Beyond Wall Street: Can Investors Truly Diversify Away from U.S. Markets?

New York Stock Exchange, Photo by Aditya Vyas on Unsplash

Article Authors: Mihail Gaydarov, Nikolay Marinski.

Introduction - The illusion of Global diversification.

The construction of a modern portfolio for an investor is often built around the idea of global diversification. An average investor is often advised to veer towards allocating capital across assets, regions and currencies with the aim to mitigate concentration risk and create predictable long-term returns. In practice, however, the mission of diversifying a portfolio is often heavily anchored to a single financial system: that of the United States.

The sheer dominance of the American capital markets is evident in the structure of the world’s major benchmarks commonly utilized by investors. As of early 2026, the U.S. market accounts for about 70% of the MSCI World Index. This implies that investors tracking a broad developed-market index are overwhelmingly influenced by the United States. Although an investor might consider that they monitor a “global” portfolio most of the structure of that portfolio is exposed to American equities. If we look more broadly on the global equity market, the United States represents roughly half of the total equity market capitalisation - holding a key role in the architecture of international finance.

The concentration of the U.S. extends far beyond equity markets. The U.S. Dollar is the dominant reserve and transaction currency, accounting for over 55% of global exchange reserves and 89% of global foreign exchange market trades. American financial institutions and asset managers play a central role in allocating capital across international markets. As a result of this dominance in the trade exchange sector and asset management, U.S. monetary policy, treasury yields and equity valuations often influence other financial systems worldwide.

These vulnerabilities include geopolitical uncertainty and policy instability may pose significant future risks. Amidst all, congressional disapproval and poor political support also do not provide a layer of confidence for the future of the United States securities markets. These downturns can rapidly transmit volatility to portfolios that seem to be global and diversified.

Rather than accepting the dominance of the United States in the securities market, it is possible to design a portfolio that reduces reliance on U.S. markets while maintaining long-term stability with a reasonable compromise on returns (in comparison to a standardised U.S.-oriented portfolio).

Ultimately resulting in the question:

“Can a portfolio meaningfully decouple from Wall Street, or is the global financial system simply too interconnected for such independence to exist?”

Structural Channels of the U.S. Influence - A Deep Dive.

In order to evaluate to what extent investors can reduce dependence on American markets, it is essential to understand why the financial influence of the United States is so pervasive. The large global finance share of the United States is not simply a result of the American marker size. The firm position is asserted through several structural mechanisms that anchor international trade, corporate activity, and capital flows to the U.S. financial system.

We have identified three channels that are particularly important to our case:

The Dominance of the U.S. Dollar

Corporate Integration with the U.S. economy

Financial Market transmission through American monetary policy and capital markets.

Dollar Dominance in Global Finance

The U.S. dollar occupies a unique position in the international monetary system. It is not merely the national currency of the United States, but it takes the function of the central currency of the global economy.

The functionality of money is commonly broken down into four main pillars: a unit of account, a medium of exchange, a store of value and a funding currency.

Many internationally traded goods are priced in dollars, even when the U.S. is not involved in the trade. This is especially true for gold, oil and gas, industrial and agriculturalcommodities and shipping. This is also known as domain currency pricing (DCP). Because prices become more rigid in dollar terms when compared to exporters’ domestic currencies, movements in the dollar exchange rate exert an economy-wide effect globally, making the dollar a central macroeconomic variable.

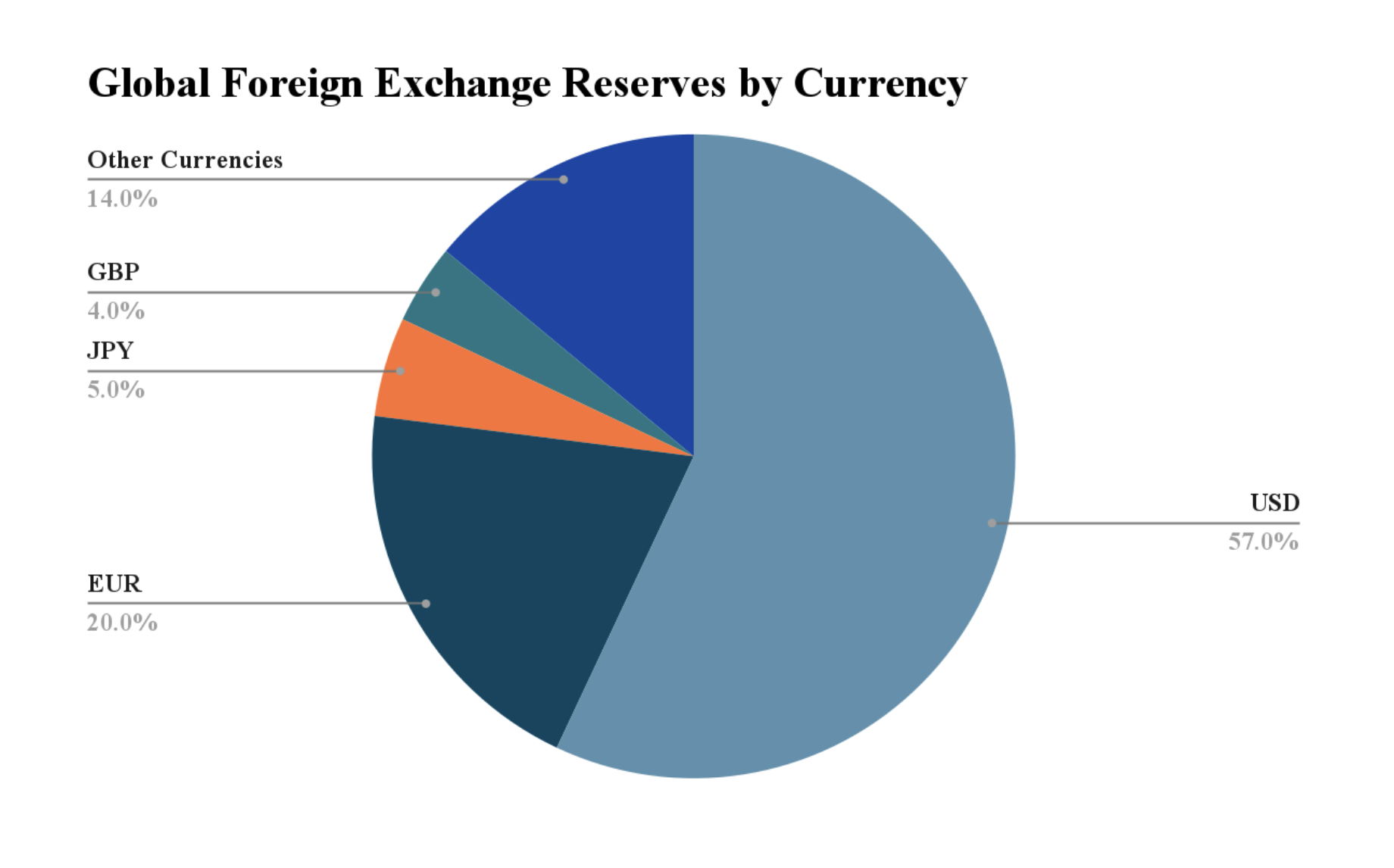

According to the IMF (International Monetary Fund), the United States Dollar accounted for 56-57% of global foreign-exchange reserves in 2025. In comparison to other currencies like the euro and other major notes, the dollar displayed a significant authority over the others (as shown by the chart below).

The significant prominence of the dollar is also present and more pronounced in global currency markets. Credible data gathered from the Bank of International Settlements indicate that the dollar has a 89% involvement in all foreign-exchange transactions worldwide. The central role that the dollar has taken in international trade has profound implications on investors. Due to the fact that international trade, commodities pricing, and cross-border financial flows are largely priced in ($) USD. Furthermore, monetary policy decisions made by the U.S. Federal Reserve influence financial conditions well beyond the American economy.

When the interest rates in the U.S. rise, capital tends to flow towards dollar-priced assets, strengthening the position of the dollar and pressuring financial conditions in other emerging markets. Conversely, periods of U.S. monetary easing can inject liquidity back into markets. Thus said, even portfolios that are composed primarily of foreign assets therefore remain tied to the dollar liquidity cycle, indirectly.

Corporate integration with the U.S. economy

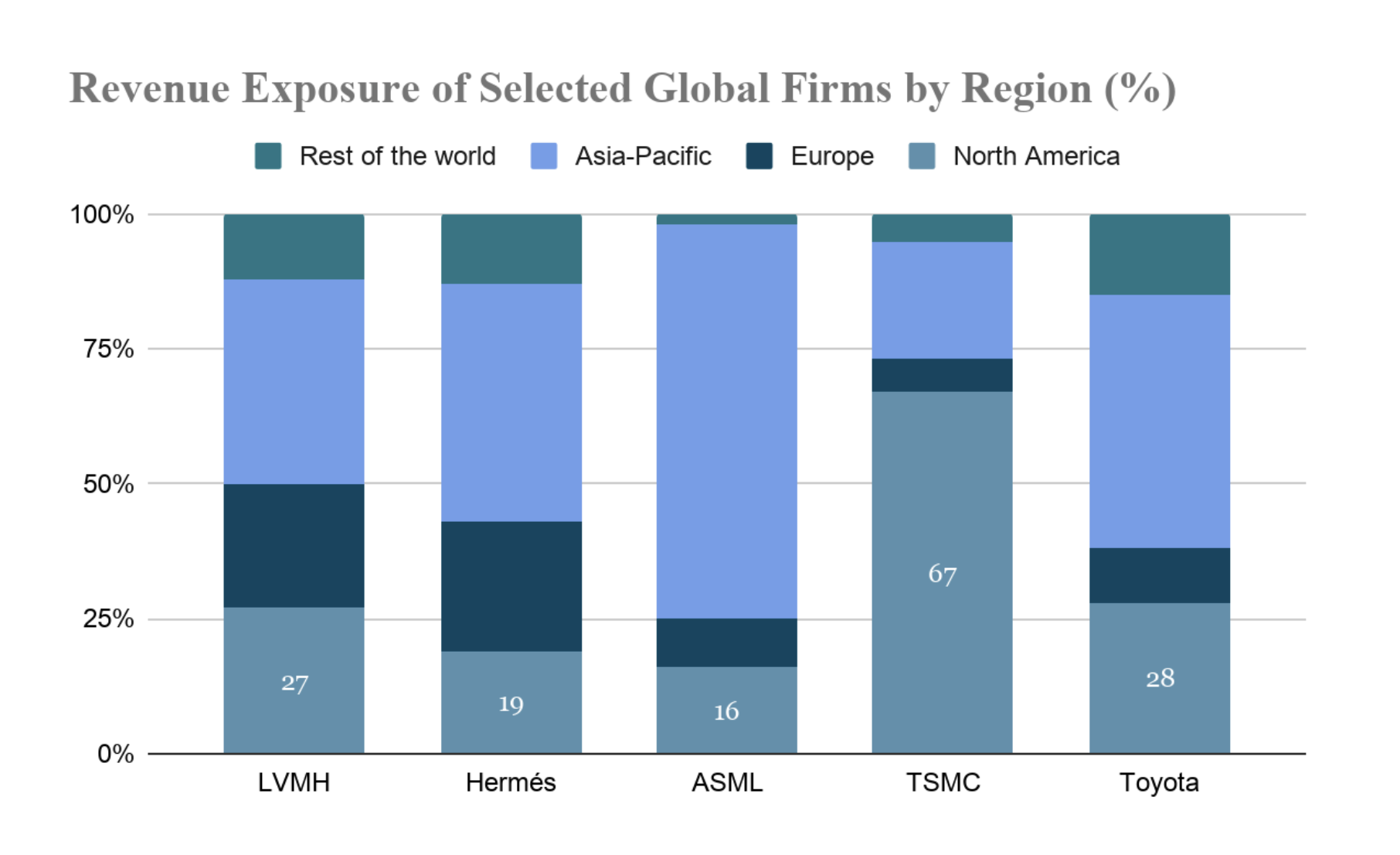

Firms outside the United States are often deeply embedded in the U.S.-centred production networks, consumer markets, capital structures, and regulatory environments, making it more than just bilateral trade. The channel emerges from the economic importance of the Americanconsumer and their corporate markets. With the United States having one of the largest consumer markets in the world, a revenue dependence is created with a direct demand-transmission mechanism through which changes in the U.S. consumption, investment or market conditions can be correlated with the stability of foreignfirms.

The United States, to this date, remains one of the wealthiest large economies in the world and, as mentioned, a very valuable customer to most export businesses outside of the US. IMF data suggests that for 2025 the U.S GDP per capita is positioned at about $92,000. Compared to other countries that are classified as large economies like Russia and India, the American consumer has exceptionally high levels of purchasing power parity relative to these other global economies. For instance, Russia has a GDP per capita of $17,287, which is less than ¼ of that of an American. This significant wealth advantage translates into substantial demand and the ability to purchase imported goods in categories such as luxuryproducts, technology, and other premium services.

As a result, many corporations that do not operate within the premises of the United States depend heavily on revenue that is generated within the Americanmarket. European luxury goods, international consumer brands and semiconductor manufacturers all rely to some extent on demand from the United States. Moreover, the critical infrastructure foundation, which the U.S. tech giants have built, puts every sector in a state of partial dependence, especially for the sectors of e-commerce, fintech, media, manufacturing, and, in recent times, Artificial Intelligence.

Ultimately, this dynamic implies that most of the time, even geographical diversification is majorly limited. A company that operates in Asia or the EU may still receive revenue from conducting business within the U.S. , making it dependent on American consumers and corporate investments. In practical terms, an investor holding foreign equities may still be indirectly exposed to fluctuations in the U.S. business cycle and consumer spending environment.

-> Graph note: “TSMC’s main client is the U.S.”

Financial Market Transmission

As we briefly discussed in the points we made prior, beyond trade and corporate revenues, global financial markets are also prone to another limitation from the United States. They are heavily interconnected through the transmission of U.S. monetary and fiscal conditions. In practice, movements that are originating in American markets have the tendency to set the trend across international financial systems, which influences asset prices far beyond the United States.

Arguably the most important channel through which this propagation occurs is through U.S. monetary policy. Decisions that are made by the United States Federal Reserve, or in short form FED affect global liquidity conditions because rates set in the U.S. act as a benchmark for international capital flows. When the Chair of the Federal Reserve decides to tighten monetary policy, all of a sudden assets become much more attractive to investors. The circulating capital tends to flow towards dollar-denominated securities, which further strengthens the position of the dollar. Which in turn, tightens the financial conditions in other economies.

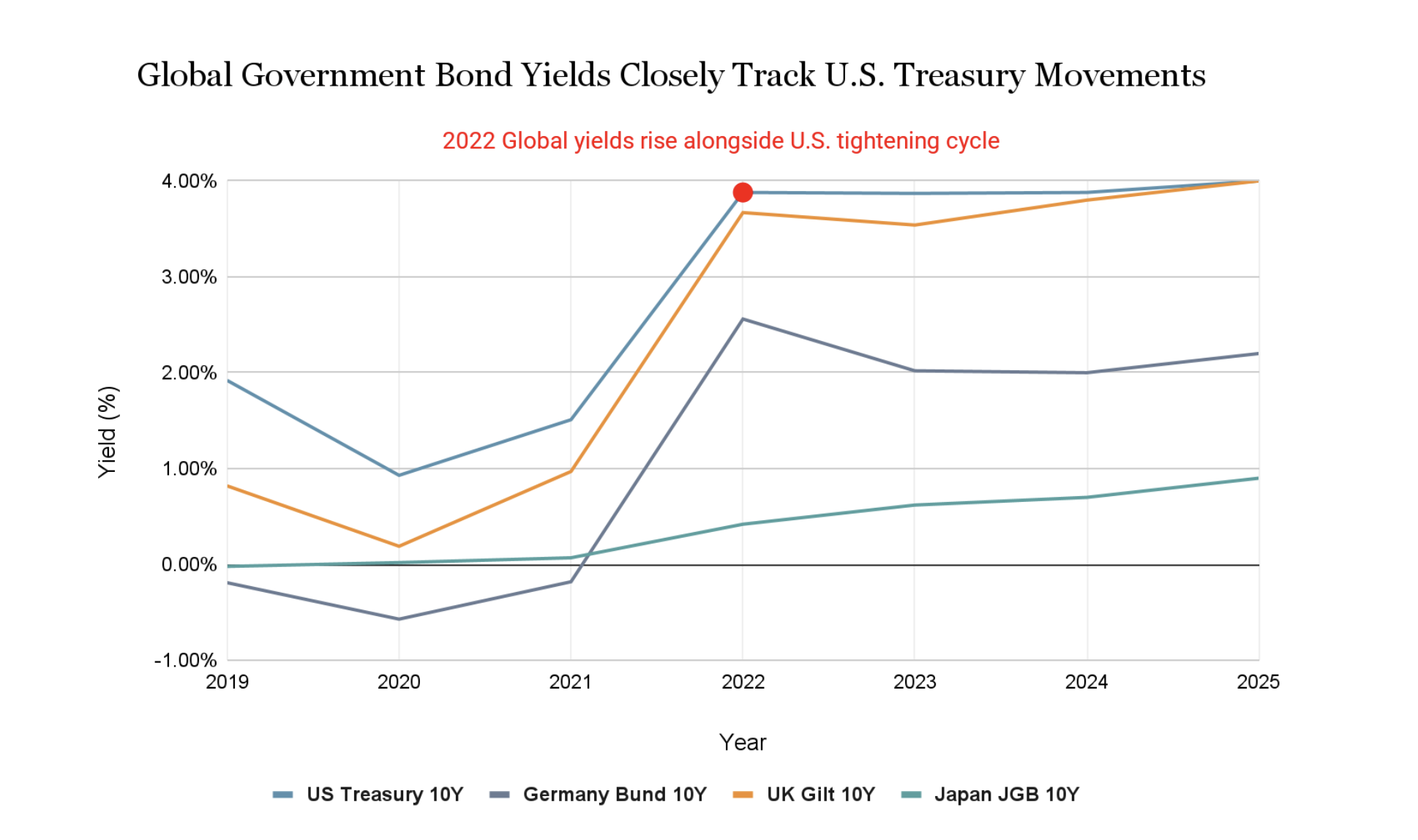

Another transmission channel that we have identified is Treasury securities as the global risk-free benchmark. When we discuss international finance, government bond yields are often tied and priced relative to U.S. Treasury yields. As a result, increases in Treasuryyields frequently lead to higherborrowingcosts for governments and corporations worldwide. With that said, even countries that have a strong domestic financial system often experience correlatedmovement in their bond markets when U.S. yields shift.

Furthermore, global capital allocation by the asset management and intermediary class industry is heavily concentrated in the US. Investment conglomerates like BlackRock, Vanguard, and State Street all manage trillions of dollars in global assets every day. Through various methods like ETFs that combine specific stocks, pension mandates and institutional portfolios these investment vehicles allocate capital across international markets, implying that investorsentiment toward U.S. markets often translate into large cross-border capital movements.

As a result of all, shocks on WallStreet often coincide with shocks on securities markets around the world. This strength that the U.S. has on securities and other financial instruments demonstrates how deeply integrated international financial systems can be.

-> Data Source: Federal Reserve Economic Data (FRED), U.S. Treasury Department, European Central Bank (ECB), Bank of England, Bank of Japan.

Chart Analysis

The above shown chart illustrates the close relationship between the U.S. Treasury yields and sovereign bond yields across major developed economies. We can observe that following the global inflation surge in 2022, as a result of the Covid-19 Pandemic, the Federal Reserve initiated the most aggressivemonetarypolicytightening in decades. Similarly, monetary policy contracting movements are also observed during that same period from other large economies like the UnitedKingdom, Germany and Japan. Even though Japan maintained a lower yield environment in comparison to other countries it is due to its yield-curve control framework following the stagnant growth from the 1990s decline. Besides, we can still find a correlation and a trend line - Japanese government bond yields gradually increased. The correlated movement of these yields highlights the central role that the United States has taken in shaping global borrowing costs. This reinforces the narrative that international bond markets remain structurally influenced by developments in U.S. monetary policy.

Designing a profitable portfolio with reduced U.S. exposure

While considering how powerful the presence of the United States is in the context of global finance it is difficult to avoid entirely. Investors can still make deliberatedecisions to reduce the concentration of their portfolios in American assets majorly because of the significant political instability ongoing as of 2026. Rather than trying to detach from the United States entirely, which would prove to be almost an impossible of a task, portfolio construction can bring focus on diversifying exposure across geographic regions, asset classes and other currencies that are not that closely tied to the U.S. dollar.

One approach to take here is to increaseexposure to equity markets outside of the United States. Efficient markets in developed countries like Japan, the United Kingdom, Canada, and Switzerland provide substantive and liquid capital markets that provide alternative sources within the realm of corporate earnings and economic exposure. With the election of the newly appointed Japanese PM Sanae Takaichi, investors sharedhope for the expanding future of the Japanese market - as shown by recent movements in major indices like the Nikkei 225. Japan’s equity market has attracted renewed global investor attention following the recent corporate governance reform - steering away from traditional methods and rising shareholder return policies. Simultaneously, several other emerging markets have shown continuous growth in the last few years. For instance, India has sustained a realGDPgrowth of 6-7% in recent years and has proven to be one of the fastest growing large economies around the globe.

This is all fuelled by demographic expansion and rising domestic consumption. Investors seeking diversified exposure to these markets often rely on exchange-traded funds tracking indices such as MSCI World ex-USA or FTSE Developed ex-US. These indices provide broad exposure to developed economies, including Japan, the United Kingdom, Switzerland, France, and Canada, while avoiding the heavy U.S. weighting found in traditional global benchmarks.

A secondary layer of diversification can be achieved through a method known as currency exposure. Essentially, an investor wants to broaden their investments to as many currencies that are stable and as looselytied to the dollar as possible. Although the U.S. dollar is seen as the most dominant currency around the world, other major currencies like the Euro, the JapaneseYen, and the British Pound-Sterling have a notable share in globalcurrencyreserves. About 20% of global foreign-exchange reserves are stored in euro accounts, and about half of that are in Japanese Yen and British pound.

Allocating capital to securities that are dominated by the alternative currencies can prove to be an effective method for getting exposure to alternative monetary policy environments, which in turn would reduce the reliance on the United States dollar.

As a final point to designing a diverse portfolio with lower U.S. exposure, many investors decide to incorporate real or defensive assets, which would act as a security towards systematic financial risk that might be caused by political instability. Preciousmetals and more particularly gold have historical proof to be stores of value during periods of currency and economic instability under stress. Data presented by the World Gold Council indicates that central banks purchased more than 1,000 tonnes of gold in 2022 and 2023. These numbers marked the strongest period of official-sector demand in years. These significant trend deviations suggest that among sovereign institutions, there is a will to diversify reserves away from the traditional dollar-priced assets.

When we take into consideration all of these points, put into practice allows investors to construct portfolios that have a lessened presence of U.S.-denominated financial assets. Still, total independence from American assets and market dynamics remains a very difficult task to achieve.

The Trade-offs of Reducing U.S. Exposure

Although through diversifying we reduce the concentration risk, it also introduces other important trade-offs for investors. Perhaps the most prominent one is the potential loss of exposure to sectors that are innovative and outperforming in gains as of now, in comparison to smaller markets. We must note that much of the global equity performance in recent years has been drawn from the United States directly. The technology sector within the U.S. alone represents more than 30% of the market representation of the S&P 500. Large corporations like Apple, Nvidia, Microsoft and Alphabet collectively hold over $1o trillion in market value. The aforementioned firms dominate global digital infrastructure, Artificial Intelligence development and cloud computing. In most cases, there are very few direct replacements to the products that these companies offer, and direct substitutes are limited in scale and market dominance, even at a similar price. Therefore, a portfolio that is substantially underexposed to U.S. securities may suffer from lower earnings growth.

Another very important consideration to take when discussing limitations is the issue of liquidity. As of today, the U.S. capital markets remain the deepest and most liquid in the entire world. The total market capitalization of the U.S. public equities was recorded to be $50 trillion as of 2024. This figure represents about half the value of all the globally listed equity. Meanwhile, the U.S. Treasury market has an estimated valuation of more than $26 trillion in government securities.

As we saw previously, the United States is considered to be a benchmark for risk-free global assets like treasury bonds. These strong markets provide investors with a high level of liquidity, price transparency and institutional participation that is nearly impossible to replicate by other regions.

Conclusion

So could investors build a profitable portfolio, which is decoupled from the U.S. Market?

Even though we have identified the goal of detaching from American-related assets there are investments which would be an effective hedge against the volatility and political instability in the United States ongoing as of 2026. Increased exposure to equity markets in developed and expanding markets like Japan, Canada, the United Kingdom, Switzerland, and India through exchange-traded funds (ETFs) such as MSCI World ex-USA or FTSE Developed ex-U.S. would be a simple first step for an investor looking to diversify his equity. An additional step would be to broaden their investments to different stable currencies that are as loosely tied to the dollar as possible, such as the Euro, the Japanese Yen, and the British Pound, which hold a notable share in the global currency reserves. Furthermore, exposure to precious metals such as gold and palladium provides a defensive hedge against financial risks driven by political instability.

With this in mind, an investor also has to consider the trade-offs of diversifying his investments, as with underexposure to innovative and market-outperforming sectors, such as the technology sector in the U.S., which represents more than 30% of the S&P 500, an investor may suffer from slower earnings growth.

Finally, although our uncertainty for the future of the United States might remain, global investors continue to treat U.S. financial assets as the primary safe-haven assets when uncertainty emerges. We vouch not to fully decouple from the United States but to provoke investors to look into the future and explore potentially safer investments in the long run.

This is not formal investment advice! Invest at your own risk!

Bibliography

Bank for International Settlements (BIS). (2025). Triennial Central Bank Survey of Foreign Exchange and Over-the-Counter (OTC) Derivatives Markets. Available at: https://www.bis.org

European Central Bank (ECB). (2025). Statistical Data Warehouse: Government Bond Yields. Available at: https://sdw.ecb.europa.eu

Federal Reserve Bank of St. Louis. (2025). Federal Reserve Economic Data (FRED): 10-Year Treasury Constant Maturity Rate (DGS10). Available at: https://fred.stlouisfed.org

International Monetary Fund (IMF). (2025). Currency Composition of Official Foreign Exchange Reserves (COFER). Available at: https://data.imf.org

International Monetary Fund (IMF). (2025). World Economic Outlook Database: GDP per Capita (Current Prices). Available at: https://www.imf.org

OECD. (2025). OECD Corporate Governance Factbook 2025: Global Public Markets and Corporate Ownership. Available at: https://www.oecd.org

MSCI Inc. (2026). MSCI World Index Factsheet. Available at: https://www.msci.com

World Gold Council. (2025). Gold Demand Trends: Full Year 2024 / 2025. Available at: https://www.gold.org

Bank of England. (2025). UK Government Bond Yield Curve Data. Available at: https://www.bankofengland.co.uk

Bank of Japan. (2025). Japanese Government Bond Yield Data. Available at: https://www.boj.or.jp

U.S. Department of the Treasury. (2025). Daily Treasury Yield Curve Rates. Available at: https://home.treasury.gov

Data Sources

(IMF, BIS, FRED, ECB, BoE, BoJ, Treasury)

Market Data & Indices

(MSCI, OECD)

Commodity / Alternative Assets

(World Gold Council)

Mihail Gaydarov

Chief Financial Analyst, The Financier Review.

Nikolay Marinski

Chief Business Analyst, Financial Analyst, The Financier Review.

© 2026 The Financier Review. All rights reserved.

This article is for informational and educational purposes only and does not constitute financial, investment, or legal advice. The views expressed are those of the author and do not necessarily reflect those of affiliated institutions.