Profit in the Crossfire: Energy and Tech Giants cash in as the Iran conflict shakes Global Markets

Photo by Leo_Visions on Unsplash

Hormuz Goes Dark.

Since the end of February the war in the Middle East is keeping the world on its toes, but even the months-long closure of the Strait of Hormuz has nоt had the expected derailing impact on the world economy yet.

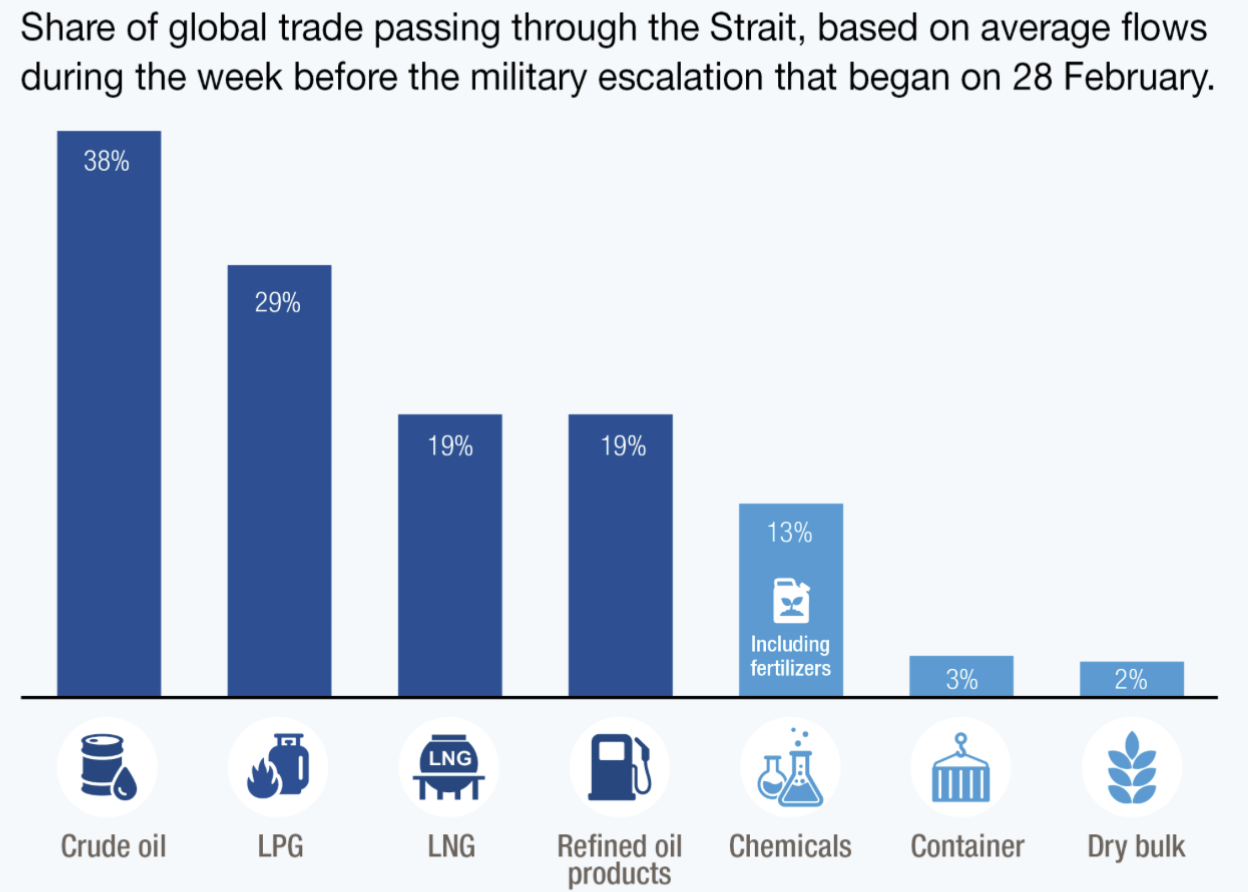

On paper the hostilities should impact almost all economic sectors due to the risks they create for oil and natural gas exporters. After the initial strikes between U.S. / Israel and Iran the conflict has significantly spread to other Gulf nations, with Iran hitting key regional infrastructure targets such as the Ras Raffan gas complex in Qatar, which has stopped operating and therefore has contributed to the decrease of global LNG supply by 17%. Additionally, the major problem is the leverage Iran has on account of the Strait of Hormuz, that is a key maritime area, responsible not only for the transport of around a quarter of the world’s seaborne oil, but also accounts for huge amounts of the LPG and LNG trade. Recently an advisor to the Iranian Supreme Leader defined it as an “atomic bomb”, that gives to those controlling it the power to influence the global economy with a single decision. (Andrews & Baldwin, 2026)

Source: UN Trade and Development (UNCTAD), based on data provided by Clarksons Research 2026.

Iran formally closed the Strait at the beginning of March and by the end of the month the country had enforced the blockade via attacks, mines and various shipping disruptions. The closure has continued until April 17, when a brief reopening was introduced under the conditions of a ceasefire, but tensions remained and as of now, the area remains almost entirely closed, with ongoing instabilities and tanker rerouting. Recently an officer in the Islamic Revolutionary Guard Corps (IRGC) has revealed the newly developed definition that IRGC has of the Strait of Hormuz - not a narrow stretch, but an increased in scope and military importance maritime territory. The redefinition is perturbing and implies the intention of Iran to augment the range of the blockade.

The first glimmer of hope that the conflict may come to an end was the initial Ceasefire Deal that came after a couple of weeks of negotiation - the U.S. has originally proposed a one-month ceasefire on March 25, but Iran rejected it due to suspicions that the U.S. and Israel would use it to regroup and hit harder later on. However, Iran came up with a 10-point plan as a counter proposal that became the common ground for the temporary truce. On April 21, President Trump indefinitely extended the ceasefire. On the one hand, he did not want to lift the blockade on Iranian ports, imposed by the U.S. as a response to the closure of the Strait of Hormuz by Iran, on the other hand the hostilities were not appealing to Washington either. As of May 12 the ceasefire is still in place, but appears to be extremely fragile. After some strike exchanges on May 7 - 8, a few days later Donald Trump has defined it as being on “massive life support”, which was immediately reflected in the oil prices - a rise of 4% was noted for the international oil benchmark on May 11. (Staff, 2026)

In the last week there have been talks between Washington and representatives from Tehran about a permanent truce under the conditions of opening the Strait of Hormuz and indefinitely halting any military actions. However, it appears that Trump has rejected the latest proposition from Iran.

The attention now shifts to the role, which China could possibly play. Xi Jinping already met with Iran’s foreign minister, Araghchi, last week. The two discussed the circumstances, under which the Strait of Hormuz would be opened, as well as the need for stable ceasefire conditions. Now a meeting between the Chinese and American presidents is underway. The new sanctions from May 11 against companies that facilitate exports of Iranian oil to China are a sign that Trump intends to use Beijing to push Iran into accepting his terms. Even though the U.S. president has rejected the claim that he needs Chinese intervention, forcing one of Iran’s greatest allies to cooperate would be crucial for the American cause.

Macroeconomic effects and financial stability risks.

The uncertainties about the future of the conflict further increase the preoccupations regarding the macroeconomic stability of the world’s economy. Even the Federal Reserve has noted the geopolitical risks in its semi-annual Financial Stability Report. The current political disruptions in the Middle East as well as the resulting oil price shocks are marked as the most significant threats to the U.S. financial system. The Fed states that the war may disturb the economy through several interconnected channels. (Financial Stability Report)

Inflation and the Risks It Creates

The immediate concern after the war started was related to the expectations of a new inflation wave across sectors and regions.

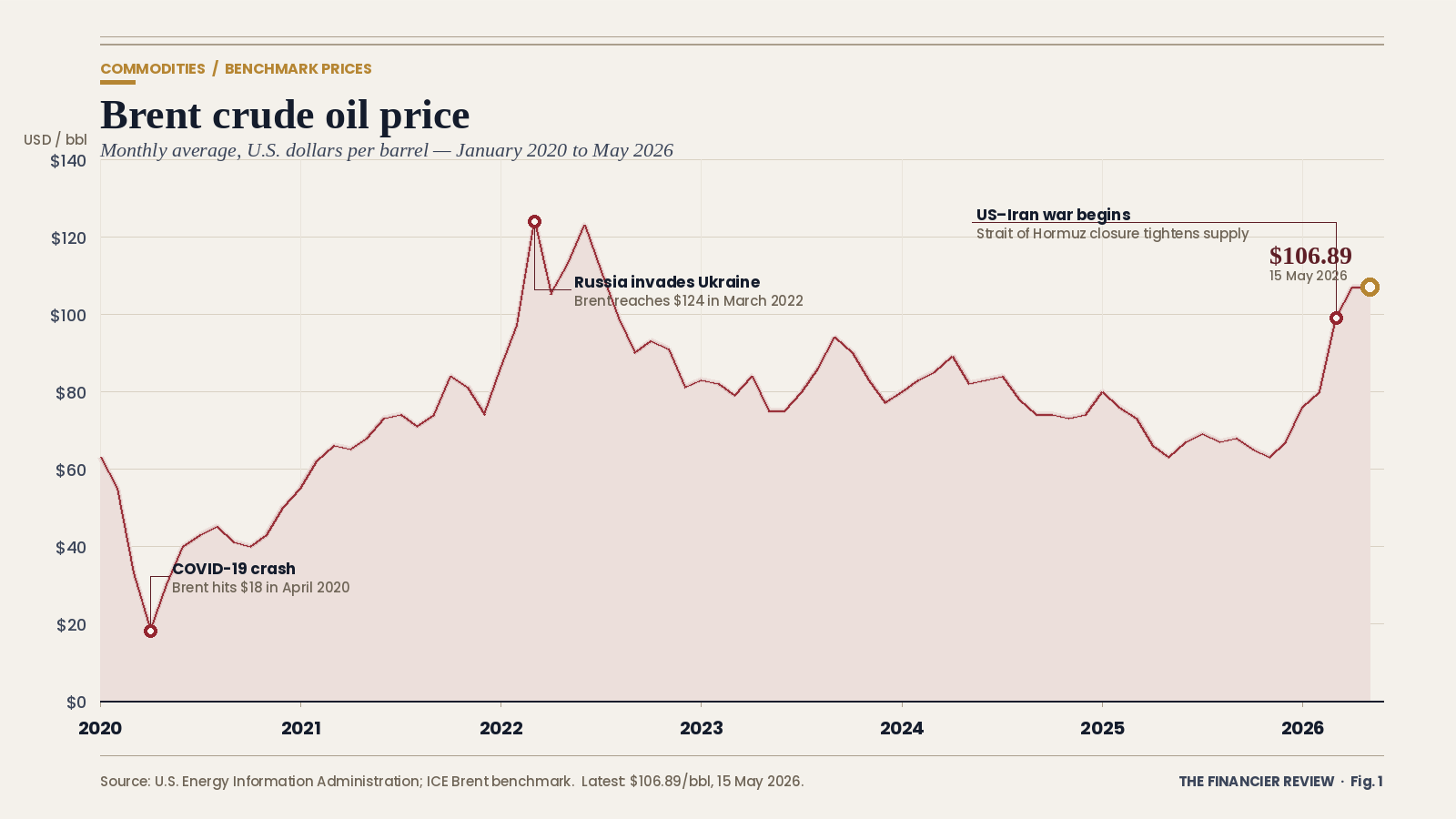

The most obvious price increase risk is that of the oil and gas products’ prices. Since 2022 the petroleum market particularly in Europe has experienced several shocks and therefore was on a shaky ground even before the conflict started. Now with the reduced trade of such products the prices were expected to surge immensely. The continuous talks about those risks created a preposition for speculations in many countries, increasing the inflation furthermore. In the U.S., for example, gas prices surged by 21% and were the primary driver of the spike in inflation levels in March - up to 3.3%. Additionally, the persistence of the crisis contributes to inflation expectations. J.P. Morgan has predicted for oil prices to stay in the “low $100” per barrel for the rest of the year, even if the Strait of Hormuz opens within a week. (Chia & Race, 2026)

Graph Design: TFR.

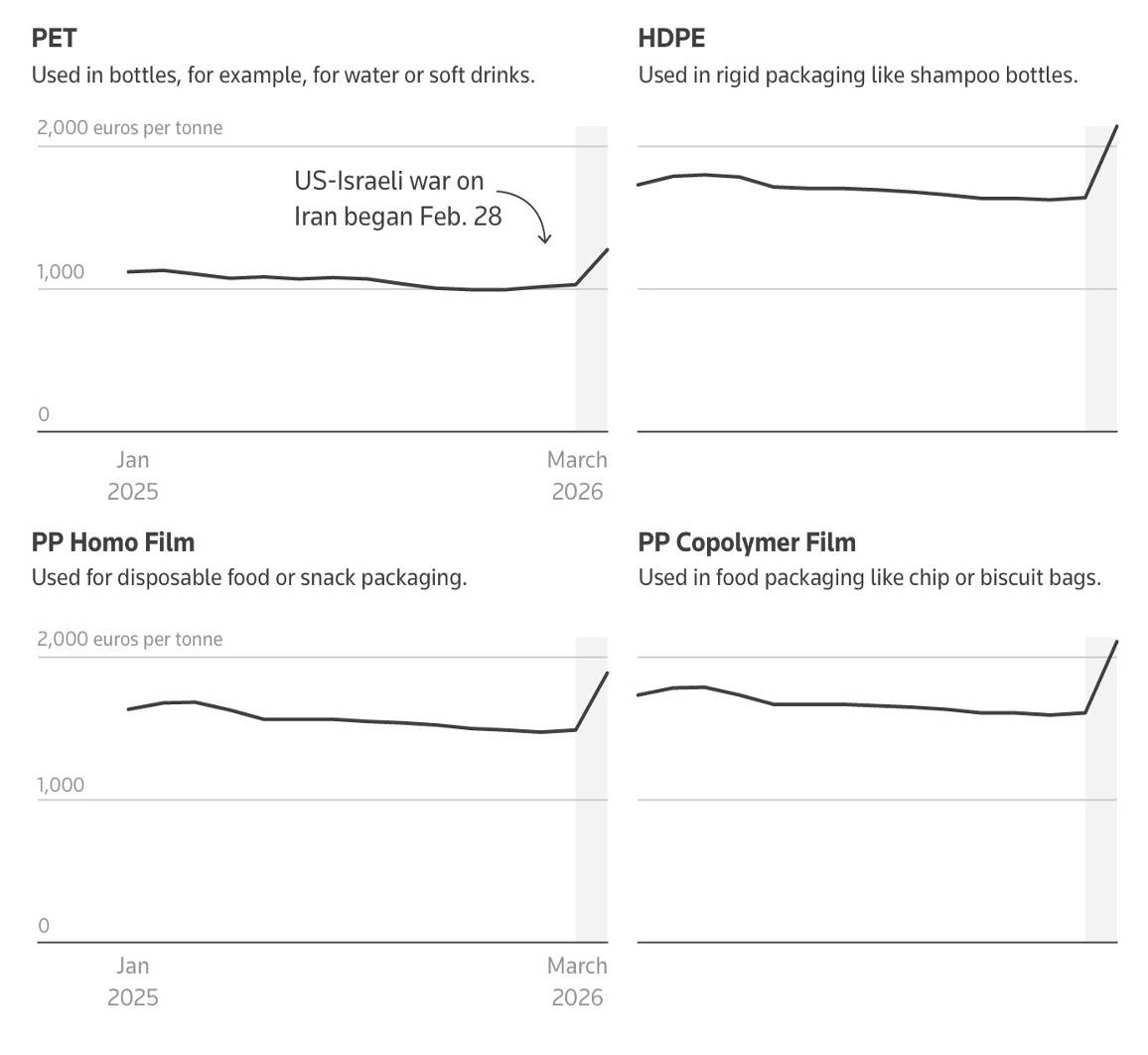

But even with excluded volatile food and energy prices, core inflation stays above target - at around 2.6% in the U.S. The dependence on petroleum products, that many industries characterize with, is another key factor when it comes to inflation spike risks. In a research made for Reuters by NielsenIQ the data showed a very rapid rise in the prices of several consumer goods from disposables all the way to almost any plastic packaged product there is. (Aluckal et al., 2026)

Data source: Plastics Information Europe; Graphics: Reuters

And those are only the initial market reactions provoked by the surge in oil prices. A second-round of price effects are expected when the crisis finally hits the Asian petro-chemical industry. Chinese refineries are starting to cut production and close due not only to the higher costs, but also to the reduced supply of crude oil derivatives. There is just not enough input for the industry to keep working at full pace. Increased prices of fossil fuels impact other industries as well. Means of transportation, especially the aviation industry are severely impacted, tourism also suffers due to the disrupted aerial routes.

Inflation is perceived as a risk for the global economy also due to the related regulatory capital implication and the following recognition risk-like repercussions. With prices rising, the central banks would eventually need to adjust the interest rates, and when those are higher a “Fair Value” problem emerges for many financial institutions that usually hold fixed-rate assets like Treasury bonds and Mortgage-backed securities, whose market value declines compared to the increasing flexible interest rates’ returns. Many banks hold similar impaired assets in HTM accounts recorded as regulatory capital. Additionally, rising prices trigger central counterparties (CCPs) to significantly increase margin requirements supposed to cover default risks. This often results in a sudden need of liquidity that is easily satisfied by trading fixed-rate assets that are already compromised. But such sales must be recognised as a reduction of the banks’ regulatory capital, therefore creating future risks when it comes to crisis management potential.

EconomicResilience and Monetary Policy

However, despite all the reactions, the global economy has shown to be surprisingly resilient. Goldman Sachs chief economist Jan Hatzius has described it as “bending, not breaking” and according to him there are three main reasons for this unexpected endurance.

First of all he mentions the unusually high inventories of crude oil supplies across the world before the start of the war. Moreover, product shortages on a regional level have been dealt with through insignificant decreases in supply and demand - aerospace corporations for example were among the biggest losers at the start of the war, but gradually the situation improved due to the decreased demand. The artificial intelligence industry boom has also supported stock markets by providing alternative, fossil-independent growth opportunities. (Conley, 2026)

And the Monetary Policy trends support that view of the current state of the global economy. The Fed has held interest rates steady so far at a target range of 3.5% - 3.75%. But the inflationary trends may make the intention of the next chair of the Federal Reserve Kevin Warsh to lower the interest rates harder to complete - experts forecast a delay in the cuts until at least 2027. (Mitchell, 2026) In the UK, the bank of England is also maintaining interest rates’ levels at 3.75%, but has warned that in the worst case scenario the inflation may hit values above 6%, when multiple rate rises would be necessary. ECB has also kept rate levels, but if the conflict continues, a second-round of inflation would be inevitable and rates would be forcibly adjusted.

Despite the precarious conditions, the major economic actors have maintained their interest rates at the pre-war levels as of the middle of May. And the overall picture of the economy seems better than anticipated at the beginning of the conflict.

Winners, Losers, and the

In-Between.

Financial markets' response so far remains surprising. Even if the initial better-than-expected situation could be explained by high oil reserves, those are now starting to reach dangerously low levels, but financial markets do not seem to care. The narrative that compares the current situation with the one from 2022, combined with the constantly emerging news of permanent peace hopes help stabilise the market responses, despite the obvious threats.

Equity markets initially suffered from the shocking start of the war, then stabilized for a couple of weeks, but as hopes of a quick resolution faded away, stocks started to fall down again. And the same trend was apparent across multiple industries, with the exception of the oil majors as well as to some extent tech-giants that are perceived as safe havens with lower exposures to broader economic shocks. Bond markets have not responded in a single coordinated move, but with several bouts of volatility. Ten-year government bonds have surged in prices and short-term ones experienced even larger increases. Therefore, similar fixed-rate investments still are a lucrative portfolio diversification option, especially given the fact that central banks are still holding interest-rate levels. But if the conflict intensifies they may quickly become “Fair Value” problems.

Of course, this global resilience layout is not applicable to the same extent everywhere. Here is an analysis of the different regional financial markets that intends to show the exact effect the war has had on each of them.

The American Financial Market

The U.S. were not among the most impacted countries by the war, despite the fact that they play a crucial role in the conflict. There was lower exposure to oil price shocks - as the world’s top oil producer and net exporter, the country is not as vulnerable to supply shocks in the sector. The country even benefited by the vague dollar appreciation that emerged as a reaction to the fluctuations of the euro. The ongoing peace-talks also help stabilise the situations - even though investors do not completely believe Trump about his estimations of the length of the conflict, they believe his intentions for it to come to an end sooner rather than later. (Baker, 2026)

Additionally, S&P 500 and Nasdaq Composite both have marked record high values recently. This surge is explainable by the fact that the U.S. has been at the center of the boom in AI related investments. The tech industry provides a strong fossil-independent engine of growth that doesn’t suffer from direct negative consequences from the war.

Asian Markets

Similar are the reasons behind the spikes in some Asian technology-based stock markets - South Korea’s benchmark Kospi index, Taiwan’s Taiex index and Japan’s benchmark Nikkei 225 all have hit record highs in the last weeks. Asian markets have felt the crisis more heavily than the American ones, due to their dependence on petroleum imports, especially crude oil and LNG from the Gulf region. But the AI popularity compensates for the expected decline in consumer spending. South Korea for example benefits from being a major player in the semiconductor industry and the country’s equity market is now the seventh largest globally. Japan’s success is also the result of AI, semiconductor producers and data center-related companies that account for almost half of Nikkei 225 weight. (Towfighi, 2026)

European Financial Markets

The influence the AI hype has on Asian markets success becomes evident through the comparison with the European stock markets. The EU countries are also heavily dependent on fossil fuel prices since the continent is a net importer as well, but the lack of tech industry contributes to the negative trends in the financial markets. Since the beginning of the war Europe’s benchmark STOXX 600 index is down almost 2%, despite the 5% increase it has marked in February. (Towfighi, 2026) The long-term bond surges have also had an impact on many of the smaller European economies. According to surveys released by S&P Global in mid-April there has been a sharp fall

of business activity in the euro area. The Eurozone Composite PMI has fallen below 50, which indicates contraction rather than growth trends. But the decrease accounts for the service sector, while paradoxically manufacturing seems to be glowing, but the surge there is rather a reflection of larger input orders aimed to compensate for future shortages. The IMF also downgraded the eurozone in its latest Report, predicting lower growth rates. However, April’s PMI data doesn’t show signs of recession yet, so despite its vulnerability the European economy appears to be resilient as well. (Cingari, 2026)

The Gulf states and their role in the Petrodollar system

The region most affected by the war is the region where the war unfolds. With the closure of the Strait of Hormuz the biggest leverage the Gulf states have has been almost completely neutralized - the halt of oil and LNG export disturbs their entire economic systems due to the countries’ high dependence on fossil fuels trade, more than 50% of the governments’ incomes builds through energy sales. The fact that civil key infrastructure has been targeted by missile and drone strikes additionally complicates the situation. Secondary income channels like the well developed tourism sector were also suspended due to the war. The Gulf states not only have lost access to their primary means of income, but now they need to cover reparatory military defensive response costs.

The Gulf nations play an important role in the Petrodollar system and the threats they are exposed to may force them to reconsider their relations with the U.S. The Petrodollar depends on, firstly, the U.S. oil demand channels, that ensure dollar priced energy sales and secondly, the agreement that the Gulf nations would reinvest the revenues in American companies for the exchange of U.S. promise to secure the region. And the war threatens all of those dependencies: Even before the conflict, the Gulf states have started to diversify their export destinations while the U.S. has gradually become a net oil exporter, so the American need for Middle East fuels decreases. If another country becomes the main importer of Gulf energy then the dollar would probably stop being the main exchange currency method. Consequently the ties that provoque the return of dollars to the U.S. in the form of various investments would also fall out. With the war, the Gulf countries already start reconsidering the amounts they reinvest mainly in American companies and would probably redirect some of that money toward securing their own recovery from the conflict. And here comes the undervalued implication this war might have for the American stock markets - if investments for U.S. firms decrease (and those firms are primarily AI and Tech Giants) then even the technological orientation of the industry would not be able to compensate for consumer spending losses and the markets might lose their resilience. (Patterson, 2026)

The War Profiteers'

Quarterly Report

Behind the moral and ethical arguments that serve as an ideological front in every conflict, there is often a deeper motive, usually closely tied to personal benefit. So the question is: who would be the winner this time?

First of all, let’s take a look into the sectors and the companies that can gain the most.

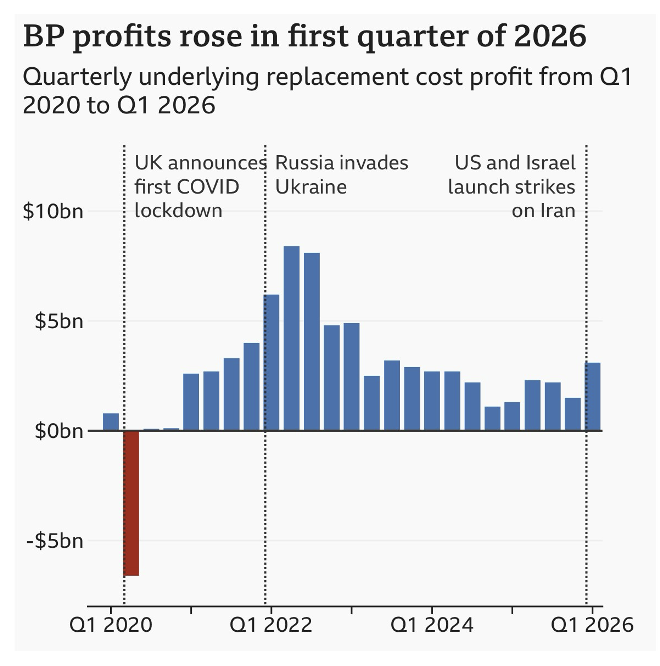

The most obvious winners from the conflict are the companies in the fossil fuel sector that can only benefit from the higher prices due to lower supply levels. Only for the first quarter of 2026 BP’s profits almost doubled.

Source: BP; Graphic: BBC

Shell and TotalEnergies also marked huge profit margins. U.S. oil companies are not as successful but have benefited from the situations well. Another logical beneficiary is the Aerospace and Defence Industry. It has started to mark increased revenues last year, when most of the European NATO countries agreed to increase their defence budgets. However, the new military conflict has boosted the sector’s demand and has contributed to a further increase in revenues.

Major investment banks have also capitalized on the war so far. The volatility risks that arose from the war have triggered investors to trade assets and financial institutions have responded as mediaries, therefore increasing their profits. But that could work only in the short term, experts warn, as the longer the conflict gets, the more alerted investors become, and the less trade deals happen.

The renewable energy sector has also experienced a positive trend. Many economic actors are exposed to the fossil fuel price shocks, as this war is the third major crisis this decade that triggers a surge in traditional energy prices. Many Asian countries, that have been hit the most, have recently introduced tax incentives and other similar measures to stimulate at-home solar panel installations and different renewable energy projects. China is the main solar panel producer and therefore has also benefited from the increasing interest in such products.

The war has had a positive economic and geopolitical influence for some particular countries as well, even though the overall effects are usually either mixed or negative. When it comes to currencies, the U.S. dollar has appreciated, firstly because of the Euro devaluation, but also because it is usually perceived as rather safe. Therefore, demand for dollar secured assets has emerged with the beginning of the war. Additionally, the States are gradually establishing themselves as the main oil net exporter partner for Europe for example. Global Affairs (Miller & Clark, 2026) has stated that the war has helped Beijing to project an image of global stability and responsible leadership. Russia also gains indirectly, because the diminished supply has weakened the sanction imposed previously, which has helped the country to diversify once again its exports portfolio.

The Bill Comes Due.

Global markets have proved to be more resilient than expected during the first two months of the war in Iran, despite high economic pressures. Events like the closure of the Strait of Hormuz and the attacks on Gulf oil and gas infrastructure are considered main forerunners of inflationary and stability risks around the globe. However, sufficient oil inventories, experience with energy crises, central banks caution, hopes of rather quick resolution and spikes in AI-driven economic sectors have contributed to the absorption of risk so far.

A main takeaway from the conflict is the capacity of war not only to destroy values, but to redistribute profits across the economic system. Households, governments and oil-dependent industries have borne the majority of the costs, while energy giants, defence companies, banks and technology firms have found a way to cash in in times of scarcity, insecurity and volatility.

For some the longevity of the conflict may present endless opportunities to increase profit margins, but with regard to the accumulative effects, the longer the crisis continues, the bigger the risks become. Deepening energy shortages, possible decrease of Gulf reinvestments and long-term increase of investors cautiousness, combined with diminished consumer spending capabilities may deepen the economic crisis and force the world into recession-like conditions. Even the apparent winners may struggle as a result of a prolonged conflict: One of the major consequences of the war is the acceleratory effect of structural change. Debates about energy independence through increase in domestic renewable energy productions may threaten the fossil fuel hegemony and contribute to fundamental structural changes in the global economy.

— The Financier ReviewAll data used in this article is derived from publicly available institutional reports and industry analyses.

This article is for informational purposes only and does not constitute investment advice.

References

Aluckal, A. J., Naidu, R., & Kiyada, S. (2026, April 30). How the Iran war is driving up the cost of your shopping cart. Reuters.

https://www.reuters.com/graphics/IRAN-CRISIS/OIL-CONSUMERS/akpeyyn mypr/

Andrews, F., & Baldwin, S. L. (2026, May 8). Trump says Iran’s response to peace proposal “totally unacceptable.” CBS News.

https://www.cbsnews.com/live-updates/iran-war-trump-us-attacks-qeshm-islan d-ceasefire/

Baker, W. (2026, April 24). Why are stock markets surging despite Iran crisis? The

Week.

https://theweek.com/business/economy/why-are-stock-markets-surging-despit

e-iran-crisis

Board of Governors of the Federal Reserve System. (2026). Financial stability report, may 2026.

Chia, O., & Race, M. (2026, May 11). Oil price predicted to remain above $100 for rest of year. BBC News. https://www.bbc.com/news/articles/ckgp4ev4yg4o

Cingari, P. (2026, April 23). Euronews.com. Euronews.

https://www.euronews.com/business/2026/04/23/iran-war-effects-on-europe-is

-a-recession-already-unfolding

Conley, J. (2026, May 11). “Bending, not breaking”: Goldman Sachs explains why the war in Iran hasn’t derailed the global economy. Yahoo Finance.

https://finance.yahoo.com/economy/article/bending-not-breaking-goldman-sac hs-explains-why-the-war-in-iran-hasnt-derailed-the-global-economy-13354205

8.html

Hale, E. (2026, April 17). Iran war’s big winners: Wall Street, weapons firms, AI and green energy. Al Jazeera.

Khan, S. (2026, March 25). Gulf war tests the foundations of the petrodollar. Modern

Diplomacy. https://moderndiplomacy.eu/2026/03/25/gulf-war-tests-the-foundations-of-thepetrodollar/

Miller, A. P., & Clark, M. (2026, April 17). The iran war is a win for china. Foreign

Affairs.

https://www.foreignaffairs.com/united-states/iran-war-win-china?check_loggedin=1&utmmedium=promo_email&utm_source=lo_flows&utm_campaign=arti cle_link&utm_term=article_email&utm_content=20260509

Mitchell, A. (2026a, April 29). Four key takeaways from Jerome Powell’s final rate decision as Fed chair. BBC News.

https://www.bbc.com/news/articles/c62rm4zk3kgo

Mitchell, A. (2026b, May 8). The companies making billions from the Iran war. BBC

News. https://www.bbc.com/news/articles/ce8pyyz5e0ro

Patterson, R. (2026, May 1). Disappearing gulf capital: The iran war risk wall street isn’t watching. Council on Foreign Relations.

https://www.cfr.org/articles/disappearing-gulf-capital-the-iran-war-risk-wall-stre et-isnt-watching

Rizve, S. (2026, April 24). Who is profiting from the US-Iran War? The Business

Standard.

https://www.tbsnews.net/features/panorama/who-profiting-us-iran-war-142052

6

Staff, A. J. (2026, May 8). What we know about Iran’s response to the latest US ceasefire proposal. Al Jazeera.

https://www.aljazeera.com/news/2026/5/8/what-we-know-about-irans-respons e-to-the-latest-us-ceasefire-proposal

Strait of Hormuz disruptions: Implications for global trade and development. (2026,

March 10). UN Trade and Development (UNCTAD).

https://unctad.org/publication/strait-hormuz-disruptions-implications-global-tra de-and-development

Towfighi, J. (2026, May 7). Market rebound: Why some stocks are looking past the

Iran war. CNN.

https://edition.cnn.com/2026/05/07/investing/global-stocks-iran-war

Edit Dukova

Financial Analyst.

Mihail Gaydarov - Article Role: Editor.

Chief Financial Analyst

The Financier Review

© 2026 The Financier Review. All rights reserved.