Liquidity: the most MISUNDERSTOOD force in financial markets

Author: Mihail Gaydarov, Chief Financial Analyst.

Image source: Wikipedia, Fidelity - Taken by Vera de Kok.

Liquidity as an investment illusion

When we observe financial markets, we receive this false impression that whenever somebody sells a position, there is always another player on the stock market to buy it. We default to the idea that markets are liquid by default. High trading volumes of a certain asset and tight bid-ask spreads reinforce this perception of ease when it comes to investing, especially when bought or sold in normal conditions. Modern markets have the tendency to be sufficiently liquid and, especially if we compare them to historic events, they do seem to be rather predictable and safe. As a result of these assumptions, it is safe to assume that the average participant in direct finance is seldom going to examine liquidity as long as the pricing of assets continues to move smoothly and lacks fluctuations.

Yet history has repeatedly shown us that the notion of market liquidity is not a constant. It is most abundant when markets are calm and most fragile when an outlier event occurs. In periods where the stock market, or any asset market for that matter, is under stress, we tend to observe the ability of an entity to transact diminish – even when some assets are widely regarded as resilient to “black swan” events.

In that sense, a question arises to an investor that we try to answer here: If liquidity is plentiful in favorable market conditions, why do we tend to observe a diminish the moment markets are under pressure?

What is liquidity? (and what it isn’t)

Fundamentally, the term liquidity refers to the ability of an asset owner to transact at meaningful size, in a swift manner, without having a material effect on the established market price. We must keep in mind that this definition extends far beyond surface indicators such as trading volume or narrow bid-ask spreads. A market for an asset can show high turnover (volume of buy and sell orders) and, at the same time, remain shallow beneath the surface, similarly to how tight spreads can coexist with limited depth. The true liquidity of markets is derived from the capacity of market participants to absorb the flow of orders without demanding a significant price concession.

Prominently, liquidity is a function of the market itself and not a categorizing property of an asset. The whole notion relies on the presence of sufficient depth and the availability of balance sheet capacity for the orders to be executed without extreme concession. Furthermore, the properties of liquidity of a market are also conditional on the financial intermediaries standing ready to transact. Whenever any of the aforementioned conditions are weakened, liquidity can deteriorate rapidly even in presumed robust markets.

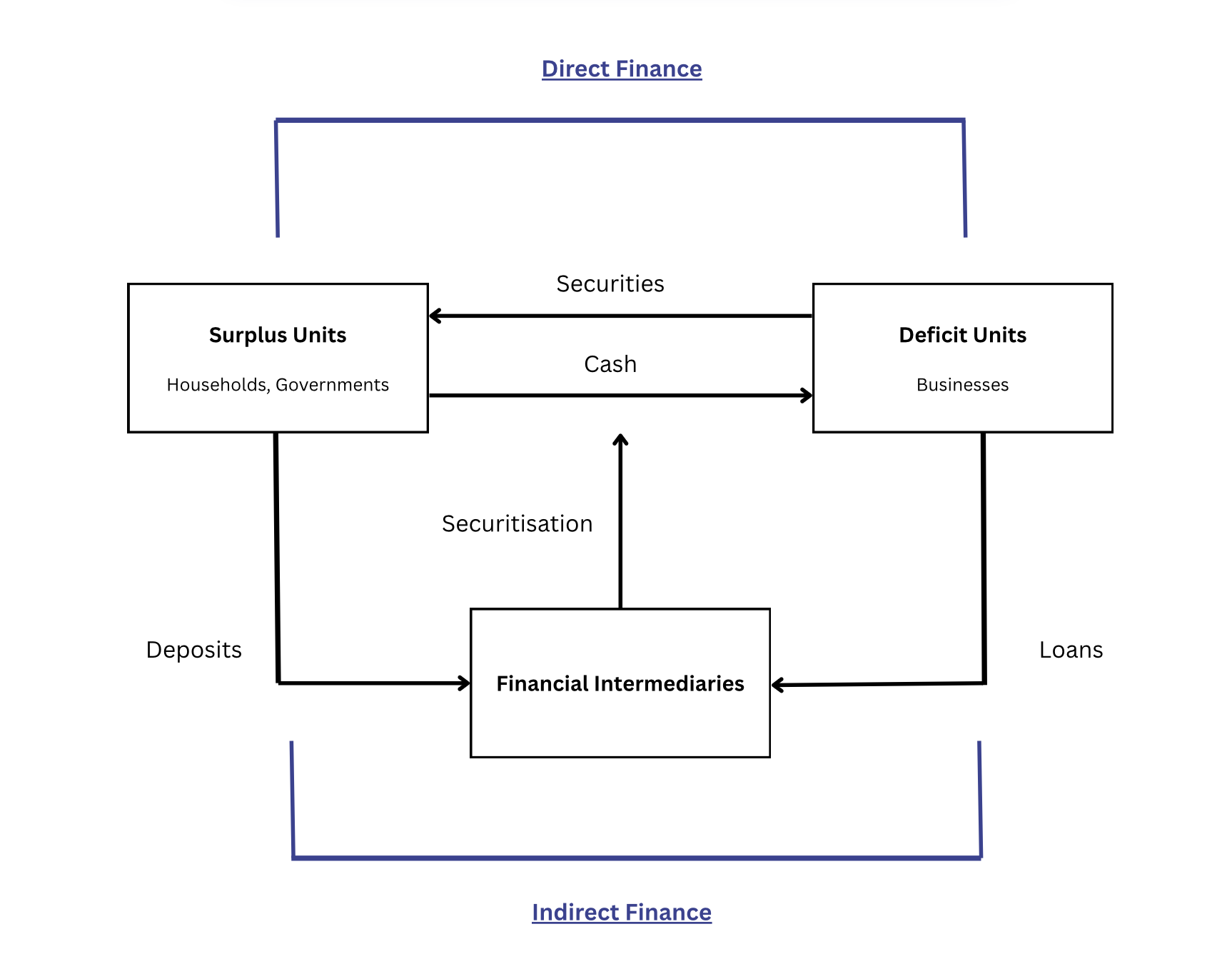

Who actually provides liquidity?

Now here is the part where most inexperienced investors stumble. As mentioned, liquidity is a property of the transactional relationship within a financial market. Thus, liquidity in modern financial markets is largely sourced by financial intermediaries like banks and mutual funds (the two largest by market share) and their willingness to stand between the buyers and the sellers. Market makers and dealers absorb order flow by taking positions on their own balance sheets, profiting from the spreads and inventory management. From a historical perspective, large investment banks played a central role in the process of intermediation when it comes to indirect finance; mass regulation has changed that dynamic and reduced the scale of their direct market activities or practices such as securitization.

In modern times, this dominance of banks within the intermediary sector has changed significantly. High-frequency private firms like mutual funds have taken a leading position in providing short-term liquidity, continuously quoting prices and facilitating rapid transactions. Nevertheless, it is important to note that much of the liquidity that these entities provide is based on speed rather than on their balance sheets. This implies that this surface-value liquidity is fragile and sensitive to volatility and risk conditions. Asset managers may also provide liquidity indirectly when their trading objectives align with market demand, but their participation is inherently conditional.

Essentially, the most critical point to be made here is that liquidity is supported by balance sheets and risk tolerance. When we talk about the resilience of markets, we have such conditions when financial intermediaries are both able and willing to absorb inventory risk. Whenever any of these two factors diminish, liquidity can recede very quickly.

The conditional nature of liquidity.

Although liquidity is perceived as an inherently normal feature of a financial market, we must keep in mind that without intermediaries this property will almost entirely vanish. One of the main issues with the support from intermediaries is that, to provide liquidity, they have to be the bearer of the risk – more specifically, they bear the inventory risk. They manage to achieve this by temporarily holding assets on their balance sheets while facilitating the transaction between the surplus unit and the deficit unit. This mechanism is not without consequence to the intermediaries, and as well as holding the risk, they are often subject to price fluctuations which can trigger a chain of events and cause mass disruptions within the balance sheet of the intermediary. If market volatility and risks increase, the risk to the intermediary increases accordingly.

Source: Principles of Banking and Finance, E. Becalli

In addition to the inventory risk that intermediaries have to bear, liquidity also depends on the specific capacity of the balance sheet that an intermediary has. Essentially, due to regulations and capital constraints, intermediaries have limited room to reduce their own risk. In some cases, regional governmental regulations do limit buy and sell orders for intermediaries. Thus, when uncertainty increases within the market, or when losses decrease the available capital that the intermediary has, their ability to intermediate diminishes. Because of all that, liquidity provision might become too expensive or simply unachievable.

Furthermore, these organizations also have internal limits and constraints, in addition to the regional governmental ones and their physical availability of capital. In many situations, these intermediaries have a limit on the risk that they can take in highly volatile market situations. Policies like value-at-risk thresholds and leverage constraints are designed to protect solvency. When these limits are breached, intermediaries lower their exposure and undermine the provision of liquidity – in some cases stepping back entirely from markets. As a result, liquidity exists primarily when it is economically viable and operationally permissible for intermediaries to provide it.

How liquidity disappears before prices even move?

Whenever markets are under stress, we have to note that liquidity rarely vanishes all at once – more so, it deteriorates in stages. One of the first signs that liquidity is diminishing is a reduction in the actual depth of the market. There are fewer orders quoted at the best available prices, and the volume that is possible to be transacted without affecting price declines. Although on the surface prices appear stable, beneath, the capacity of the market to absorb order flow is slowly weakened.

With uncertainty increasing, financial intermediaries that provide most of the liquidity widen bid-ask spreads in order to compensate for the rising risk in their inventory. The widening itself is a rational response of an intermediary due to the elevated uncertainty and the balance-sheet exposure. Thus, even very small imbalances begin to move prices substantially due to the lowered market depth and wider spreads.

From here, whenever this process begins to pick up speed, the adjustment of the prices gives way to discontinuous movement. Trades that would normally be absorbed smoothly instead force prices to gap as available liquidity at intermediate levels disappears. What we often describe in financial markets as sudden volatility is often the mechanical but invisible consequence of liquidity withdrawal.

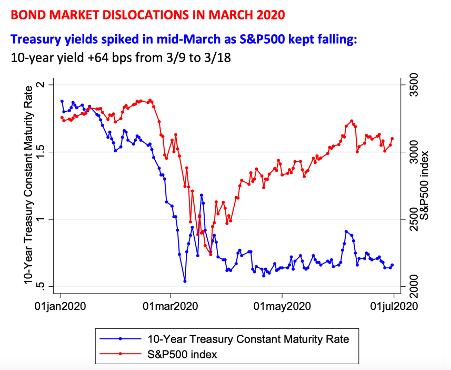

A clear depiction of this occurrence happened in March 2020. The U.S. Treasury, majorly regarded as the deepest and most liquid asset, experienced severe dislocations. As documented by the FED and BIS, market depth became very shallow, and price impact amplified, while at the time there was no real doubt among investors regarding the solvency of the U.S. government. This example confirms that even the most solvent of markets can be shaken by balance-sheet constraints.

US Treasury Bond Liquidity diagram (March 2020)

Graph Source: Adam Tooze

In this sense, unstable prices of an asset are often a symptom of deteriorating liquidity rather than the root cause of the losses. Markets are not illiquid because they move – prices fluctuate sharply due to the receding power of trading absorption mechanisms.

Why investors misread liquidity?

One of the key reasons that liquidity is misunderstood is because when markets are stable, it is most visible. The high trading volumes and tight ask-bid spreads, resulting in ease of transaction, cater to the impression that markets are deep and secure. However, this surface level often represents markets in secure times where we see normal conditions and structural resilience rather than chaos. Investors tend to overestimate the solvency of a market due to the smoothness of transactions in the present day. Assumptions that regular-day liquidity is similar to stress days on the stock market are inherently false.

A further source of misinterpretation is newly emerged trading tools. Oftentimes, electronic trading platforms and exchange-traded funds create a false sense of security that the ease of transaction is an inherent characteristic of the stock market. While these instruments may trade actively, their liquidity ultimately depends on the underlying assets and the willingness of intermediaries to absorb inventory risk. So, when stress can be observed, a distinction becomes very crucial – while some assets may appear liquid on the surface, constraints often cause massive disruptions that are nearly invisible to the regular investor.

Finally, although diversification is important and certainly recommended, it is more likely to create a sense of complacency than actual security. As a tactic, diversification is often beneficial in stable times when correlations operate as predicted, are moderate, and markets can absorb order flow efficiently. However, it is important to note that when financial markets are under stress, the contraction of liquidity can synchronize asset movement since participants aim to reduce risk simultaneously. The structural tightening of liquidity conditions is often a reflection of structural alterations rather than a fundamental reassessment of value.

Therefore, the fundamental issue here is not underestimating volatility but overestimating the permanence of liquidity. Smooth markets are not necessarily robust markets; they are simply markets in which the mechanisms of intermediation are functioning normally—for the time being.

Liquidity as the Hidden State Variable.

In conclusion, we can argue that liquidity is often treated as a background feature of financial markets – presumed to be present if trading occurs in a market and prices move suddenly. Yet what we find to be the case is that liquidity is neither permanent nor guaranteed. Suppliers of liquidity, or intermediaries, operate under severe internal and external stress like governmental regulations, internal company policies, and balance-sheet constraints – which ultimately may shift the incentive of the intermediary to provide liquidity. When constraints become stricter, the ability of the financial market to absorb order flow weakens, resulting in price instability.

Understanding liquidity as a conditional and structural force reframes how market stress is interpreted. Sharp price fluctuations are not always the origin of instability but more of a consequence of the shallowing of a market – in essence, the subtle withdrawal of intermediaries that had previously kept markets stable. In this sense, liquidity functions as a hidden state variable: invisible in calm periods, decisive when conditions deteriorate. Markets do not fail because prices move. They fail when the mechanisms that normally allow prices to move smoothly cease to function.