significant non-linear growth that reflects both institutional capital inflows and structural displacement of bank lending.

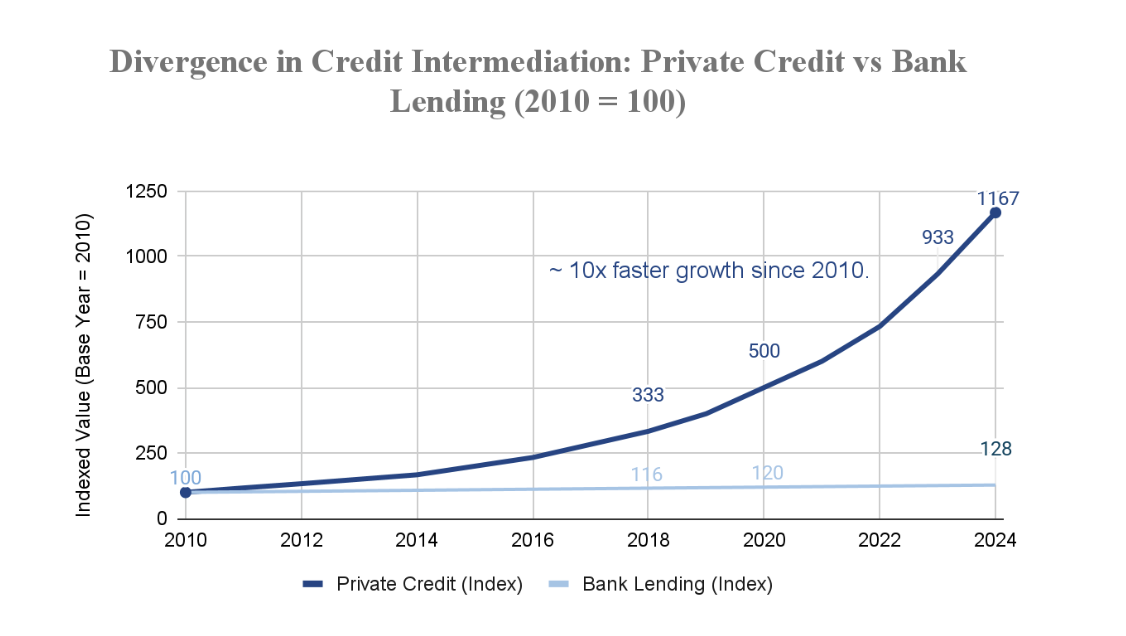

Figure. 2

In this case Figure 2 illustrates a clear and very persistent evolution of credit intermediation following the 2008 Financial Crisis, with a higher focus on the divergence to private credit. While global bank lending has expanded relatively, rising to an approximate index of 128 in 2024, private credit has experienced a growth that can only be described as exponential. Private credit reached an index of 1167 over the same 14 year period. If we compare the two industries we have private credit with a growth of nearly elevenfold, which corresponded to a compound annual growth rate of 20% (CAGR)

We can argue that this isn’t just a function of the cyclical expansion, but more or less a structural reallocation of credit provision away from traditional bank balance sheets following the crisis in 2008. The relatively flat and insignificant growth of bank lending is in very sharp contrast to the exponential growth of private credit, which is not simply growing alongside banks, but increasingly capturing incremental demand in credit markets.

Therefore, the rapid expansion of private credit post-2008 is not a cyclical anomaly that is a short trend fuelled by opportunity, but more or less a direct consequence of the reconfiguration of credit markets caused by regulatory constraints on banks. These new frameworks shifted risk-taking and lending activities towards non-bank financial entities, which fundamentally altered the architecture of financial intermediation.

The Pre-Crisis Credit Model: Expansion and the OTD Business Architecture.

In the years prior to the 2008 Global Financial Crisis global credit underwent a very significant structural shift that was derived from financial innovation, stable liquidity and a sustained demand for yield. In the traditional sense of banking business, these institutions engaged in a system known as OTH (Originate-to-hold). Put simply, the OTH model was such that banks sourced the loans and kept them on their asset side of their balance sheet until the end of the loan maturity (until the debtor repays their financial obligations + interest). Although this model was stable and predictable it was very limited when we refer to liquidity since banks were only allowed to give so many loans due to capital legal restrictions on their balance sheets .

As a result, banks had to improvise in order to provide more liquidity to the rising demand for funding. Subsequently, they slowly started to replace their business model to an originate-to-distribute, which fundamentally altered incentives, interested parties and the overall risk dynamics of credit intermediation.

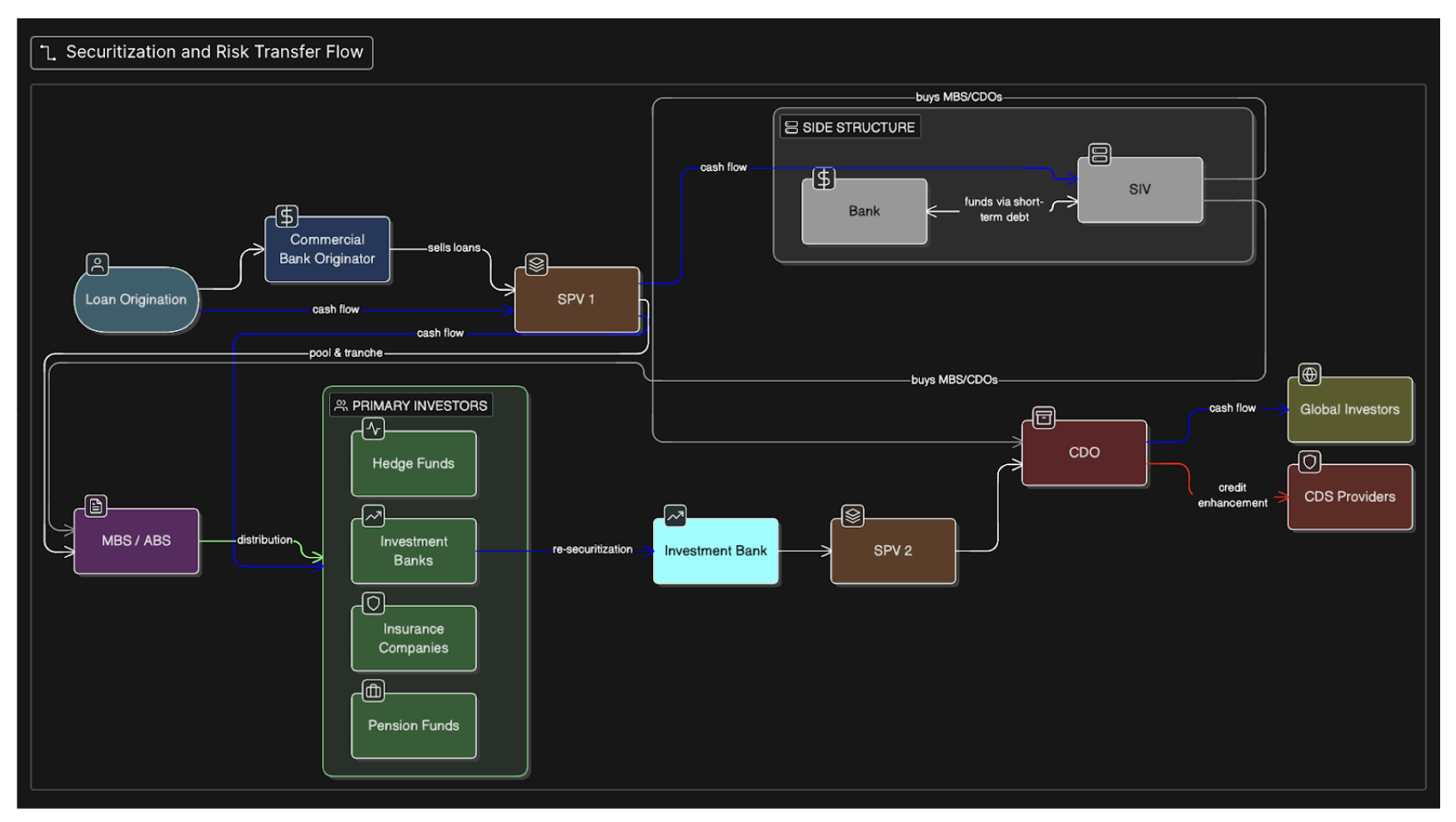

Under the OTD model, banking institutions originated loans that were mostly in the field of residential mortgages and transferred them quickly to entities that were outside of their own balance sheets through a process known as securitisation. The loans were pooled into other kinds of derivatives known as Mortgage-Backed Securities (MBS) and later restructured as Collateralised Debt Obligations (CDOs), which were sold to institutional investors on a global scale. Through this process banks were able to bypass regulatory frameworks on the amount of loans able to issue, recycle capital efficiently and significantly expand credit supply beyond the constraints of their balance sheets.

The Process of Securitisation (Full Scale).

The relative scale of this distribution expansion was rather substantial. In the U.S.A alone, the total mortgage debt increased from approximately $4.8 trillion in the very early 2000s to $10.5 trillion by 2007. While this notable growth of 2.2x is intriguing by itself for the entirety of the credit market, the real issue lies in issuance of subprime mortgage loans. Subprime mortgage loans were a practice done back in the 2000s where loan issuers gave out loans to individuals with almost no background check to ensure they are solvent and/or able to pay their future debt obligations. Subsequently, a staggering 80% of this class of loans were never repaid and the debtor was declared insolvent. This class of loans alone rose from $130 billion per annum to more than $600 billion per annum over the same period. This is a recorded growth of 4.6x from 2000 to 2007. This record high growth reflected not only the demand for housing finance but also a systematic relaxation of the standards for originating loans when we talk about commercial banks.

But despite the risk of subprime mortgage debtors not paying back their obligations was evident, there were other severe misalignments with the general framework of the OTD model. For starters, loan originators were compensated based on the volume of their trades and not on the performance of their loans. This raises a serious issue where banks are not highly incentivised to ensure creditworthiness, but rather keep a high volume. At the same time as this decline in pre-loan creditworthiness, investors relied heavily on external credit ratings that were issued by CRA (Credit Rating Agencies). Essentially, investors trusted loan ratings from these agencies that had a major flaw in their transactional model of business.

From a technical standpoint these agencies were used to operating and assessing risk mainly through the usage of historical data from 20-30 years ago. The problem with this practice is that even though these ratings were considered accurate, they weren’t quite so. Banks utilised the traditional Originate-to-Hold model that was so popular during the decades prior to the crisis and these agencies used data from this banking model to analyse credit, while banks had slowly moved to the OTD model, rendering the data rather inaccurate to assess this newer banking technique.

Furthermore, another very notable flaw to this risk assessment model is the presence of a conflict of interest. While Risk Agencies by themselves were accurate with their ratings, essentially, the seller of the derivative/security is the one to pay the risk agency to assess their own instrument. Of course, the argument to be made here is not that the ratings were fabricated, but more or less that the business model was flawed. At the time very few investment clients for these agencies existed therefore, losing a client meant being run out of business. On that premise, institutions worked closely with CRAs in order to bring their ratings up, formally. Investment Banks sometimes decided to keep bad loans on their balance sheets and pool ones with higher credit ratings, implying that the lesser the risk, the lower the required interest on that loan pool. Ultimately, the lower rating meant that investment had to pay less interest on those loans, retaining higher profits.

And with this in mind, we can argue that this structure created the illusion that risk is diversified and spread out across the financial system. In practice, the story was completely different. Risk was transformed and redistributed in opaque ways, through multiple layers of securitisation. The complexity and opaqueness of this system obscured underlying exposures and limited the transparency of the market.

At the same time, the macroeconomic conditions in the majority of the world reinforced these dynamics. During the early 2000s interest rates were particularly low following the 2001 recession. This encouraged both borrowing and risk-trading while global capital inflows, especially from surplus economies, provided ample liquidity to sustain credit expansion. Due to the pressure on financial institutions for expansion and especially the idea for an owned house for every American, further accelerated the growth of securitised lending.

At the essence of all, the financial system back then did not lack innovations per se, but more or less failed from a structural standpoint. It succeeded massively, at redistributing and providing liquidity to the system. The issues arise from failure of risk governance and incentive alignment. This imbalance between the deterioration of underlying liquidity and the expansion of the credit environment laid the structural foundation that crumbled the market in 2007 and 2008. Once assets began to deteriorate in performance, like in our case real estate, the weakness exposed inside the system, triggered a global financial crisis across markets.

The Structural Consequence: The Emergence of a Credit Vacuum.

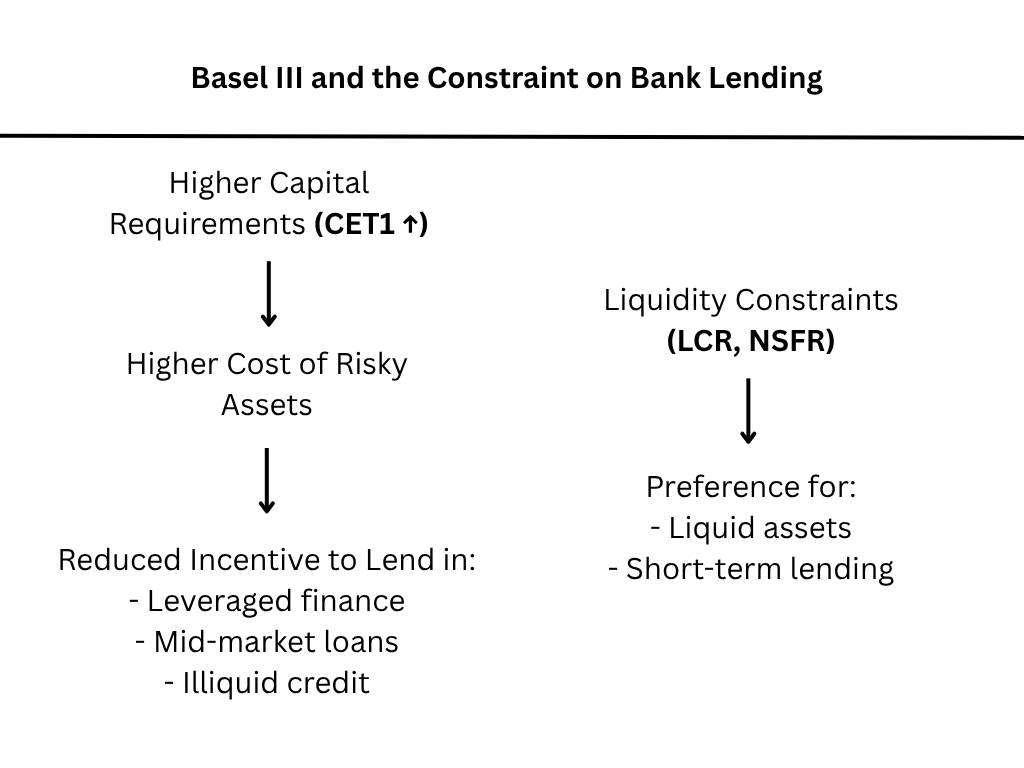

Following the crisis, policymakers implemented a comprehensive overhaul of the system, while trying to restore stability and prevent recurrence of the vulnerabilities exposed during the crisis. Arguably, the most crucial variable to this effort was the introduction of the Basel III framework. It increased mandatory capital and liquidity substantially, while also raising risk management requirements for banks. Fundamentally, the framework did not eliminate risk, but altered the lending activities that were historically reserved for commercial banks, and increased their material expense from a capital and funding perspective.

The shift was mostly prominent in segments like leveraged finance and mid-market corporate lending. These areas are typically characterised by higher risk and lower standardization. Under the new regulatory regime, these exposures carried disproportionately high capital charges, reducing their attractiveness relative to more liquid and lower-risk assets.

Evidence suggests that there has been a sharp decline in the share banks held for these given lending categories. As of the mid-1990s, 70% of the middle-market lending was held by banking institutions. Nowadays, we are looking at a share of a mere 10%. This illustrates most importantly the significant withdrawal from segments where flexibility and risk tolerance are mandated.

It is important to note, that the lack of supply on the bank side did not relate to a reduction in demand for private credit. Private equity expanded massively especially in recent years and increased corporate leverage required for tailored financial solutions. At this point we get a clear view of the occurring structural imbalance. Large demand for private capital that meets with a constrained traditional credit system. The gap in the demand for this service and the lack of supply for it represents a defining image of the post-crisis lending landscape. From this “vacuum” private credit emerged to what we now know as the dominant force in this field. Of course, private lending did not become a perfect substitute for bank lending, but a complementary mechanism that is aimed to operate where banks are constrained by their balance sheets.

The Rise of Private Credit: Force of Efficiency, Yield and Structural Demand.

The emergence of modern private credit as a dominant force in financing is not only a consequence of retrenchment on banks but also as a result of the benefits it provides to its customers. Private credit is effective at aligning the incentive of investors and borrowers by operating outside of the traditional bank balance sheet constraints.

Borrower Advantage (Flexibility and Speed)

From the perspective of a debtor, the services that private credit provides are relatively superior to those from banking institutions. For instance, one of the main benefits is the speed of execution for each transaction. Syndicated loans usually have delays due to the process of internal risk assessment which is very typical for banks and bank-like institutions.

And perhaps the more significant point to be made here, is the fact that private credit allows for bespoke financial structures that banks simply cannot offer. The loans that Private Credit offers can be customised to the needs of the clients. These include customised covenants, flexible repayment schedule and other capital solutions. The value of this flexibility is mostly perceived well by mid-sized companies and private equity-backed firms. For these enterprises, and the complexity of their business and demand for hybrid loan structures, accompanied by time-sensitivity, makes private credit firms so attractive for them.

In volatile market environments, this flexibility becomes even more critical. Unlike banks, which may reduce lending activity during periods of uncertainty due to regulatory or balance sheet constraints, private credit funds are often able to deploy capital opportunistically, providing a more stable source of financing under stressed conditions.

Investor Demand (Yields, Illiquidity Premium, and Portfolio Diversification)

From an investor stand point, private credit has benefited largely from a sustained demand for yield in an environment with low interest rates. The historically low returns of traditional fixed-income instruments, as a result of the 2008 Financial Crisis meant that investors were seeking alternative sources of income.

Investment alternatives from private credit often generate yields in the range of 9-12% far exceeding any yields in the public debt market. This higher return is a product of the illiquidity of an asset class and also of the complexity of underlying loans.

Furthermore, private credit has another major advantage to traditional banks. The service offers much better diversification offers with institutional portfolios. The performance of these companies is loosely correlated with public equity and the bond market, which makes private credit an attractive allocation for insurance companies, pension funds and other practices that augment risk-adjusted returns.

Structural Growth and Market Scale

The effects coming from the demand of borrowers and investor allocation had constituted a large-scale expansion in private credit markets. The global assessment for these instruments has reached $3.5 trillion as of 2024. A tenfold increase since 2010.

Recent data suggests that this growth trajectory is still unfolding at a substantial rate. Private credit deployment reached $592 billion in 2024 alone, indicating a large growth year-on-year. Fundraising activities also remain robust with approximately $224 billion of capital raised in 2025. These figures highlight not only the scale of the market, but also the substantial growth it is experiencing year-on-year, indicative of the demand for more customised credit services.

More importantly, the growth has been facilitated within particular sectors such as direct lending to mid-market companies and sponsor-backed transactions. These are the exact sectors that banks have retreated from due to regulatory restrictions, implying that private credit expansion is structurally linked to the post-crisis banking model.

Are we going to see a full replacement of banks in the lending segment of finance?

This rapid expansion of private credit has arguably fostered the perception that traditional commercial banks will cede their dominance as the primary providers of credit within the financial system. While the divergence of growth trajectories as illustrated in figure 2. supports this view of bank lending going extinct is more or less an oversimplification of the structural dynamics in this transformation.

After all, banks remain the central pillar of financial intermediation and it is highly likely that will continue to be the case. The role of an intermediary such as a bank is not only as a lending vehicle, but also sustaining critical functions like deposit-holding and payment infrastructures which play a crucial role for providing system-wide liquidity. These functions are deeply embedded within the monetary system and are supported by regulatory frameworks and central bank backstops that private credit institutions do not possess. As of recent estimates, the global banking sector continues to hold an asset valuation in the range of $165 - $180 trillion.

What has changed is not the relevance of banks as a whole, but in what activities banks precisely engage. In the post-crisis regulatory environment, banks have increasingly concentrated on assets that are capital-efficient, liquid, and compliant with stricter risk-weighting requirements. This allowed banks to strategically retreat from leveraged lending, and mid-market corporate finance. Areas that have become less attractive due to regulations such as Basel III.

Therefore, private credit expanded exactly within these segments. Effectively, these segments were private debt platforms, direct lending, and other alternative asset managers. This change reflects the functional segmentation of the credit market, reinforcing the idea that this post-2008 change is a structural shift of the financial system. Private credit has scaled in fields where precision, execution speed, flexibility and tolerance for illiquidity are vitally important. In contrast, banks have concentrated their activities on standardized, liquid and exposures that are capital efficient.

This shift has resulted in a system that is known as a layered credit system. Banks and private credit operate on a parallel basis, where each addresses different segments and demand for credit needs rather than competing with each other.

At the same time, it is important to make another point to the case of private credit and banking, that is how blurred the boundary is. Financial arrangement and capital allocation now directly and indirectly expose banks to private credit. This growing interdependence suggests that private credit is not developing in isolation, but as an extension of the broader financial system.

The implication is clear: private credit is not replacing banks—it is redefining the perimeter of the banking system itself.

Risk fragilities: the redistribution of risk

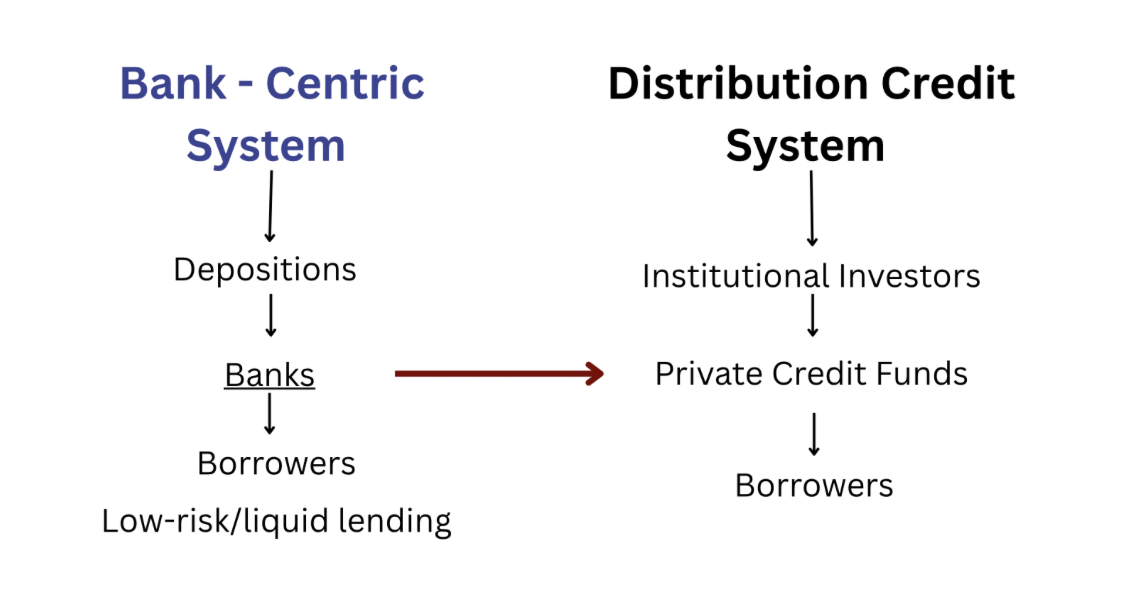

Bank - Centric System vs Distribution Credit System.

The structural expansion of private credit has introduced a new form of risks to the credit market that differ from the traditional preconceived notions of a bank-based lending system. These risks are not derived from excessive off-balance sheet lending and regulatory arbitrage , but from the design characteristics of the asset class itself—namely illiquidity, valuation discretion, and concentration.

One of the central vulnerabilities of private credit that we have identified is the temporal mismatch between asset duration and capital expectations. Private credit funds deploy capital into long-duration, illiquid loans, yet the capital backing these investments—while more stable than bank deposits—is not entirely permanent. As the class of assets continues to institutionalize, a large share of capital is subject to reallocations. This creates sensitivity to shifts in investor sentiment even if there is an absence of immediate credit deterioration.

Furthermore, the absence of continuous price discovery introduces further aspects to risk. Portfolios from private credit companies are valued infrequently and rely on an internal assessment rather than market prices that are observable. This established practice within the private lending market has the ability to suppress short-term volatility, but in the long run it may delay the recognition of deteriorating credit conditions. The result of this mechanism is not necessarily mispricing, but rather lagged repricing, which can amplify movements once they occur.

Another aspect to risk is shaped by the composition of borrowers. Private credit has a disproportionate allocation to mid-size firms and sponsor-backed transactions. In these engagements capital structures are often more leveraged and operationally their operational resilience is more variable when we compare them to large investment corporations. In segments like these the performance is closely tied to refinancing conditions and earnings stability. As financing costs rise or growth slows, these borrowers become increasingly sensitive to credit tightening, introducing a cyclical dimension to default risk.

The concentration of exposures within similar economic channels is also a very important factor when we evaluate the risk of private credit. Portfolios are often built around deal types like leveraged buyouts or growth financing which leads to clustering. In essence, the clustering comes from overexposure in sectors like technology, healthcare and business. While theoretical diversification does exist, in practice many of the underlying drivers could remain correlated. This would be particularly troublesome in events of major macroeconomic downturns and other black swan event.

When we observe the credit system in its entirety, the increasing integration of private credit into institutional portfolios adds severe complexity to risk transmission. As pension funds, insurers, and asset managers expand their allocations, private credit becomes embedded within broader asset allocation frameworks. Inherently, this does not create excess risk, but we have grounds to argue about indirect linkages between private credit performance and the overall financial conditions.

To summarise, the defining characteristic of these vulnerabilities is the lack of visibility we have as a byproduct of this newly emerging industry. Unlike banks that are subject to very heavy restrictions under legal frameworks like Basel III and others, where they are limited in terms of liquidity, reporting and oversight, private credit risks are less obvious and more difficult to identify on a market level. This limits the ability of markets and policymakers to assess concentrations and respond preemptively. Therefore, we can deduce that the evolution of the credit market has not removed structural risk at all, but has altered the form of risk born by the market. The applied mechanism is less observable therefore difficult to assess and prevent future crises.

Conclusion

The expansion of private credit reflects a fundamental shift in the structure of modern financial markets. What began as a post-crisis adjustment to regulatory constraints has evolved into a core channel through which capital is allocated and risk is intermediated. Private credit has scaled not because it replaces banks, but because it operates effectively in segments where traditional banking models are no longer economically or structurally suited.

This evolution has improved the efficiency of credit allocation, aligning borrower demand for flexibility with investor demand for yield. At the same time, it has redefined the boundaries of the financial system, extending credit intermediation beyond the scope of traditional regulation and into a more distributed and less transparent environment.

The key implication is not that the system has become more or less risky, but that risk is now embedded in different forms and locations. Its visibility has decreased, even as its importance has grown.

Private credit is therefore not a temporary trend, but a structural feature of contemporary finance. Its continued expansion will depend not only on market demand, but on how effectively the system adapts to monitor and manage the risks it now carries.

Bibliography

Core Reports & Institutional Sources

International Monetary Fund (2023). Global Financial Stability Report. Washington, DC: IMF.

Bank for International Settlements (2022). Annual Economic Report. Basel: BIS.

Preqin (2024). Global Private Debt Report. London: Preqin.

McKinsey & Company (2023). Global Private Markets Review. McKinsey & Company.

Market Data & Industry Analysis

J.P. Morgan (2024). Private Credit Under the Microscope. J.P. Morgan Private Bank.

S&P Global (2025). Private Credit Market Insights. S&P Global Market Intelligence.

AIMA (2024). Global Private Credit Market Overview. AIMA.

Regulation & Frameworks

Basel Committee on Banking Supervision (2011). Basel III: A Global Regulatory Framework for More Resilient Banks and Banking Systems. Bank for International Settlements.

Academic & Foundational Research

Gary Gorton (2010). Slapped by the Invisible Hand: The Panic of 2007. Oxford University Press.

Atif Mian and Amir Sufi (2014). House of Debt. University of Chicago Press.

Supplementary Data Sources

World Bank (2023). Global Financial Development Report. Washington, DC.

OECD (2022). Financial Markets Trends. OECD Publishing.

All data used in this article is derived from publicly available institutional reports and industry analyses.

This article is for informational purposes only and does not constitute investment advice.

Mihail Gaydarov

Founder & Chief Financial Analyst

The Financier Review

© 2026 The Financier Review. All rights reserved.