“LBO-ing” a Merger - Paramount "Hops After" Warner Bros. with a Deal Approval.

Two and a Half Companies.

Most of the media we now know is majorly operated and created by a handful of entertainment giants. Despite their overwhelming current position and success, all of them had simple and modest beginnings, which are worth exploring in order to better understand the current events.

The most widely known and used entertainment platform is the streaming giant Netflix. It was founded by Reed Hastings and Marc Randolph in 1997 in Scotts Valley, California. Hastings got the idea after he was annoyed by a $44 late fee for a Blockbuster VHS tape. The first plan for Netflix was simple, but innovative - they would send DVDs by mail for a flat monthly rate. People could also order online, which was a fresh idea at the time. Additionally, Netflix used data to suggest movies people might like, making the service more attractive and easier for users. In 2000, Netflix faced hard times with the burst of the dot-com bubble, and the company had a lot of expenses. Hastings and Randolph went to Blockbuster with a $50 million offer to sell Netflix, but the leaders of Blockbuster, feeling sure of their position in the market, turned down the offer, even reportedly laughing at it. In 2007, Netflix made the big move of launching a streaming service, with the rapid spread of fast internet. The breakthrough came in 2013 with the release of their first original series, followed by the creation of other productions, awarded for their creativity, originality and captivating storylines. Nevertheless, the biggest driver for Netflix’s success is the advanced Cinematch algorithm it uses, which has the capability to process and analyse large volumes of user data and provide tailored recommendations for each user.

One of the oldest American media and entertainment conglomerates, Warner Bros’s story began more than 100 years ago. It was founded by the four brothers, Harry, Albert, Sam, and Jack Warner. Everything began in 1903 when movies transitioned from simple spectatorship of an event to the beginning of skilful narrative storytelling, allowing the audience to get lost in the movie they saw on screen. Sam pitched to his family the idea of investing in this technology. The four brothers combined all of their money, and with some help from their father, Benjamin Warner, who had to pawn his gold watch, they managed to buy a projector for $1,000. They started from their backyard and, after the success, moved to a vacant store, hoping to capitalise on the influx of people from the local carnival. They quickly saw that their business was booming and started to go to nearby towns as well. But they realised that the key to real profit was to have their own venue. In the following years, they continued to expand their operations. As nickelodeons opened in nearly every town, the brothers recognised that the biggest opportunity was in movie distribution, and they founded Duquesne Amusement Supply Company. By 1914, they had begun producing films, and by the early 1920s, they acquired their first studio in Hollywood. On April 4, 1923, with the help of money landed to Harry, they formally incorporated, creating Warner Bros. Pictures. The immense success of the early sound films enabled Warner Brothers to become a major motion-picture studio. By the 1930s, Warner Brothers was producing around 100 movies a year and controlled nearly 800 theatres, with 360 theatres in the United States and more than 400 abroad. In 1953, Jack Warner took full control of the company by buying 90% of the stock. He began expansions into different fields, including animation (Looney Tunes [Warner Bros. Cartoons]), music (Warner Bros. Music), and later television (Warner Bros. Television Studios). In 1967, the company was sold to Seven Arts Productions, run by Eliot and Kenneth Hyman, for $32 million and was renamed to Warner Bros.-Seven Arts.

However, two years later, they sold it to the Kinney Corporation, which was headed by Steven J. Ross, who had also recently acquired National Periodical Publications (now known as DC Comics), Television Communications Corporation (later becoming Time Warner Cable) and Paperback Library (Warner Books). He created the entertainment conglomerate Warner Bros., Inc., which became a highly diversified subsidiary, venturing into such areas as music, video games, and comic books. The Kinney National Company was later renamed Warner Communications, and after merging with Time Inc. in 1990, it became Time Warner. In the mid-2000s, Time Warner separated or sold several Warner-derived or branded divisions as independent companies, including Warner Music Group, Time Warner Cable, and Warner Books. Additionally, on December 3, 2002, Time Warner's film and television divisions were incorporated into a new Warner Bros. Entertainment subsidiary. More recently, Time Warner was acquired by AT&T on June 15, 2018, and renamed WarnerMedia. AT&T then sold WarnerMedia to Discovery, Inc. to form Warner Bros. Discovery on April 8, 2022.

Another giant in the industry is the well-known Paramount. It dates back to 1912, which is the founding date of the Famous Players Film Company. The founder, Adolph Zukor, was an early investor in nickelodeons. He saw that movies appealed mainly to the working class. With his partners Daniel Frohman and Charles Frohman, he planned to create and offer feature-length films that would appeal to the middle, featuring some of the famous at the time, and they founded the Famous Players Film Company. The following years were very eventful, starting in 1916, with the merger of Zukor’s Famous Players with The Jesse L. Lasky Company, which was producing films in Hollywood. On May 8, 1914, Paramount Pictures Corporation was founded by William Hodkinson, who merged five smaller firms. On May 15, 1914, Hodkinson made an agreement and signed five-year contracts with the Famous Players Film Company, the Lasky Company, and other producers to distribute their films and became the first successful national distributor. However, in 1916, Zukor had a plan to merge Famous Players, the Lasky Company, and Paramount. Zukor and Lasky took over by buying out Hodkinson of Paramount, and joined the three companies into one. As a result, the new enterprise became the largest film corporation at the time with a value of $12.5 million ($380 million in 2026). Zukor was the main reason for the success of Paramount, as he built a chain of around 2000 screens, ran two production studios and invested early in technologies like radio. A strategic move he made was the acquisition of the successful Balaban & Katz in 1926, who had developed the concept of the “Wonder theatre.” The success did not continue for long as the over-expansion and use of overvalued Paramount stock created a $21 million debt to the filing for bankruptcy on March 14, 1933. Bankruptcy trustees were appointed, which led to Zukor losing control of the company. It wasn’t until 1935 that the company reemerged as Paramount Pictures Inc. It continued to expand and grow, with setbacks along the way, like the Supreme Court decision in 1948 that movie studios could not own theatres, which parted the theatre chain into United Paramount Theatres. Some of the most notable moments include when the failing Paramount was sold to Gulf and Western Industries in 1966, which helped restore the reputation of the company. Additionally, the acquisition of Viacom over Paramount in 1994 and later in the 2000s, the merger with CBS, where Viacom obtained it, created one of the world’s largest entertainment companies, combining TV, movies and radio. In 2022, the conglomerate renamed itself to Paramount Global to centre the company around the internationally recognised Paramount brand. The recent merger between Paramount Global and Skydance Media, at a valuation of $28 billion, formed Paramount Skydance. Finally, most significant is the current acquisition of Paramount over Warner Bros. Discovery, with Netflix backing off from the deal after being outbid by Paramount.

An “Unforgiven”Standoff.

In the modern streaming industry as we see it today, scale is no longer a competitive advantage within the market, but more of a prerequisite for survival. As the growth of subscribers begins to slow, the costs of creating new content for users becomes incrementally larger. Due to high demands for profits from investors, large media companies like Netflix and Paramount enter a brutal phase of consolidation. For Netflix, the acquisition of Warner Bros Discovery allows the conglomerate to evolve from a dominant streaming platform into an empire that singlehandedly controls some of the most valuable intellectual property in the world. Such property includes HBO, DC, and the century-old film library of Warner Bros.

Considering the other party, interested in the acquisition of Warner, we have Paramount Skydance, also a very prominent media conglomerate, established nearly 100 years ago. But what we have to carefully consider is that the potential merger of any of these two parties is done under polar circumstances. Unlike Netflix, the acquisition of Warner Bros Discovery for Paramount is more of an existential matter. A Netflix-Warner combination would have concentrated unprecedented market power into a single competitor, further marginalising already weakened legacy studios struggling with declining linear television revenues and increasingly unprofitable streaming operations. Paramount was therefore no longer pursuing Warner Bros. Discovery simply as a strategic acquisition, but as a defensive necessity to avoid long-term irrelevance in an industry where scale increasingly determines survival itself.

“Beat or be beaten. In a dog-eat-dog consolidating market the only way to stay in is to keep those knocking on your neighbour’s porch out. An opportunity and a risk-taking to ensure one’s own survival as the junior becomes a senior with the help of a number of bankers ready to bet for the sake of private credit and the extremes of fiscal discipline, or in this case the lack thereof.”

Looney (Tunes) Loans

A conglomerate after a $110.9 billion deal and around 200 million subscribers to its streaming platforms. This is what the merger deal between Paramount Skydance Corporation and Warner Bros. Discovery, Inc. could achieve if it gets U.S. clearance, which has started to seem a bit shaky in the past few days. A colourful pallet of controversy, financing miracles and the crazy extents, to which capitalism could bring 2 media and entertainment companies.

After mentioning the standoff between Netflix and Paramount, we could continue with the actual active players in the merger deal with Warner Bros. So the question is simple: “Who writes the check?”, though the answer is not. Starting with the actual structure of the buyer, Paramount Skydance Corp. has Class A shares with voting rights and Class B shares without such rights. Harbour Lights Entertainment holds 100% of Class A voting shares, which are then distributed with a 77.5% stake for CEO of Paramount Skydance, David Ellison, and a 22.5% stake for RedBird Capital. The total Class A and Class B shares of David Ellison account to a bit above 50% within Paramount Skydance giving him a majority stake.

An interesting point to note is the close relationship between the Ellison family and RedBird Capital as they have helped Skydance Media in 2024 finance the acquisition of National Amusements, Inc., i.e. the holding company of the former Paramount Global, from the Redstone family to create Paramount Skydance. What is even more “looney” than that is the Chinese multiple co-investments together with Tencent Holdings in Skydance prior to the merger with Paramount Global. Furthermore, Tencent Holdings was scrutinised when attempting to finance $1 billion for the merger between Paramount Skydance and Warner Bros. Discovery, which in the end forced them to exit, though re-entering indirectly with a smaller sum in the hundreds of millions as a “passive financial investor”. Returning to RedBird, this is not the only Chinese interaction. During the controversial attempt at Telegraph Media Group, which ultimately collapsed, several human rights groups signaled RedBird Capital chairman John L. Thornton’s close relationship with Chinese political and economic elite circles. Regarding the Paramount-Warner Bros. deal, a combined equity $47 billion equity package for the WBD shareholders involving the Ellison family and RedBird Capital is one of the main components of the 100% acquisition of WBD as an all-cash transaction. From the $47 billion, Larry Ellison, father of CEO David Ellison and CTO of Oracle, has committed $40.4 billion as an equity financing guarantee against roughly 1.6 billion of his Oracle common stock.

Before adding more complexity we have to take a look at the balance sheets of Warner Bros. Discovery and Paramount Skydance. The former has an existing debt burden of around $29 billion still lingering from Warner Bros. acquisition of Discovery. Meanwhile, the latter has around $10.36 billion in debt after the acquisition of Paramount Global itself. Continuing with the “Looney Loans”, Paramount Skydance has agreed to take $54 billion in initial mostly bank commitments from Bank of America, Citigroup, and Apollo Global Management. To this end, $39 billion has been incremental new debt for the acquisition and $15 billion as a backstop, i.e. bridge debt, for WBD’s existing debt piles. Another smaller portion of the financing has also been announced as $3.25 billion in rights offering, meaning more equity financing, to existing Paramount shareholders. This could bring a total debt pile of more than $90 billion, analysts say (the financing through Gulf investments has not been fully disclosed in the implementation yet). However, when factoring in the company's refinancing and proactive liability management efforts, it is estimated that the combined entity will reasonably carry between $45 billion and $55 billion in net debt post-transaction.

The latest news regarding moneybags jumping on the bandwagon have been regarding the deal struck between Paramount Skydance and a number of Gulf sovereign wealth funds such as Saudi Arabia’s Public Investment Fund, L’imad Holding Co. (UAE / Abu Dhabi), and Qatar Investment Authority acquiring 15.1%, 12.8%, and 10.6% respectively of the new Paramount-Warner Bros. conglomerate, which sums to a 38.5% Gulf stake of Class B non-voting shares for $24 billion. In term, the Ellison family has sought to ease their exposure in the $40.4 billion of financial guarantees, as well as lowered the aggregate bridge loan from $54 billion to $49 billion. Unfortunately for the company with existing foreign stakes, summing up to 49.5% also due to a Chinese stake via Tencent Holdings, has sounded the alarm at Washington and invited unwanted attention from the FCC with a rigorous review of the firm being inevitable.

As of May 2026, the deal had secured early approval from Germany and Slovenia within the EU, despite the EU commission's pending response, which signaled a broader consensus for the deal and made U.S. clearance not as an “if” but as a “when”. This has rapidly evolved though, as U.S. lawmakers are starting to understand just how intransparent the whole situation is. Senators Warren and Booker co-signed a formal letter to U.S. Treasury Secretary Scott Bessent demanding that the Committee on Foreign Investment in the United States (CFIUS) open an immediate investigation into the merger and raising concerns of the Gulf and Tencent stakes at the conglomerate and the possible financial and media (CNN and CBS News) dependencies arising from that. Furthermore, Senators Warren (again) and Blumenthal joined Congressman Sam Liccardo and 11 other House members in demanding that the Department of Justice (DOJ) and the U.S. Treasury closely examine the merger's threat to market competition, while further stating risks for higher prices to consumers when combining two of the five remaining film studios. The cherry on top once more comes from Senator Warren as she publicly labeled the merger as an “antitrust disaster”, while commenting on the close personal relationship between President Donald J. Trump and the Ellison family, particularly Larry and David Ellison. This became apparent after the hosting of a formal dinner by David Ellison attended by the Donal Trump, members of his cabinet, and media executives, which aggregated public protesters, also due to the comments of Trump’s Pete Hegseth criticising CNN for reporting the war in Iran and David Ellison’s promise for “sweeping changes to CNN”. The most recent hurdle has been the push of 34 Democratic lawmakers from California who are galvanising the broader push against the merger with them sending a letter pressing Attorney General Rob Bonta to get involved in the antitrust investigation with the situation seeming increasingly uncertain for the deal.

To complicate the situation external actors continue to undermine the deal with a suspected aggregator being Netflix after losing the merger deal to Paramount Skydance. The entertainment giant has faced a series of accusations regarding its quiet support for public opposition campaigns and potentially reaching out to regulators with concerns over the deal, though Netflix continues to deny involvement. On top of that an open letter in Hollywood from April 2026 collecting signatures of industry professionals has been initiated to help with the blocking of the merger and signed by over 4700 as of early May 2026. One of the signatories is Mark Ruffalo, a famous actor for his performance as “Hulk” at Marvel, has signaled that many actors are afraid to sign the letter due to fear of being blacklisted from the entertainment giants. Despite that a growing consensus is arising that the deal should not happen and it is a matter of time before the regulators step in.

However, U.S. clearance is far from the only significant point worth discussing as every merger requires a stable buyer, which seems increasingly shaky for Paramount Skydance.

The “Wolf” of Wall Street Strapped for CasH.

Rating agencies have always played an important role in determining the prospects of a company, but in Paramount’s case only doom and gloom have foreseen the company in the last few years. In 2023 S&P Global Ratings demoted the company to BB+ (“junk”) due to systematic risk, which was followed by subsequent demotions also by Moody’s and Fitch in 2024 and 2025 respectively.

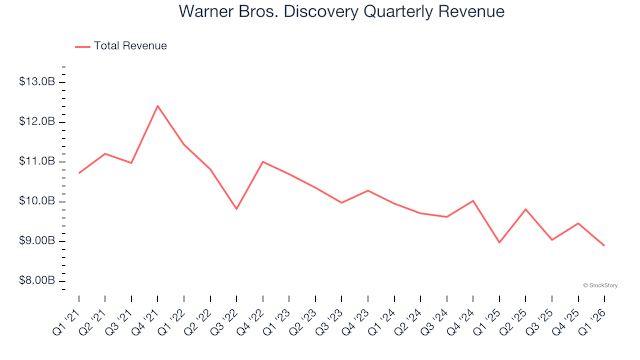

Terminal decay of linear television, involving faster-than-expected declines in advertising and affiliate fees, as well as immense capital burn in a desperate position in the direct-to-consumer (DTC) segment with cash burners such as Paramount+ and Pluto TV. Impairment-Based Revaluations were further prompted after the increasingly bleak reports from financial analysts, which resulted in goodwill impairment write-downs for both Paramount Global and Warner Bros. in 2024 for $5.98 billion and $9.1 billion due to the downward adjustments regarding expected future cash flows after referencing the decay of linear television, the asset impairment and the companies’ valuations after merger transactions. Further losses in 2024 and 2025 amount to $1.16 billion in programming charges for abandoned projects and lower than expected FCF due to missing licensing fees for Paramount and $422 million in content impairment fees for Warner Bros. Moreover, Paramount recorded $149 million in charges in 2024 to write down the carrying values of its FCC and Australian broadcast licenses to their newly estimated fair values and changing their accounting methods for licenses in order to make them amortisable.

In the first half of 2024 Centerview Partners performed a DCF analysis of Paramount using a higher discount rate (WACC) ranging from 8.5% to 10.5% based on the lower credit rating, macroeconomic mechanics, size of the risk premia, capital structure. Regarding the merger the combined entity has been targeting an EV/Revenue multiple of 2.0x-3.0x, which based on analyses has been regarded as “defensible”. With estimated revenues ranging $60-$70 billion a conservative valuation of $120 billion and an extremely optimistic one of $210 billion could be derived from them. After subtracting an estimated $45 billion to $55 billion in post-transaction net debt, analysts calculate an implied equity valuation for the combined entity of $65 billion to $155 billion, i.e. a stock price between $60 and $140 per share. Defending these valuations sits the estimated EV of WBD at $110.9 and the approx. EqV at around $81 billion. The bid of Paramount Skydance is to buy out all Warner Bros. Discovery shares for a fixed $31/share price, which raises the question about the free float of Paramount. As David Ellison controls around 49% of Class B shares with a 3% and a 13% minority interest by Harbour Lights Entertainment and RedBird Capital, the free float rate could be calculated to around 35% giving the company some liquidity on the market with a share price of around $10/share in early May 2026. This could increase if Paramount delivers on its intentions to further finance the merger by rights offering for an additional $3.25 billion.Estimates either support the theory that the stock is extremely undervalued and some say the exact opposite with the aforementioned target being $60 to $140 per share.

Ok, but how do you defend this when taking into account the current net income, FCF, CAPEX and Debt-to-EBITDA of the buyer? Paramount Skydance has not had a single positive year for net income since 2023 with a total loss of around $7.9 billion for 2023, 2024, and 2025, with the company having a positive Q1 net income of $168 million. The FCF margin has hovered between 0.5% and 1.7% with it being currently a 1.3% for 2026 Q1, meaning the company is in a serious need for cash and capital restructuring. Paramount has weak recent free cash flow, while 2026 requires heavy transformation spending regarding the move to the Oracle Fusion Enterprise Resource Planning System and real estate and office consolidations, amounting to a significant CAPEX increase to around $800 million. Furthermore, the WBD transaction adds very high leverage with further merger agreement clauses limiting additional over-budget expenses. The last nail in the coffin is the Debt-to-EBITDA, which is around 4.3x. Such an enormous multiple could only be reasonable if the fully synergised EV/EBITDA for 2026 materialises as 7.5x, which is unlikely after taking into account the expression “fully synergised” in a behemoth such as “Warnermount”.

To the previous statement, it has to be elaborated on the question: “How could Paramount believe that it is right to use a fully synergised enterprise valuation and revenues respectively?”

A Synergy Ramp Flatter than a Basketball Court.

Overvaluating synergies in a megamerger of this scale presents several severe financial and operational risks. The financial models and promises of the buyer driving the combination of Paramount Skydance and Warner Bros. Discovery relies heavily on an estimated $6 billion in expected annual synergies. Unfortunately, the people making the calculations have stated that an immediately synergized consolidation is to be expected, which is both fictional and dangerous.

Like a “jam at the basketball court” it is unrealistic to expect that everything will go as smoothly as planned while unrealised projections for cost and revenue optimisations, to say the least, will be implemented fully starting from next Monday. This is why especially in mergers as complex as this one a synergy ramp is to be taken into account with their gradual implementation. Even if operations are integrated successfully, often risks arise and unexpected or unwanted costs with expectations for gains falling as time passes, hence their implementation via a synergy ramp. In this case the sum of the synergies is best to be distributed in the span of 4 to 6 years to minimise bias and wait for tangible outcomes.

With integration costs “swallowing” benefits with examples being execution risk with possible delays or failures during integration, timing risks regarding the future value of money and one-off cost underestimation with management not expecting as high of restructuring costs, severances, IT migration costs, etc. Further issues arise through revenue dis-synergies when customers leave to the integration changes, automatically lowering revenue synergies, or through double-counting synergies once as a cost reduction and once as a margin expansion. This is not an exhaustive list and the point is clear - synergies give a lot of room for manoeuvring and are an unreliable source of fiscal space.

Regarding segment and architectural synergies significant proposals have been made. About the internal architecture itself it is very likely that the whole conglomerate will move to a unified ERP system, which is almost certainly going to be Oracle Fusion ERP. This will also be followed by the physically consolidating the two iconic studio slots at Hollywood and Burbank belonging to Paramount and Warner Bros. respectively. Segment synergies involve the massive technological undertaking of consolidating their DTC streaming technology stacks, such as merging the backend of Paramount+ and Max into a single unified platform.

Operational efficiencies are also a part of the spotlight. Across the companies' various business segments, management plans to achieve cost savings by eliminating redundant corporate functions, such as human resources, legal, and finance departments. This integration is expected to be heavily driven by new AI-based workflows, alongside broader procurement savings and general operational streamlining, which could be interpreted not as a simple buy-and-build tactic but rather an intelligence-led consolidation with real restructuring value.

Through the aforementioned synergies a broader category of cost and revenue synergies could be defined, which is included as extra $6 billion in the fully synergized enterprise value. An astronomical amount though with some significant points made in favour. The cost synergies are outlined mostly as technological integration with a common ERP system and DTC streaming platform, operational efficiencies mostly through restructuring and automation, and real estate and office consolidation. This unfortunately does not quite state the immense CAPEX increase, which will follow and will be heavily scrutinised due a high Debt-to-EBITDA, extremely low FCF margins, and merger agreement spending constraints. Adding to that we also have to mention the revenue synergies stated as pricing power scale regarding the oligarchic state of the streaming platform sector and “ParamountMax” (if we could call it so yet) rivalling Netflix, a better demographic usage of the platform expanding to newer consumers and expected to grow from 200 million to 210 million directly post-merger, as well as better retention rates due to the more homogenic content within the platforms boosting retention rates. Despite that the double-counting effect of synergies and the revenue dis-synergies often lower the final outcome.

So taking into account the faulty implementation of synergies and the more realistic case of $1 billion to $1.5 billion pre-merger, which is still incorrect as nothing is immediate, this will make the fiscal situation even tighter with a lower EV/Revenue multiple and a higher Debt-to-EBITDA multiple significantly raising the risk premium.

But at the end of the day who will give a hand to such a risky client?

But at the end of the day who will give a hand to such a risky client?

How Private Credit acts as the Godfather.

The whole merger deal between Paramount Skydance and Warner Bros. Discovery has become a sensation in the media due to numerous caveats in just one merger. One of the most interesting could be that the acquired is four times the size of the acquirer. This is not a simple merger, it is a proxy LBO as if this was a private equity fund.

This was achieved through a series of aggressive financial maneuvers designed to bypass traditional acquisition hurdles, heavily reliant on private credit institutions and banking syndicates providing financing without the strict fiscal discipline prerequisites typically demanded in such high-stakes transactions. To raise the required $47 billion in cash equity to buy out WBD shareholders, the Ellison family and RedBird Capital executed a massive equity syndication strategy with Larry Ellison’s personal guarantees of $40.4 billion through 1.16 billion Oracle shares and the further help of Gulf sovereign wealth funds.

Initially, the primary skepticism surrounding the megamerger was the severe financing risk of carrying around $90 billion in debt in a declining linear television market. However, management has actively turned this financial risk into a core strategy through proactive balance sheet restructuring. Rather than simply piling on new debt and waiting for maturities to hit, the company is actively refinancing existing obligations, extending debt maturities into the future, and reshaping its capital structure. By smoothing out the debt profile and reducing near-term refinancing pressures, executives are trying to eliminate the cause of concern regarding incoming liquidity risks, which frees management to focus on operational efficiencies and integration. Nevertheless, this is a debt loop where new debt is always the answer and the need for constant refinancing and liquidity being the main focus increasing shareholder-value orientation at the cost of other stakeholders.

Who benefits? This is no secret after the media rundown of the whole saga. The Ellison family will gain absolute control over a media empire that includes CBS, CNN, and a significant influence over TikTok in the U.S. via Oracle's infrastructure, which could influence the freedom of the press. Like so David Ellison is set to become the "most powerful person in Hollywood". Warner Bros. Discovery will also gain a lot via the $31/share deal, which will account to almost 150% over the stock price. It is said that the CEO of Warner Bros. Discovery David Zaslav will gain $550 million to $780 million from the merger. Gulf countries will also win a lot from such a strategic acquisition with a 38% stake at Paramount-Warner Bros. with unprecedented leverage over American news and entertainment. For financing the whole deal private creditors and banks earn fees for syndicating and managing the $54 billion debt load. It is a full financial ecosystem relying on Paramount-Warner Bros. to pay off its debt or to refinance it via increasingly focusing on shareholder value and likely increasing prices in a consolidating market.

Despite a bleak situation in the balance sheet, how could this all play out?

Focus. Strategically, of Course

“Paramount Skydance views its $110.9 billion acquisition of Warner Bros. Discovery as a powerful "accelerant" to its vision of creating a next-generation media and technology empire.” This is how it may sound from a position of strength. How about another perspective: “Paramount Skydance’s $110.9bn acquisition of Warner Bros. Discovery can be framed as an admission that its standalone business lacks the scale, cash generation, and strategic relevance needed to compete independently.”

This is the truth regarding the current market dynamics and in society as a whole. People are moving to streaming platforms and Paramount Skydance does not have the capacity to compete. This is why they need to team up with someone out of their league in order to survive in such a brutal landscape. Currently no company has the capacity to compete with Netflix at this scale and only combined efforts may offer an alternative. With Paramount-Warner Bros. plans to merge their streaming platforms, film studios, restructure and implement AI in their processes the whole situation becomes more manageable with a focus on efficiency and gaining market share while consolidating the media and entertainment landscapes.

Nevertheless, the oligarchic situation of the American and in some sense the global entertainment industry is becoming increasingly vicious in its attempts to maximize profits. This is why these companies should always keep a note when considering their customers. The entertainment industry is a pure discretionary and if these companies abuse their position of power within a fragmented but also competitively not as significant market landscape, then a streaming service fatigue could easily develop, which could even now be linked to the surge in online piracy. This harms intellectual property rights but the enforceability could be difficult if people start doing it en masse. As such companies should prioritize user experience instead of profits, which in turn would drive more sales.

Although a market giant would appear, Paramount-Warner Bros. will be difficult to manage and govern. Cultural integration is an important management risk when discussing adaptability with both Paramount Skydance and Warner Bros. Discovery having different corporate cultures, leadership structures, and creative processes, where poor integration could stifle productivity, which is much needed when you once enter a cycle of constant refinancing and the need for liquidity.

Governance is a whole topic by itself but upon the closing of the transaction, entities controlled by the Ellison family will hold approximately 77.5% of New Paramount's voting Class A common stock. Because the Ellisons will control more than 50% of the voting power, New Paramount will officially be classified as a "controlled company" under Nasdaq listing rules. This designation allows the company to opt out of standard corporate governance protections, meaning New Paramount is not required to maintain a board with a majority of independent directors, nor is it required to have an entirely independent compensation or nominating committee. Meanwhile, the vast majority of the company's equity will be held by Class B common stockholders, who will have absolutely no voting rights.

Furthermore, the company's new charter waives the "corporate opportunity doctrine" for the Ellison family and RedBird Capital. This legally permits the controlling stakeholders to invest in competing businesses without presenting those opportunities to Paramount first, creating a built-in conflict of interest between the board and public shareholders.

One more point. The deal relies heavily on $24 billion from Middle Eastern sovereign wealth funds (Saudi Arabia, the UAE, and Qatar) and capital linked to the Chinese conglomerate Tencent. While structured as non-voting shares to avoid regulatory triggers, lawmakers warn this massive financial dependency could allow foreign governments to exert indirect pressure on the editorial independence of American news networks like CNN and CBS News.

This is interesting to say the least. But will all of this even matter if the U.S. blocks the merger?

Conclusion: “Its Arrival”

As of the 8th May 2026 a trend emerges where more and more people and organisations are getting involved in the move of blocking the merger between Paramount Skydance and Warner Bros. Discovery due to blatant violations of acting in good faith.

The whole process has been a mess from the beginning with the bidding war between Netflix and Paramount Skydance. Now it has escalated into a book meddling situation with fictitious synergies and a pressuring campaign against descent in broader Hollywood as well as accepting foreign investments and entering into a vicious debt refinancing cycle in order to outbid the opponent while seeking shelter from antitrust measures under the umbrella of the Trump administration and the President himself in exchange for a crackdown in media pluralism.

At the end of the day what is left is the final product, which the company is offering. In this sense it will be “ParamountMax” as the streaming platform, the jobs it will still offer after the restructuring, and production powers in the fields of entertainment and media. A company should focus on the quality of its service and if the goal is to be a real rival to Netflix, then the focus will have to solely lie in the execution of processes efficiently and delivering what is wanted, possibly at the price that is wanted.

Despite the whole discussion nothing is certain. The U.S. regulators will have the final say. Until then people can either wait for a definitive result, or act in order to tip the scales either in favour of the merger or not.

Resources

“Companies Ranked by Market Cap - CompaniesMarketCap.com.” Companiesmarketcap.com, 2024, companiesmarketcap.com.

“Credit.” Apollo.com, 2024, www.apollo.com/strategies/asset-management/credit.

Financial Times. “Financial Times.” Financial Times, 12 May 2023, www.ft.com.

“Fitch Ratings:Credit Ratings&Analysis for Global Financial Markets.” Fitch Ratings, www.fitchratings.com.

“Home | S&P Global Ratings.” Www.spglobal.com, www.spglobal.com/ratings/en/.

“Industries | Deloitte.” Deloitte, 2024, www.deloitte.com/global/en/Industries/tmt.html. Accessed 8 May 2026.

MacroTrends. “Netflix Revenue 2010-2023 | NFLX.” Macrotrends.net, 2024, www.macrotrends.net/stocks/charts/NFLX/netflix/revenue.

Moody's. “Moody’s - Credit Ratings, Research, Tools and Analysis for the Global Capital Markets.” Www.moodys.com, 2022, www.moodys.com.

“Paramount Global Debt to Equity Ratio 2010-2025 | PARA.” Macrotrends.net, 2025, www.macrotrends.net/stocks/charts/PARA/paramount-global/debt-equity-ratio.

“PARAMOUNT to ACQUIRE WARNER BROS. DISCOVERY to FORM NEXT-GENERATION GLOBAL MEDIA and ENTERTAINMENT COMPANY | Paramount.” Paramount.com, 2026, www.paramount.com/press/paramount-to-acquire-warner-bros-discovery-to-form-next-generation-global-media-and-entertainment-company.

“Paramount–WBD Merger Looks Stronger as Debt Strategy Shifts.” Investing.com, 21 Apr. 2026, www.investing.com/analysis/paramountwbd-merger-looks-stronger-as-debt-strategy-shifts-200678902. Accessed 8 May 2026.

“Psky-20251231.” Sec.gov, 2025, www.sec.gov/Archives/edgar/data/2041610/000204161026000011/psky-20251231.htm.

“SEC Filing | Paramount.” Paramount.com, 2025, ir.paramount.com/node/70906/html.

“The New Sovereign of Cinema: ParamountâS $111 Billion Conquest and the Future of Media.” FinancialContent, 27 Feb. 2026, markets.financialcontent.com/stocks/article/finterra-2026-2-27-the-new-sovereign-of-cinema-paramounts-111-billion-conquest-and-the-future-of-media. Accessed 8 May 2026.

U.S. Securities and Exchange Commission. “SEC.gov | HOME.” Sec.gov, 5 Feb. 2017, www.sec.gov.

“Warner Bros Discovery Debt to Equity Ratio 2010-2025 | WBD.” Macrotrends.net, 2025, www.macrotrends.net/stocks/charts/WBD/warner-bros-discovery/debt-equity-ratio.

“Welcome to Zscaler Directory Authentication.” Mckinsey.com, 2026, www.mckinsey.com/industries/technology-media-and-telecommunications.

All data used in this article is derived from publicly available institutional reports and industry analyses.

This article is for informational purposes only and does not constitute investment advice.

Spas Arsov

Financial Analyst, M&A Specialist.

Mihail Gaydarov

Chief Financial Analyst

Nikolay Marinski

Chief Business Analyst

The Financier Review

© 2026 The Financier Review. All rights reserved.