The $725 Billion Question: Are Big Tech's AI Bets the Greatest Misallocation in History or Exactly Right?

Nvidia Headquarters - Santa Clara, California, United States of America.

Introduction

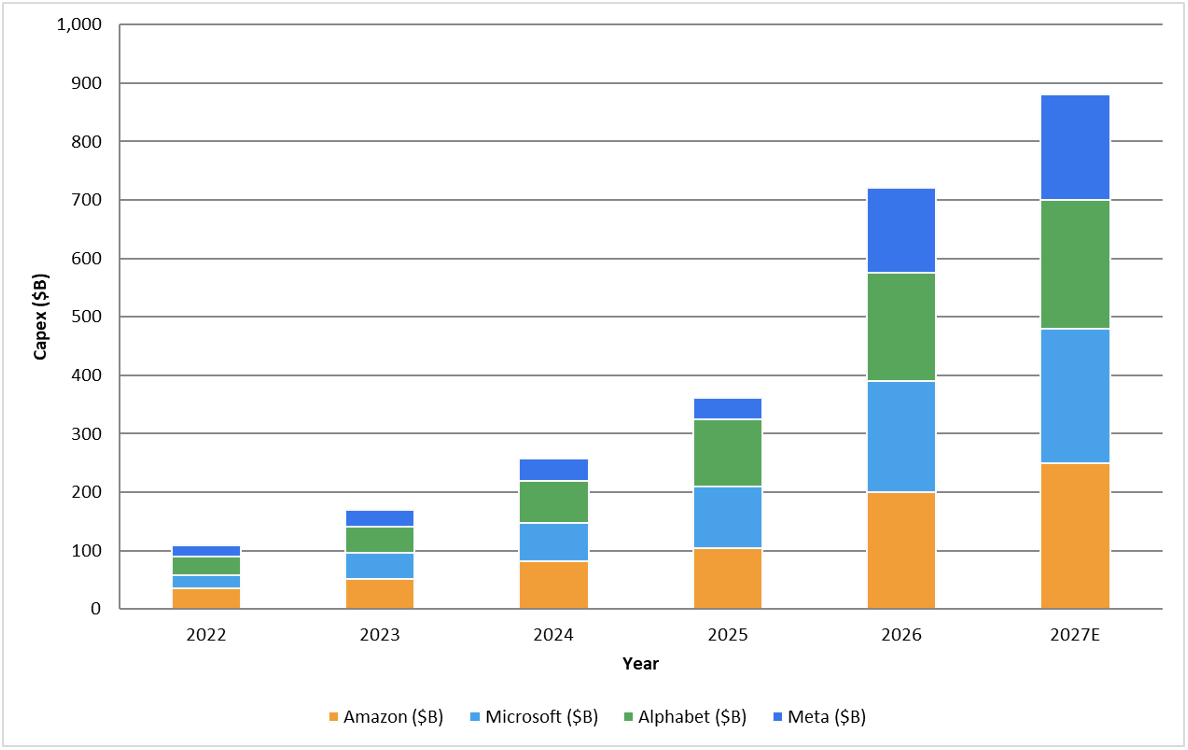

Meta, Microsoft, Alphabet, and Amazon are projected to spend $725 billion on AI infrastructure in 2026, which is up by 77% from 2025’s record $410 billion. Amazon plans on investing $200B, Microsoft - $190B, Alphabet around $180B and Meta - between $125 and $145B. In Q1 2026 alone, the four major companies spent around $112 billion combined and Wall Street is projecting that the amount will hit $1 trillion in 2027.

Graph - The Capex Escalation

Source: Bloomberg, Financial Times/Yahoo Finance, Tom’s Hardware, Statista, company earnings releases

Altogether, $725 billion is more than Sweden’s GDP (approximately $600B). It almost quadruples the Marshall Plan in today’s dollars. It also approaches the entire U.S. defence budget. And this is a sum, which is not being spent by governments but only by four corporations, making a wager on technology.

However, opinions on the matter have split into two main categories. Some financial analysts call this cycle the most important infrastructure investment since the internet. On the other hand, others believe it is similar to the dot-com case, where investors were excessively enthusiastic about internet-based companies which led to a market crash and to WorldCom and Global Crossing filing for bankruptcy. While both sides have some correct assumptions, none of them ask the harder questions. So, in the end, who is right?

The Market’s New Attitude

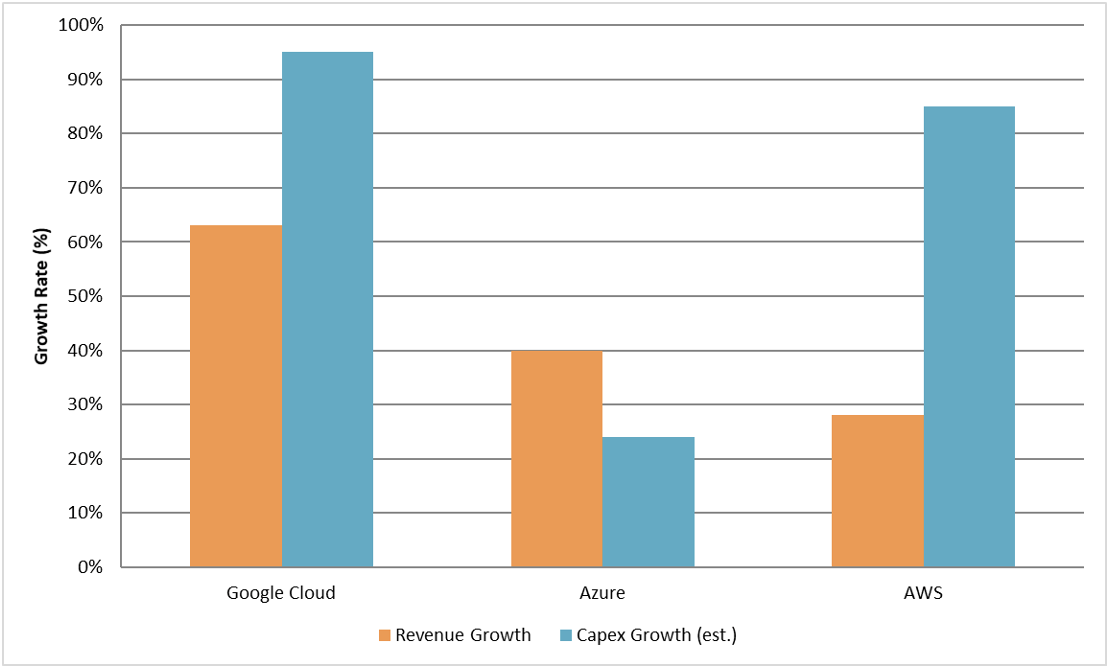

In 2023 and 2024, the AI market trend was: the bigger the spending expectations, the higher the stock price. However, in 2026 that dynamic has already shifted - now investors discriminate between companies showing revenue conversion and those that do not. But honestly, the AI capex cycle does not look like the dot-com bubble because, most importantly, revenues are actually materializing.

At Google, the market reacted positively. Google Cloud revenue reached a 63% increase compared to 2025, the RPO has nearly doubled from the previous quarter to $460B and net income has grown 81% to $62.6B. Microsoft’s AI business is at a $37B annual run rate, which means it is up 123% YoY. At the same time, Amazon’s Web Services growth is accelerating at 28%, with AI services at a $15 billion-plus annualised run rate. That is not just projections - these are audited financial results filed with the SEC.

Graph - Revenue vs. Capex - Are the Returns Keeping Up?

Source: Alphabet, Microsoft and Amazon earnings releases, MindStudio

Compared to these numbers, during the dot-com period the revenues that justified the infrastructure never materialised on any comparable timeline. The fibre-optic networks were laid in anticipation of internet traffic that was real but several years away. Whereas, the companies today are not building in advance of demand, they are building because they have capacity constraints. Microsoft’s CFO said that the company “expects to stay capacity constrained during 2026” despite $190 billion in annual spending.

This distinction is very important regarding how you value the bet. The question no longer is whether AI generates revenue because it clearly does. We ask ourselves if $725 billion is the right amount to spend to capture that revenue and who will end up holding the risk when the accounting catches up to reality.

The Trap Nobody Chose To Enter

Consider Google’s position. The company earns the overwhelming majority of its revenue from search advertising. If Microsoft builds a sufficiently capable AI assistant into every product it sells and if that assistant becomes the main tool from which people gain access to information, Google’s core business would face an extreme threat - structural replacement.

Given that fact, can Google choose not to spend? Evidence suggests that the answer to that is most likely no, which means that Google must match Microsoft’s investment even if its expected return on marginal capital might not be as …. At the same time, Microsoft faces the same logic in reverse - if Google achieves AI superiority, Microsoft’s cloud business faces potential catastrophe.

This is a classical prisoner’s dilemma. Each company’s individual rational decision produces a collective irrational outcome. The specific game theory term is a Nash equilibrium. The financial history term is a capital cycle. Anyhow, the outcome of both is the same - overinvestment together with margin compression and facing the unavoidable financial facts.

Will History Repeat Itself?

In the 1980s Cisco Systems was founded with the primary purpose of connecting disparate computer networks. Now, it has emerged to be one of the top-tier AI infrastructure companies. But between then and now, there have been a few setbacks.

In the 1990s networking equipment for the internet boomed. Stock grew 3,800% from 1995 to 2000. In March 2000 Cisco became the most valuable company in the world at a $555 billion market cap. However, that same year the speculative bubble of internet-based startups burst, leading to shares falling with 88% (from $79 to $9.50) and it took the company around 25 years to reclaim its dot-com peak.

Looking into the bigger picture, one could see that the situation was a lot worse than first anticipated. Between 1997 and 2001, over $90 billion were invested in high-speed optical cable in the telecom industry. By 2001, only 2.6% of that was actually being utilised. Between 2000 and 2002, $2 trillion in market value was erased and with it seventy-seven companies including WorldCom and Global Crossing.

And yet, the infrastructure itself was not wasted. The fibre-optic cable that was classified as “dark” (unlit and unused) in 2001 became the foundation of broadband internet, cloud computing, and video streaming for the next decade. Yes, the investors that financed it lost everything but the world gained a tool that transformed everything - the internet.

What happened before is a bit similar to what is happening now - the infrastructure that is being built today (data centers, power grids, networking fabric) may turn out to be transformational regardless of what returns the companies earn on their investment.

Where the Analogy Breaks Down

But here comes the diversification from its historical predecessors. Fibre cable does not become outdated. Once it is in the ground it remains capable of carrying traffic indefinitely. The investment was “an idea before its time”. But eventually demand caught up.

Compared to that, AI chips are fundamentally different. They are tied to the quick performance improvements and the rising efficiency standards. With every new generation, the cost and energy required for training and running AI models rapidly decreases. That is why older chips quickly become less competitive and it means that data centers need to replace hardware within a few years to remain competitive and economically viable. So, while dark fibre was a long-term investment waiting for the demand, AI chips are short-lived computing assets, which depreciate as fast as technology advances.

The financial risk in the current situation comes from how quickly AI chops lose their value. Currently, big tech companies spread GPUs’ costs over five - six years in their accounting but with the new chips arriving almost every year, older hardware may become outdated faster. Firms still argue that older GPUs can be reused for less advanced AI tasks which would expand their lifespan. But this only works if the demand for those lower-tier workloads keeps growing fast enough in order to absorb the outdated hardware. If it does not, companies will be left with large amounts of aging chips, which are worth less than expected, and that would force them to recognise bigger losses in future earnings reports.

Who Is Actually Right?

The honest answer is that both sides have some truthful conclusions and the resolution depends on these two variables which cannot yet be measured with confidence. The bulls are right that the revenues are materialising faster than the dot-com era suggested. Google’s $462 billion cloud backlog represents signed contracts, the majority of which are expected to generate income in 24 months and Microsoft’s $37 billion AI run rate growing at 123% annually is not a narrative. The demand is real.

Microsoft building in Vancouver, BC, Canada.

However, the bears are right that the accounting hides the true costs, the GPU depreciation creates a structural risk that fibre-optic cable never faced and the coordination trap means that the industry spends more than it is socially optimal regardless of individual company rationality.

The question here is whether the GPU model will hold - whether older hardware retains sufficient economic utility to justify the current depreciation or not and whether cloud revenue growth can sustain current rates long enough for the AI capex cycle to generate acceptable free cash flow.

The Rational Response For Investors

The investor’s problem is that none of these analyses show a clear winning strategy.

History tells us that the companies making the largest bets in transformative technology rarely capture the majority of the value that they create. Standard Oil built the current energy economy, the railroad barons built the infrastructure that industrialised America, Cisco and the telcos built the basis of the internet.

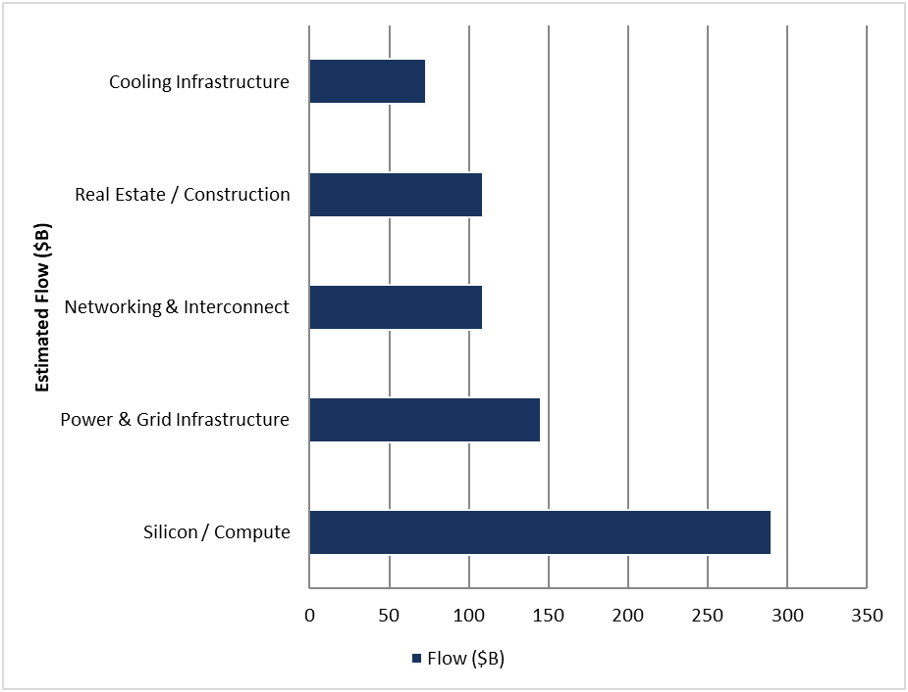

In this scenario, the best choice for investors is to use the picks-and-shovels principle. When the Gold Rush happened in California, the merchants selling mining equipment generated more returns than the miners themselves. Applying this to the current AI capex cycle we can see that roughly 40% of the massive capital expenditures (capex) dedicated to Artificial Intelligence by large cloud service providers are being spent on purchasing AI chips - primarily from Nvidia. Nvidia’s revenue depends on the investments in the whole industry. The risks are the other players on the market (Amazon’s Trainium, Google’s TPU, Microsoft’s Maia) which might eventually displace Nvidia.

Graph - Where the $725B flows through the supply chain

Source: Goldman Sachs, McKinsey, Forbes

The more overlooked opportunity is power infrastructure. AI data centers consume a lot of energy, for example a large-scale facility can absorb as much electricity as a small city. The build-out creates decade-long contracted demand for utilities, grid infrastructure, and power equipment manufacturers that is structurally protected from which AI company dominates in the model race.

Conclusion

The question of whether this is the greatest misallocation of capital in history or a perfectly justified investment cycle does not have a simple answer.

Clearly, it is not the dot-com bubble case and it is not rational capital allocation either. What it mostly resembles is a technology transition with transformative potential which is being funded at a pace that exceeds what any individual return-on-capital calculation would justify because the strategic cost of under-investing is existential for each player. The fibre-optic networks that were built in the 1990s powered the 21st-century internet. The AI infrastructure that is being built today will power the next decade.

Whether the companies building it will be compensated for the risk - that is the $725 billion question and the honest answer is that nobody clearly knows.

— The Financier ReviewAll data used in this article is derived from publicly available institutional reports and industry analyses.

This article is for informational purposes only and does not constitute investment advice.

Bibliography

Bloomberg - US Big Tech Ratchets Up AI Spending Past $700 Billion This Year (2026) bloomberg.com/news/articles/2026-04-30/us-big-tech-ratchets-up-ai-spending-past-7 00-billion-this-year

Financial Times / Yahoo Finance - Google, Microsoft, Meta, and Amazon Capex Spending to Hit $725 Billion in 2026 (2026)

finance.yahoo.com/sectors/technology/articles/google-microsoft-meta-amazon-capex-1 31823436.html

Statista - Big Tech’s AI Spending to Reach $725 Billion in 2026 (2026)

statista.com/chart/35046/capital-expenditure-of-meta-alphabet-amazon-and-microsoft Meta Investor Relations - Meta Reports First Quarter 2026 Results (2026)

Microsoft Investor Relations - FY2026 Q3 Earnings Release (2026) microsoft.com/en-us/Investor/earnings/FY-2026-Q3/press-release-webcast

Alphabet Investor Relations - Alphabet Q1 2026 Earnings Call (2026)

abc.xyz/investor/events/event-details/2026/2026-Q1-Earnings-Call-2026-nW8kCrBAKS /default.aspx

Yahoo Finance - Alphabet Q1 2026 Earnings Call Transcript (2026)

finance.yahoo.com/quote/GOOGL/earnings/GOOGL-Q1-2026-earnings_call-551989.htm l

Barron’s - Alphabet Earnings: Google Cloud Backlog and AI Capex (2026) barrons.com/articles/alphabet-earnings-stock-price-c55b88e7

Amazon Investor Relations - Amazon.com Announces First Quarter Results (2026) ir.aboutamazon.com/news-release/news-release-details/2026/Amazon-com-Announces -First-Quarter-Results/default.aspx

Business Insider - Amazon Q1 Earnings: AWS Growth, AI Capex and Chip Run Rate (2026) businessinsider.com/amazon-q1-earnings-amzn-stock-price-aws-ai-capex-2026-4

CRN - Cloud Market Share Q1 2026: AWS, Microsoft and Google Battling in AI Era (2026) crn.com/news/cloud/2026/cloud-market-share-q1-2026-aws-microsoft-google-battling -in-ai-era

Goldman Sachs - Tracking Trillions: The Assumptions Shaping the Scale of the AI

Build-Out (2026)

Goldman Sachs - Why AI Companies May Invest More Than $500 Billion in 2026 (2025) goldmansachs.com/insights/articles/why-ai-companies-may-invest-more-than-500-billi on-in-2026

World Bank - GDP, Current US Dollars: Sweden (2025) data.worldbank.org/indicator/NY.GDP.MKTP.CD?locations=SE

U.S. Senate Appropriations Committee - FY2026 Defense Appropriations Bill Summary (2026)

appropriations.senate.gov/imo/media/doc/fy26_defense_bill_summary_conferenced.p df

Deseret News - Cisco Surpasses Microsoft as World’s Most Valuable Company (2000) deseret.com/2000/4/2/19499571/cisco-surpasses-microsoft-as-world-s-most-valuablecompany

SFGate - Cisco Passes Microsoft in Worth (2000) sfgate.com/bayarea/article/cisco-passes-microsoft-in-worth-san-jose-firm-2766856.php

Barron’s - Cisco Was the Dot-Com Bust’s Biggest Loser. Now It’s at a 25-Year High (2026) barrons.com/articles/cisco-stock-ai-nasdaq-243fbc23

National Law Review - Deep Quarry: Useful Lives of GPUs - Key Considerations (2026) natlawreview.com/article/deep-quarry-useful-lives-gpus-key-considerations

SiliconANGLE - Resetting GPU Depreciation: AI Factories Bend, Don’t Break Useful-Life Assumptions (2025)

Barron’s - AI Networking: It Isn’t Just Nvidia (2026)

barrons.com/articles/ai-networking-nvidia-cisco-broadcom-arista-bce88c76

Forbes - The $725 Billion AI Spending Surge Is Missing the Real Bottleneck (2026) forbes.com/sites/jonmarkman/2026/04/30/the-725-billion-ai-spending-surge-is-missi ng-the-real-bottleneck

MindStudio - Google Cloud vs AWS vs Azure Q1 2026: Which Hyperscaler Is Winning the AI Infrastructure Race? (2026) mindstudio.ai/blog/google-cloud-vs-aws-vs-azure-q1-2026-ai-infrastructure-race

McKinsey - The Cost of Compute: A $7 Trillion Race to Scale Data Centers (2025) mckinsey.com/industries/technology-media-and-telecommunications/our-insights/the -cost-of-compute-a-7-trillion-dollar-race-to-scale-data-centers

IoT Analytics - Data Center Infrastructure Market: AI-Driven CapEx Pushing IT and

Infrastructure Spending (2025) iot-analytics.com/data-center-infrastructure-market Deloitte - 2026 Semiconductor Industry Outlook (2026)

Bain & Company - Prepare for the Coming AI Chip Shortage (2024) bain.com/insights/prepare-for-the-coming-ai-chip-shortage-tech-report-2024

Goldman Sachs - AI to Drive 165% Increase in Data Center Power Demand by 2030 (2024) goldmansachs.com/insights/articles/ai-to-drive-165-increase-in-data-center-power-de mand-by-2030

IEA - Electricity 2026: Analysis and Forecast to 2028 (2026) iea.org/reports/electricity-2026

Alexandria Chaliovski

Financial Analyst.

Mihail Gaydarov - Article Role: Editor.

Chief Financial Analyst

The Financier Review

© 2026 The Financier Review. All rights reserved.