The 2026 Iran war: are your assets in danger? analytical overview.

Research written by: Mihail Gaydarov, Chief Financial Analyst.

Key Market Takeaways

Brent crude rose 6–10% intraday, reflecting supply disruption risks through the Strait of Hormuz.

European equities declined ~2%, led by travel and consumer-sensitive sectors.

Defense and energy equities outperformed, supported by expectations of increased military spending and commodity upside.

Rising oil prices are lifting inflation expectations, pushing rate-cut expectations further into the future.

Portfolio positioning is shifting toward safe-haven assets and defensive sectors.

Background

As of February 2026, the conflict involving Iran and military actions taken by the United States and Israeli military has quickly escalated into a market-relevant event, rather merely a regional security issue. Market pricing, amid economic consequences such as disrupted energy flows, has become highly volatile. Investors are adjusting their strategies, steering away from regular securities such as stocks that have lost value over the last two days, that have also experienced high levels of market insecurity. Oil prices are rising sharply, with some analytical sources quoting figures as high as $100 per barrel, while simultaneously equity risk premiums are widening, and safe-haven assets like gold and other precious metals are attracting capital from investors.

This shift of attention reflects the immediate supply risk in energy markets – particularly through the Strait of Hormuz. Additionally, these disruptions in energy markets cause a knock-on effect for inflation, expectations on the FED for interest rate adjustments, and global growth forecasts. Considering all the aforementioned factors and understanding how these macroeconomic drivers interact is crucial for investors trying to manage heightened volatility and repricing in various asset classes.

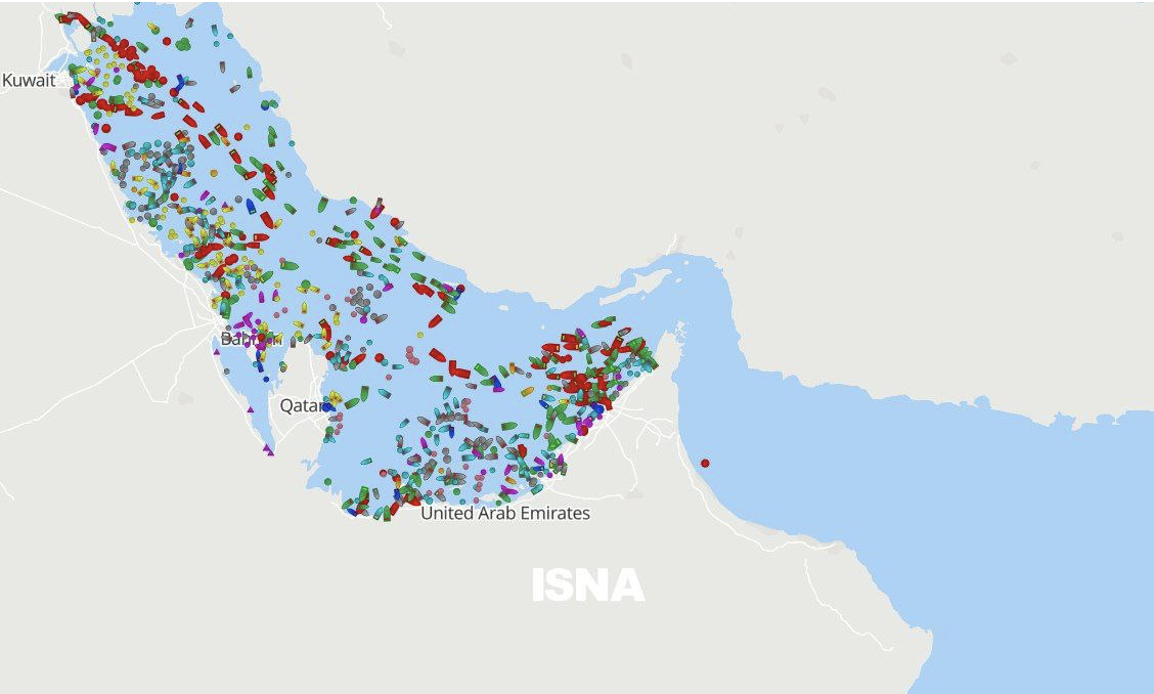

Strait of Hormuz - currently obstructed

Conflict Summary and Energy Markets Response.

On the 28th of February 2026, coordinated military strikes by U.S. and Israeli forces against Iranian strategic targets escalated hostilities, leading to Iranian missile attacks on regional bases and perceived threats to critical maritime infrastructure. The Strait of Hormuz, currently obstructed, is a strategic chokepoint in the energy market accounting for about 20% of global seaborne oil supply. As part of the retaliatory tactics of the Iranian regime towards the US and Isreal military actions, the strait is seized and all 170 container vessels, of which roughly 150 oil-bearing vessels remain immobilised. The blockade caused a steep contraction in tanker traffic as operators suspended transit amid security risk.

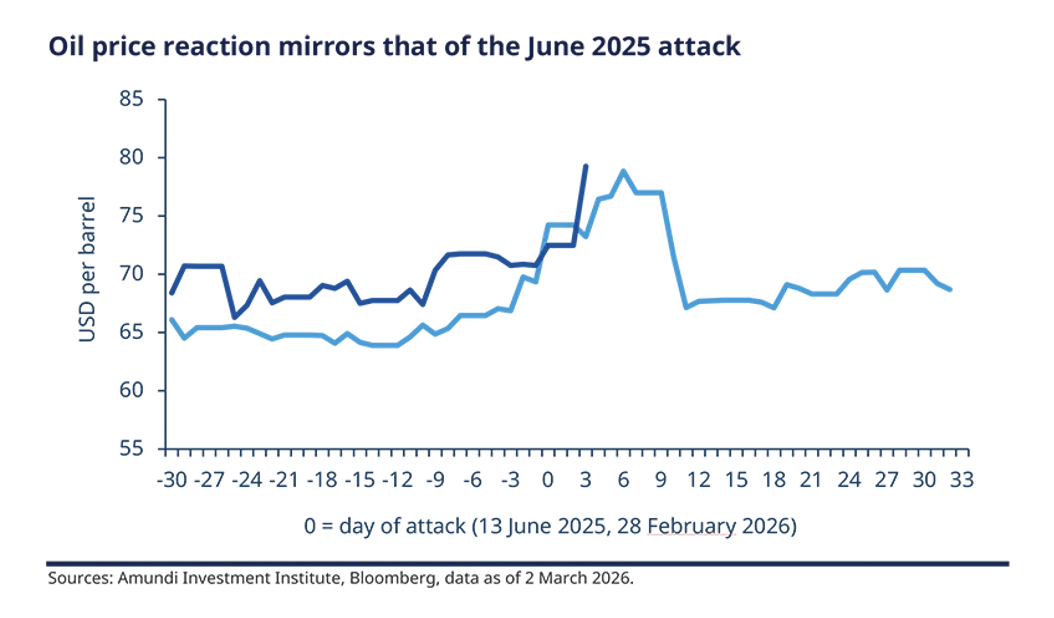

The immediate market effect that we observed was a substantial rise in crude oil and natural gas prices, caused by the supply disruptions. Brent crude oil rose sharply, reflecting the risk of prolonged supply disruptions. Gas prices similarly spiked, as LNG exports from Gulf facilities — including Qatar Energy operations — were disrupted

Source: Amundi Research Center

Furthermore, energy markets have become the primary transmission mechanism for geopolitical risk into global asset prices. Since early March, Brent crude oil, a type of light, sweet crude oil produced in the North Sea, rose roughly 6-10% intraday to prices above $80 a barrel. This sudden repricing in the energy sector has coincided with the sharp decline of major European indices with a decline of about 1.9-2.2%.

Likewise, major ETFs such as the Amundi MSCI Europe Index ETF, fell in value by 4.8% over the last 5 days. These market dislocations caused by the energy supply disruptions “put upward pressure on inflation expectations, compressing valuations across risk assets as investors adjust to a higher oil price regime and elevated uncertainty” as stated by Reuters.

Financial Markets: Equity, Bond and Overall Sector Dynamics.

The outbreak of war in Iran has significantly altered short-term price dynamics across major financial markets. Equity benchmarks and Exchange-Traded Funds (ETFs) experienced broad selloffs. Key European indices such as the French CAC 40 and Germany’s DAX 40 suffered major slips. Currently, the CAC 40 — which tracks the largest and most traded French stocks on Euronext Paris — has lost around 4% over the last week. Additionally, the DAX 40 fell about 4.8% since the 24th of February.

These declines are not merely market corrections but a reflection of investors reallocating their positions trying to mitigate surging volatility and risk caused by the emerging war in Iran.

Across other major sectors, cyclical and consumer-sensitive names have significantly underperformed. Travel-related stocks – which include major airline names and hospitality companies saw a decline of about 5-6% in their equity pricing. In some instances, as flight cancellations surged and global mobility expectations softened.Meanwhile, technology and other risk-sensitive growth assets lagged as market participants rotated out of higher-beta positions.

In contrast, to the decrease in price, we see with equities within the travel and hospitality sector, defense and energy equities outperformed the market. Defense contractors in the United States like Lockheed Martin and Northrop Grumman reported gains exceeding 3-4%, which were fuelled by public expectations of increased military spending for the American Military Complex amidst rising geopolitical tension and US involvement in military conflicts. Furthermore, energy producers also traded higher these last few days, tracking robust commodity price action as Brent crude jumped in excess of 6 %–10 %, reflecting disruption risks to oil flows through the Strait of Hormuz.

Fixed-income markets, which trade debt securities, such as government bonds exhibited mixed signals. While government bonds have been considered a safe-haven asset, especially during geopolitical stress, that shows low volatility when it comes to pricing saw pressures on prices as higher energy costs pushed inflation expectations upward – which in turn provoked repricing in yield curves for this class of asset. For instance, benchmark UK gilt yields rose amid diminished prospects for near-term cuts with inflation dynamics deteriorating. German Bund yields experienced a modest climb. In some regions of the world like Japan, short-term bonds offered by the government, had a yield that moved inversely. In a classic risk event, investors would purchase government bonds because they are considered safe. When the demand for government bonds rises, prices increase and yields fall. With Japan we saw a different story, due to oil pricing, rising inflation expectations and markets that are uncertain of Japan’s Central Bank leadership. Essentially, investors were unsure whether the central bank would tighten policy further to fight inflation. So, the uncertainty and accompanying other reasons caused these Japanese bond yields to move in the opposite direction.

Mutually, these moves by investors and markets for various assets demonstrated a trend towards risk-off positioning. The broad equity sell-offs and sector rotation out of demand-sensitive industries, and repricing of yield expectations are positive statements for this claim. Although some strategists view the initial selloffs as a short-term asset evet, we have a different claim The depth of commodity price disruption and its inflationary implications suggest that volatility may persist until clearer signals about conflict duration and energy supply normalization emerge.

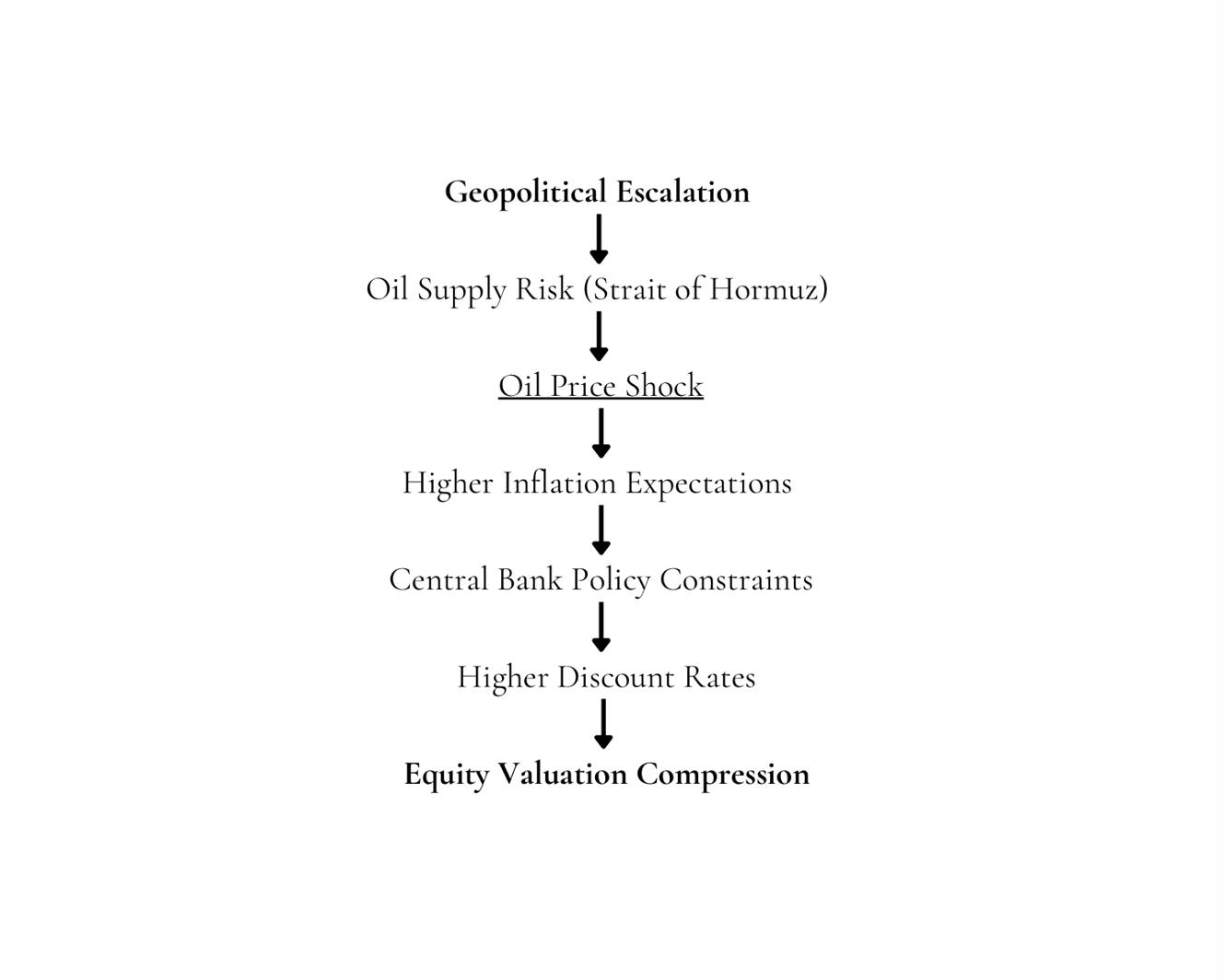

Macroeconomic Transmission Mechanisms

Chain Reaction Diagram.

The macroeconomic impact of the conflict involving Iran has mainly materialized through the energy supply channel, with secondary and perhaps long-term effect on inflation dynamics and growth expectations. As mentioned, the Strait of Hormuz accounts for about 20% of the global seaborne oil trade. Disruptions like the current Gulf obstructions introduce a structural risk into crude pricing. If a trend as such continues and political conflicts are not resolved, a sustained increase of $10-$15 per barrel in Brent oil would typically add several tenths of a percentage point to headline inflation across most advanced economies as crude oil is a crucial variable in production and transport industries. Of course, it is important to note that the proportion of influence is dependent on the degree of energy pass-through and currency effect for each individual economy.

Higher oil and gas prices act as an economy-wide cost shock. If we consider households, an increase in utility bills and fuels would result in an erosion of real disposable income, dampening discretionary consumption. When we look at businesses, input costs rise across variables such as transportation, manufacturing and heavy industry. The ultimate effect is a decrease in real income that would slow aggregate demand. Regions that engage in energy-importing instead of producing their own like Europe and some parts of Asia – face serious downside risks to growth under a sustained high oil price scenario.

Besides production cost implications, the rise in oil creates inflationary consequences, more particularly in the long run where it complicates the policy environment. Unlike demand-driven inflation, energy-induced inflation reduces growth while simultaneously elevating headline price indices, creating stagflationary pressure. As a result, central banks are constrained: an easing policy risks unanchoring inflation expectations, while tightening into a supply shock risk exacerbating a slowdown. As markets adjust to the political conflicts, rate-cut expectations are pushed further into the future which in turn would adjust short-term yields upward.

In the discussed framework here, energy prices serve more as the initiating variable, investor’s inflation expectations act as the propagation mechanism, and monetary policy constraints amplify the macro impact.

Strategic Market Implications for Investors

Considering the current geopolitical shock, the key takeaway is that an investor must engage in reassessment of portfolio risk rather than reactive positioning. The elevated energy prices caused by the supply chain disruptions of crude oil, accompanied by the widening risk premia would imply that volatility is most likely going to remain high for the upcoming week. In such an unpredictable environment capital preservation and selective asset exposure is crucial and a more effective investment strategy than aggressive risk-taking.

The dispersion of sectors is expected to persist. Producers of energy and most defense-related equities have the potential to benefit from direct revenue linked to demand for military equipment. Conversely, sectors that are vulnerable to transportation costs, discretionary demand and credit conditions should be monitored more closely – as it would be expected that their financial condition tightens.

Equity multiples, particularly in growth segments, face compression as higher inflation expectations sustain upward pressure on discount rates.

If we consider cross-assets it would be expected that the demand for safe-haven assets like precious metals and the US Dollar would persist, supported by investor uncertainty. It is important to consider that as we observe the initial implications from the war in Iran, bond markets may not provide uniform protection, especially if the inflationary expectations roll on to become the case in the near future.

From a strategic standpoint, the appropriate posture wouldn’t be to fully liquidate risk, but more of a calibrated allocation. Maintaining both capital and asset liquidity, emphasizing on the strength of a company’s balance sheet and their market pricing power. Waiting in such cases would be beneficial, at least until energy pricing stabilizes or we observe clearer policy.

Market Positioning Implications

Maintain defensive sector exposure (energy, defense).

Reduce exposure to transport and discretionary consumption sectors.

Monitor rate-sensitive growth equities, which remain vulnerable to higher discount rates.

Maintain liquidity buffers until energy price stabilisation.

Conclusion

Fundamentally, the 2026 Iran attack is a repricing event. The geopolitical shock has altered important valuation inputs like commodity prices, discount rates, inflationary expectations, and risk premia. Markets are adjusting to incoming news, but more importantly to a shift in expected cash flows and required returns.

The increase in oil prices surges input costs for firms and inflation volatility, which negatively affect earnings estimates and the discounted rates that apply to those earnings. Higher expected inflation constrains central bank flexibility, pushing rate-cut expectations further out and keeping real yields elevated. The combined effect is multiple compression, particularly in duration-sensitive equities. The sector dispersion reflects this repricing mechanism precisely. Firms that have direct exposure to commodity upside, or pricing power tend to outperform the market. Meanwhile, businesses that are leverage-heavy and sensitive to demand face pressure in their valuation.

As observed, safe-haven assets like bonds no longer function as a uniform hedge. Nominal yields are scrutinized by inflation expectations and in a case where growth is not met or in the worst case deteriorates, they would suffer as well. In this sense, cross-asset correlations become unstable, and assets that otherwise should not be moving together do.

From a capital allocation perspective, the current stress environment rewards liquidity management and resilience on a balance-sheet level. Until the energy prices experience a reasonable stabilisation expected return distributions remain skewed towards higher volatility and lower-risk adjusted equity performance. Thus, the analytical focus should lie on monitoring inflation breakevens, yield curve movements and the volatility of commodities.

Market Indicators to Monitor

Brent crude oil price

Key threshold: $90–$100 per barrel

U.S. 5-year inflation breakevens

Indicates whether energy shock is feeding inflation expectations.

VIX volatility index

Measures risk-off sentiment across global equities.

U.S. Dollar Index (DXY)

Safe-haven demand during geopolitical stress.

Global shipping and tanker traffic through the Strait of Hormuz

DISCLAIMER: This is not investment advice, invest at your own risk!