Gold at $5,000: Safe Haven or the Market's Most Expensive Psychological Crutch?

Author: Alexandria Chaliovski

Introduction

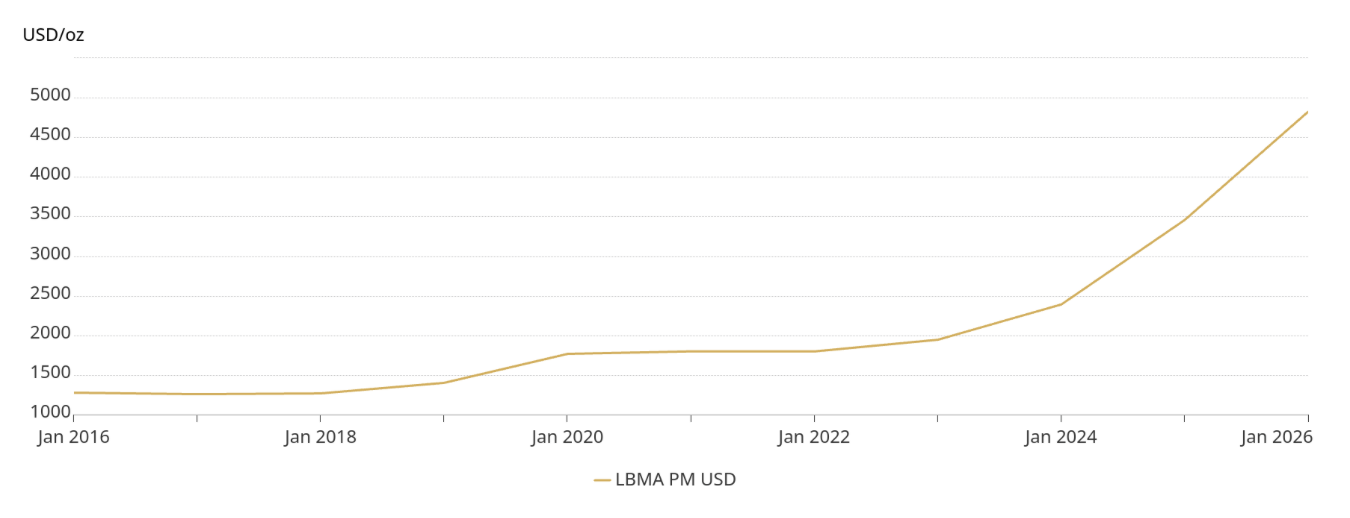

Gold broke $3,000 when Trump announced Liberation Day. Then $4,000 by October. Then $5,000 in January - achieving 53 all-time highs only in 2025. Every time it moved the causation were either inflation fears, geopolitical risks, or the dollar weakening. The safe haven story stated that gold was reliable, intuitive, but most importantly it was wrong. Actually, the change was not driven by retail investors fleeing inflation or institutions hedging tail risk. The central banks reduced their dependence on the U.S. dollar, while wealthy investors bet on long-term fiscal weaknesses and three years of pent-up ETF inflows finally turned positive again. This is not the typical safe haven behaviour and this is important because if you misidentify why something is rising, almost certainly you will misidentify when it stops.

Graph - Gold price milestones timeline

Source: World Gold Council

The Traditional Case For Gold And Why The Data Doesn’t Support It

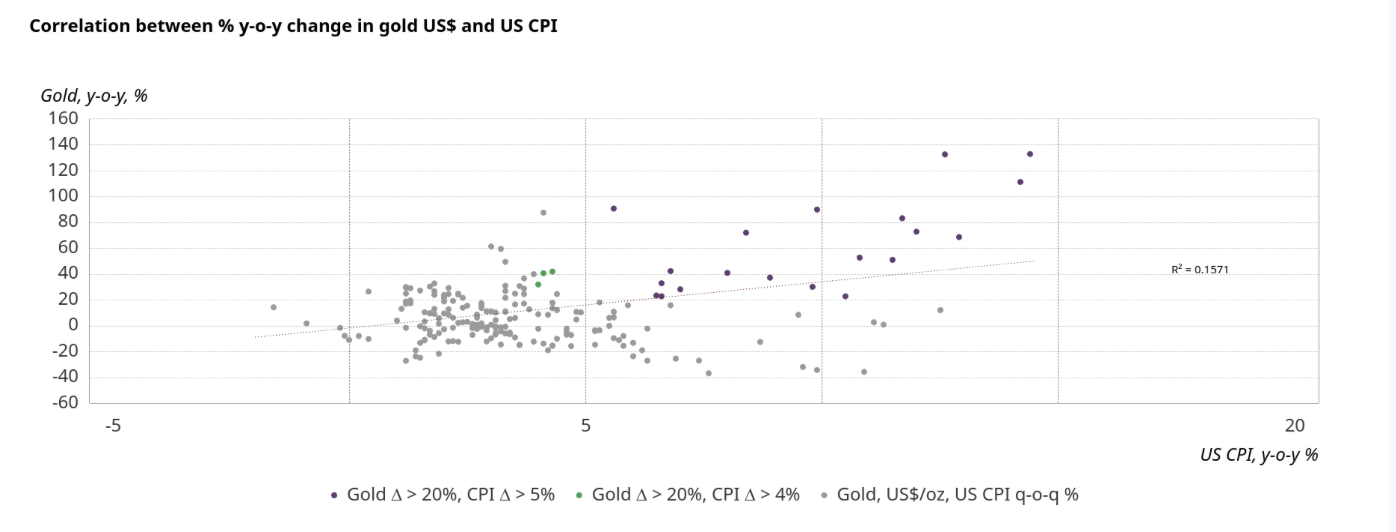

Very often gold is seen as an inflation hedge. Since it’s a real asset with finite supply, when central banks devalue paper currencies through excessive money printing, the purchasing value of gold remains and everything else decreases. However, that is not completely true. When we have short to medium horizons, the equation does not hold.

The World Gold Council published a research, acknowledging that since 1971 only 16% of the changes in gold prices could be explained in CPI inflation. The CFA Institute shows that the inflation relationship is unstable and often weak. In the 1970s gold delivered surprisingly good returns but during that period when oil shocks, the collapse of Bretton Woods, and a complete breakdown of monetary credibility happened simultaneously …. During the 2021-2022 inflation spike gold went nowhere for eighteen months and then its price increased. In 2021 specifically investors who bought gold to hedge their purchasing power spent two years being wrong before they bailed out due to completely different reasons.

Graph: Gold vs. CPI Inflation Correlation Scatter Plot

Source: World Gold Council

During the COVID crash in March 2020, when investors liquidated everything to meet margin calls, gold fell. It also reversed on Black Monday in 1987 after a one-day spike as the same dynamic played out. Therefore, gold has a pattern. Because it is one of the few assets in institutions that can sell quickly, in liquidity crises it tends to fall first. The safe premium returns after the crisis, not during it. That is a different and far less useful property than what most investors believe they are buying.

However, none of this means gold is worthless as a portfolio asset. It means that the commonly used reasons for holding it are frequently the wrong ones.

What actually Drove This Rally

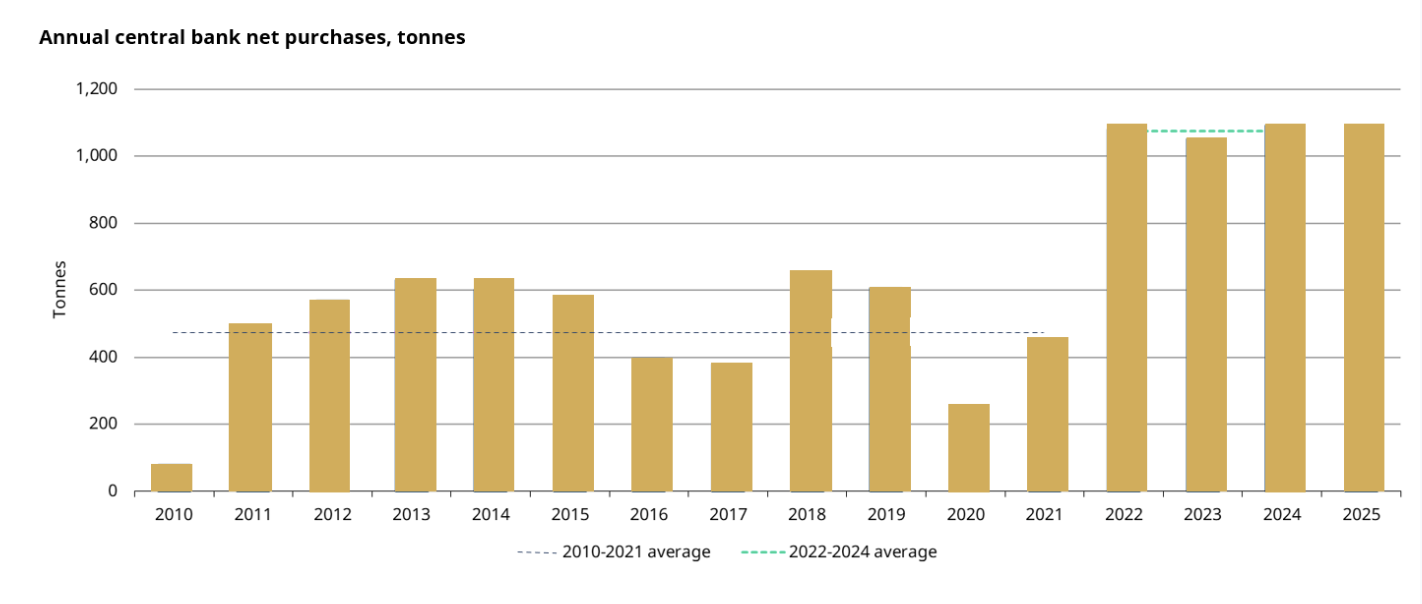

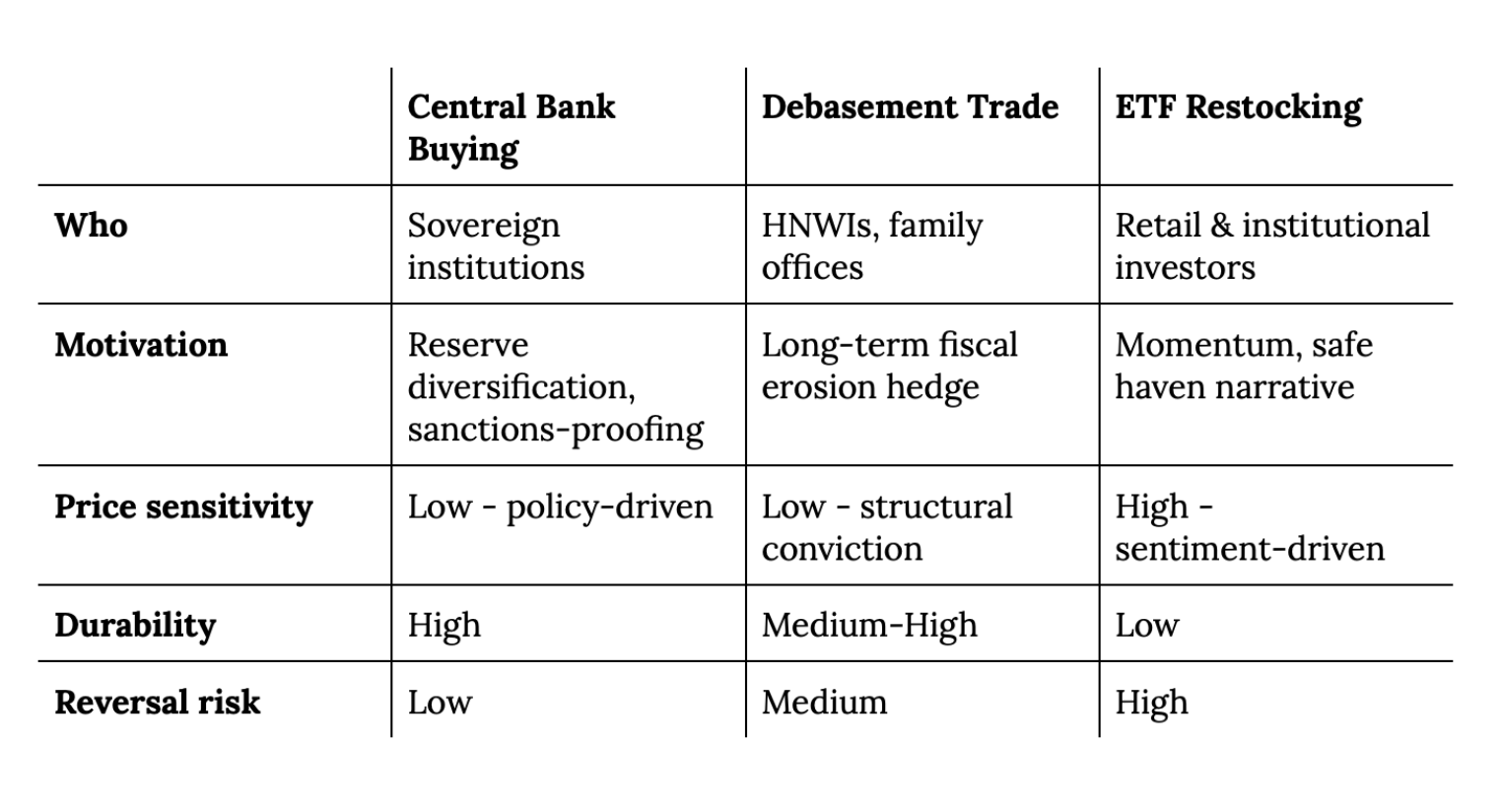

The first and most significant causation is the central bank reserve diversification - what markets have taken to calling de-dollarisation. Central banks have purchased over 1,000 tonnes of gold annually for three consecutive years from 2022 through 2024, which is more than double the average pre-2022 of 400-500 tonnes. In February of 2022, approximately $300 billion of Russia’s foreign exchange reserves were frozen overnight by the U.S., which is an unprecedented act that the majority of reserve managers noticed. This action could be translated into: dollar-denominated assets held offshore are not truly sovereign because they can be confiscated compared to the gold stored domestically which cannot. Using that move the U.S. and its allies send a message to every non-aligned government watching. For the first time since 1996, by 2025 central banks collectively hold more gold than the U.S. Treasury securities.

Graph: Central Bank Gold Purchases by Year, 2010–2025

Source: World Gold Council

The second driver is what Goldman Sachs called the “debasement trade” - a category of demand that did not feature in previous gold cycles. High-net-worth individuals, family offices, and institutional allocators are buying gold not because they are afraid of inflation but because they are worried of what will happen to the long-term fiscal trajectory of the U.S. government - in 2025 and 2026, questions about the Fed's independence have intensified. These investors are not buying a crisis hedge, they are making a multi-year bet that the structural conditions for monetary debasement are being assembled. These positions are marketed as “sticky” exactly because they are not triggered by any single economic release or geopolitical event.

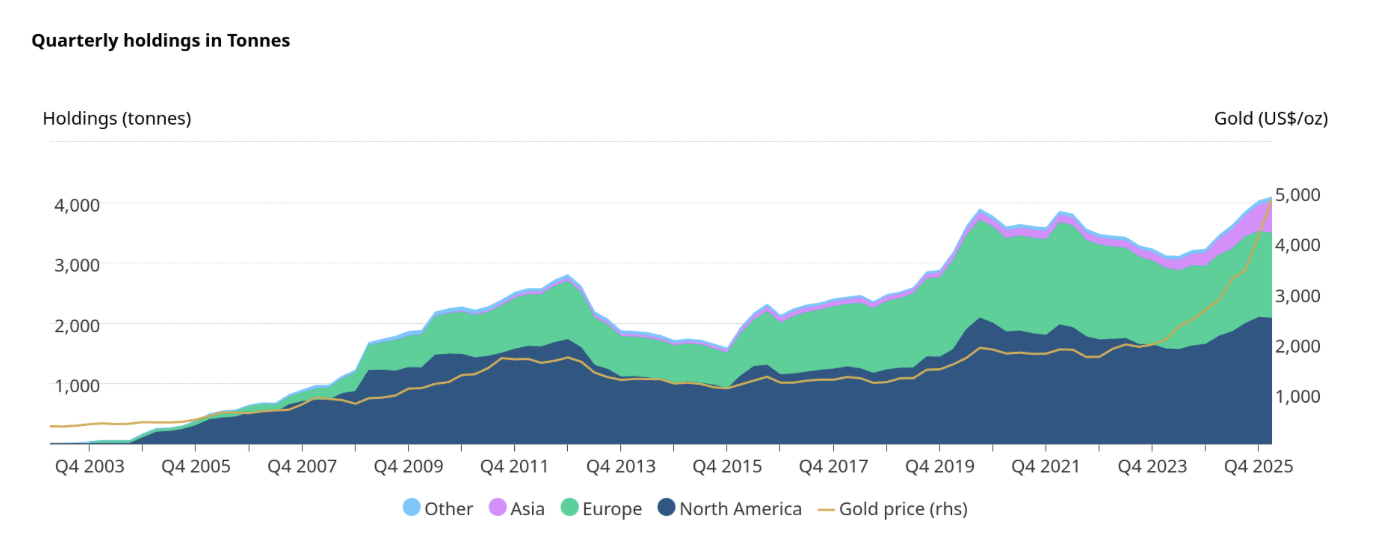

The third driver is ETF restocking. Unlike the first two, it is the least durable. From late 2020 to mid-2024, Western gold ETF investors were net sellers. When ETFs turned positive in 2025, the inflows were historic. That year, the World Gold Council reported that there have been $89 billion of ETF inflows, with AUM doubling to $559 billion, which are the largest amounts yet. North American funds led, adding tens of billions. But when in March 2026 Operational Epic Fury triggered broader risk-off conditions, U.S. investors sold gold ETFs to raise liquidity. Which means they sold their flowers and watered their weeds, which is not a safe haven behaviour at all. That is clearly momentum behaviour and momentum unwind.

Graph:Gold ETF Holdings 2004 - 2025: The Outflow and Reversal

Source: World Gold Council

Three Demand Drivers Comparison Table

The Reflexivity Problem

In modern markets gold is the purest example of a reflexivity-driven asset. It does not produce anything, pays no coupon, distributes no dividend, and does not generate earnings. There is no terminal cash flow to discount, no intrinsic value in the conventional financial sense. Its price is a product of the collective belief that other participants will also treat it as a store of value. That belief is not irrational because gold has held this role across thousands of years. But the mechanism is circular in a way most assets are not because gold is valuable due to the fact that people believe it is valuable due to its history.

At its current stage, this reflexivity is visible and trackable. When central banks buy gold, they reduce the current available supply to private markets, which pushes the price higher. The higher prices attract ETF inflows and retail buying, which makes the prices increase even further. However, J.P. Morgan managed to capture the mechanism – when the price is above $4,000 central banks do not need to buy as many tonnes to hit their desired percentage allocation, therefore the buying in volumes slows even if the price continues to rise. The World Gold Council confirmed this allegation.

However, that loop has an internal break and it is not infinite. The risk is not that gold will collapse, it is that the current price contains two different components that the markets treat as one – a structural floor (that is supported by sovereign demand and fiscal debasement) and a speculative premium (that is layered on top of that floor by momentum flows, ETF restocking, and narrative reinforcement). When the momentum deflates, it can temporarily look like the structural story is breaking even when it’s not.

The “Safe Haven” Paradox of 2026

Now comes the contradiction that the consensus narrative cannot fully explain. As of April 2026, if gold is a safe haven, then why are some central banks that used to be one of the most aggressive buyers now considering to sell?

A CNBC report from mid-April 2026 explained that war-driven pressures were forcing some central banks to sell gold in order to raise cash. Theoretically, the geopolitical crises should increase the value of gold, but in reality it is creating fiscal pressure severe enough that sovereign institutions are liquidating the asset that was supposed to protect them, which is also what happened back in 2020, when institutions sold gold to meet their margin calls. So, that is not a paradox. At the end, it turns out that at the level of short-term liquidity, gold is simply the most liquid asset institutions own, which means that it is often the first thing sold when cash is urgently needed.

Additionally, gold’s correlation with real yields has broken down this cycle in a way that the standard pricing models cannot fully explain. Historically, gold and real interest rates are inversely correlated - when real yields are negative, gold is attractive because it costs nothing to hold a relative compared to the alternative; when yields are high and positive gold should underperform. However, in 2025, gold’s prices grew even as real yields stayed elevated and that broke the relationship, used to explain most of gold’s behaviour over the past 50 years. This could mean the structural demand story is genuinely new and the old model needs updating, but it could also mean that current prices contain a premium, which will eventually mean-revert once the structural demand impulse moderates.

What Investors Should Be Thinking

Gold at $4,850 is not a bubble. The structural parameters - sovereign diversification, fiscal debasement risk, and ETF restocking, are real and it is unlikely that they will disappear quickly.

But gold at $4,850 is also not the straightforward safe haven that is currently described by many. It is a sovereignty hedge – an asset whose value is tightly linked with trust. Overall, it is considered as a durable trend but also a political one, which means that it can reverse with a speed that economic cycles cannot.

There are three possible scenarios. The bull case, which happens when de-dollarisation accelerates, the Fed loses independence, and real yields turn deeply negative. It concludes that gold will be above $6,000 by the end of the year and it is consistent with J.P. Morgan’s and Deutsche Bank’s upper-range forecast. In the base case, where central banks moderating purchases and ETF flows remain stable, gold stays in the range $4,000 - $5,000, while the speculative premium slowly bleeds out. And finally, the bear case which occurs when there is geopolitical de-escalation, the U.S. fiscal credibility is restored, and central banks increasingly sell gold due to the war-related cash needs. That is when gold corrects around 30 - 40% from the January highs, settling closer to the structural demand, where the central bank’s demand will stabilize it.

Taking a closer look, one can notice that none of these scenarios depend on the inflation rate. Therefore, investors who still frame gold as an inflation hedge are using the wrong model.

Conclusion

Gold increasing to $5,000 reflects something real. The structural forces behind it are not just some speculative fiction. But the price today is not made up only by those structural forces, it is a complex equation that sums them up with the reflexive premium, driven by momentum, narrative, and a safe haven story that the data has never fully supported.

Gold is not a safe haven in the classical sense. When monetary systems change negatively, it holds its value across long time zones and when monetary credibility is restored, gold is not valued. Also, it is the most liquid asset many institutions hold, making it the first thing that is being sold in a liquidity crunch and that is the opposite of what “safe haven” implies. In its current form, the bull market is being sustained by sovereign buyers, whose motivation is more political rather than financial.

The investors most likely to be right aren’t the ones who frame gold as an inflation or a crisis hedge but the ones who understand what they are actually buying - a bet that the institutions, underpinning dollar dominance, continue to erode and that no compelling alternative emerges fast enough to make gold’s role redundant. That bet may well be correct but it is a very different bet from the one that fills most gold brochures.

Bibliography

World Gold Council - Beyond CPI: Gold as a Strategic Inflation Hedge (2021) gold.org/goldhub/research/beyond-cpi-gold-as-a-strategic-inflation-hedge

World Gold Council - Gold ETF Flows: December 2025 (January 2026) gold.org/goldhub/research/gold-etfs-holdings-and-flows/2026/01

World Gold Council - Gold Outlook 2026 (December 2025) gold.org/goldhub/research/gold-outlook-2026

World Gold Council - Gold Demand Trends Full Year 2025: Central Banks (January 2026) gold.org/goldhub/research/gold-demand-trends/gold-demand-trends-full-year-2025/central-banks

World Gold Council - Gold Demand Trends Full Year 2025: Investment (January 2026) gold.org/goldhub/research/gold-demand-trends/gold-demand-trends-full-year-2025/investment

World Gold Council - Central Bank Gold Reserves by Country (updated February 2026) gold.org/goldhub/data/gold-reserves-by-country

World Gold Council - Gold ETF Holdings & Flows: Historical Data (updated monthly) gold.org/goldhub/data/gold-etfs-holdings-and-flows

World Gold Council - 2024 Central Bank Gold Reserves Survey (June 2024) gold.org/goldhub/data/2024-central-bank-gold-reserves-survey

J.P. Morgan Global Research - Gold Price Predictions 2026jpmorgan.com/insights/global-research/commodities/gold-prices

Goldman Sachs Research - Gold Forecast 2026, via TheStreet (February 2026) thestreet.com/investing/goldman-sachs-revamps-gold-price-target-for-the-rest-of-2026

CFA Institute Enterprising Investor - Gold and Inflation: An Unstable Relationship (June 2024) blogs.cfainstitute.org/investor/2024/06/05/gold-and-inflation-an-unstable-relationship

ScienceDirect - Is gold a hedge or safe-haven for inflation? Time-varying correlation in a multi-frequency framework (February 2026) sciencedirect.com/science/article/abs/pii/S0313592626000937

State Street Global Advisors - Could Gold ETF Inflows Spur Record Gold Prices in 2025? (January 2025) ssga.com/us/en/intermediary/insights/could-gold-etf-inflows-spur-record-gold-prices-in-2025

Finnish Institute of International Affairs - Western Financial Warfare and Russia's De-dollarization Strategy (May 2022) fiia.fi/en/publication/western-financial-warfare-and-russias-de-dollarization-strategy

Brookings Institution - What is the Status of Russia's Frozen Sovereign Assets? (2025) brookings.edu/articles/what-is-the-status-of-russias-frozen-sovereign-assets

Preprints.org - The Great De-Dollarization: How Gold Is Reshaping the Global Economy (March 2026) preprints.org/manuscript/202603.1197

ING Think - Gold's Bull Run to Continue in 2026 (December 2025) think.ing.com/articles/golds-bull-run-to-continue-in-2026

VanEck - Gold in 2025: A New Era of Structural Strength (2025) vaneck.com/us/en/blogs/gold-investing/gold-in-2025-a-new-era-of-structural-strength-and-enduring-appeal

NYCIF - Reflexivity: When Markets Create Their Own Reality (2026) nycif.org/reflexivity

Investing.com - Gold, Bitcoin: How Reflexivity Is Shaping Today's Market Narratives (March 2026) investing.com/analysis/gold-bitcoin-how-reflexivity-is-shaping-todays-market-narratives-200676265

Gainesville Coins - Historical Gold Prices: 50 Years of Market Lessons (2025) gainesvillecoins.com/blog/historical-gold-prices-market-events-lessons

Federal Reserve History - Recession of 1981–82federalreservehistory.org/essays/recession-of-1981-82

CNBC - Central Banks Were Buying Gold at Record Levels. Here's Why They're Selling Now (April 2026) cnbc.com/2026/04/15/central-banks-were-buying-gold-at-record-levels-why-are-they-selling-now.html

CEPR - The Russian Sanctions and Dollar Foreign Exchange Reserves (July 2024) cepr.org/voxeu/columns/russian-sanctions-and-dollar-foreign-exchange-reserves

Visual Capitalist - Charted: A Decade of Central Bank Gold Purchases (October 2025) visualcapitalist.com/sp/charted-a-decade-of-central-bank-gold-purchases

Amundi Research Center - Gold Beyond Records 2025: Central Banks & Market Trends (October 2025) research-center.amundi.com/article/gold-beyond-records

GoldSilver.com - Why Central Banks Are Buying Gold Again (March 2026) goldsilver.com/industry-news/article/why-central-banks-are-buying-gold-again

Trading Economics - Gold Spot Price XAU/USD (live data, accessed April 2026) tradingeconomics.com/commodity/gold

Macrotrends - Gold Prices: 100 Year Historical Chartmacrotrends.net/1333/historical-gold-prices-100-year-chart

Alexandria Chaliovski

Financial Analyst.

The Financier Review

© 2026 The Financier Review. All rights reserved.